Скачать с ютуб Eurodollar futures contract (FRM T3-28) в хорошем качестве

Eurodollar futures contract (FRM T3-28)

6 лет назад

Скачать бесплатно и смотреть ютуб-видео без блокировок Eurodollar futures contract (FRM T3-28) в качестве 4к (2к / 1080p)

У нас вы можете посмотреть бесплатно Eurodollar futures contract (FRM T3-28) или скачать в максимальном доступном качестве, которое было загружено на ютуб. Для скачивания выберите вариант из формы ниже:

Загрузить музыку / рингтон Eurodollar futures contract (FRM T3-28) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Eurodollar futures contract (FRM T3-28)

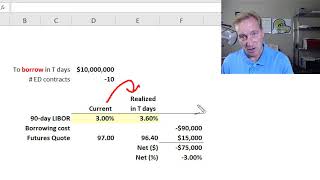

[my xls is here https://trtl.bz/2O6m5ea] A Eurodollar (ED) futures contract is an interest rate derivative: it references a future three-month LIBOR interest rate. The futures quote is given by Q = 100 - R, where R is LIBOR; for example, a ED futures quote of 97.00 signifies an anticipated 3-month LIBOR of 3.00%. The contract price is designed so that a one basis point Δ in LIBOR corresponds to a $25.00 gain/loss on a single contract. The long (short) position gains (loses) $25.00 if LIBOR decreases (increases) by one basis point (0.010%). Finally, keep in mind that the LIBOR rate is expressed with an actual/360 day count (typical of money market instruments) with quarterly compounding. Discuss this video here in our FRM forum: https://trtl.bz/2EbRkBK.

Comments