Can Data Scientists Save Hedge Funds? | Morgan Slade | AnacondaCON 2017 скачать в хорошем качестве

Can Data Scientists Save Hedge Funds? | Morgan Slade | AnacondaCON 2017

9 лет назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Can Data Scientists Save Hedge Funds? | Morgan Slade | AnacondaCON 2017 в качестве 4k

У нас вы можете посмотреть бесплатно Can Data Scientists Save Hedge Funds? | Morgan Slade | AnacondaCON 2017 или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Can Data Scientists Save Hedge Funds? | Morgan Slade | AnacondaCON 2017 в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Can Data Scientists Save Hedge Funds? | Morgan Slade | AnacondaCON 2017

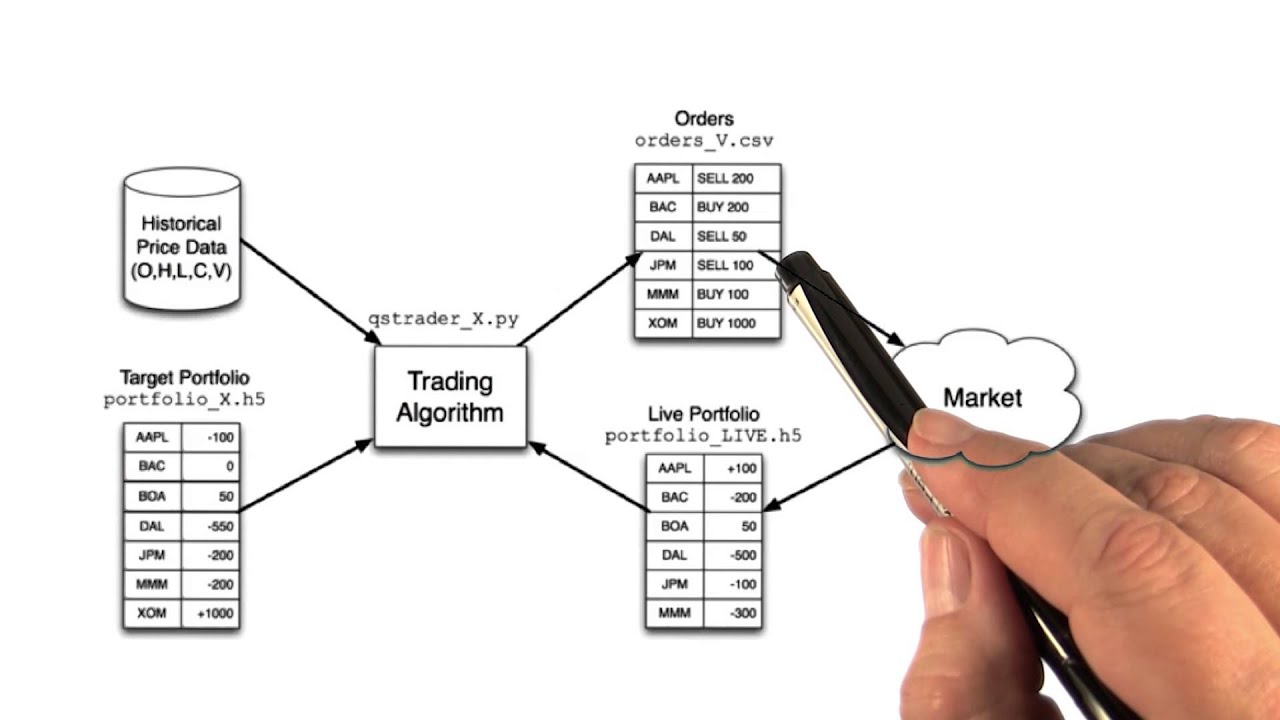

The hedge fund industry, once known for innovation and high absolute returns now lags the passive investing indices (e.g. SPY, during the period from 2009 to 2016). Most hedge funds trade the same strategies, have the same risk factor exposures, and have effectively replicated each other. In recent years, systematic hedge funds have sought to automate these well-known hedge fund strategies and have substantially done so. Research teams for hedge funds have not generated enough ideas to keep pace with asset growth. Annual returns without the deduction of management fees have declined to 5.43% per year on average from 2011 to 2015. Recently startups have created crowd research tools to address this gap between alpha production and alpha demand. We believe they will be successful if the crowd researchers are not required to become domain experts in trade execution. Cloudquant using Anaconda and other open source python toolsets provides research tools to simulate execution and a business model that enables data scientists to generate alpha ideas at scale by allowing them to focus on data science. Presented at AnacondaCON 2017 by Morgan Slade, CloudQuant. Download Morgan's slides here: https://www.slideshare.net/continuumi...

Comments

-

9 лет назад

9 лет назад

-

-

9 лет назад

9 лет назад

-

2 года назад

2 года назад

-

-

5 лет назад

5 лет назад

-

Трансляция закончилась 2 месяца назад

Трансляция закончилась 2 месяца назад

-

3 года назад

3 года назад

-

7 лет назад

7 лет назад

-

Трансляция закончилась 1 день назад

Трансляция закончилась 1 день назад

-

Трансляция закончилась 13 часов назад

Трансляция закончилась 13 часов назад

-

Трансляция закончилась 3 месяца назад

Трансляция закончилась 3 месяца назад

-

11 лет назад

11 лет назад

-

-

6 лет назад

6 лет назад

-

8 часов назад

8 часов назад

-

5 лет назад

5 лет назад

-

3 года назад

3 года назад

-

Трансляция закончилась 1 месяц назад

Трансляция закончилась 1 месяц назад

-

9 лет назад

9 лет назад