Peter Friz's talk at the SNSL24 скачать в хорошем качестве

Peter Friz's talk at the SNSL24

1 год назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Peter Friz's talk at the SNSL24 в качестве 4k

У нас вы можете посмотреть бесплатно Peter Friz's talk at the SNSL24 или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Peter Friz's talk at the SNSL24 в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Peter Friz's talk at the SNSL24

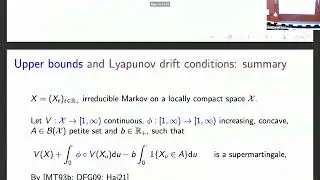

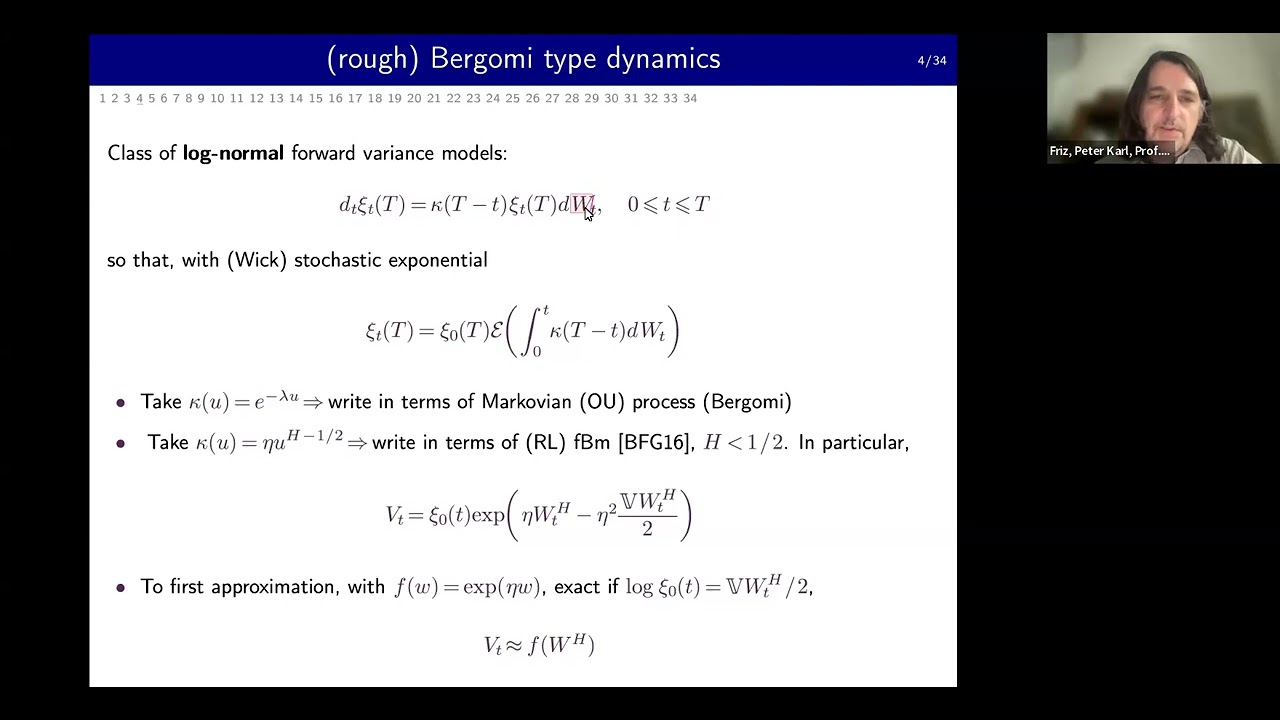

Peter Friz - Rough analysis of rough volatility models The question what rough paths have to do with finance has received many answers in recent years, this talk is devoted to some these. I will start by reporting on recent work that identifies the weak rate for a class of rough (Bergomi type) volatility models. In a second part, I will present a rough PDE based extension of the Romani-Touzi formula, describing the law of some asset under partial conditioning, applicable in particular to local rough stochastic volatility models. Finally, I will present an extension of Gatheral's diamond calculus, motivated by rough Heston in forward variance form, to expected signatures, offering systematic computations in general semimartingale models. Credit to numerous coworkers will be given in the talk.

Comments