Seller Financing vs Traditional Loan I Bought Properties Both Ways скачать в хорошем качестве

Seller Financing vs Traditional Loan I Bought Properties Both Ways

12 часов назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Seller Financing vs Traditional Loan I Bought Properties Both Ways в качестве 4k

У нас вы можете посмотреть бесплатно Seller Financing vs Traditional Loan I Bought Properties Both Ways или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Seller Financing vs Traditional Loan I Bought Properties Both Ways в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Seller Financing vs Traditional Loan I Bought Properties Both Ways

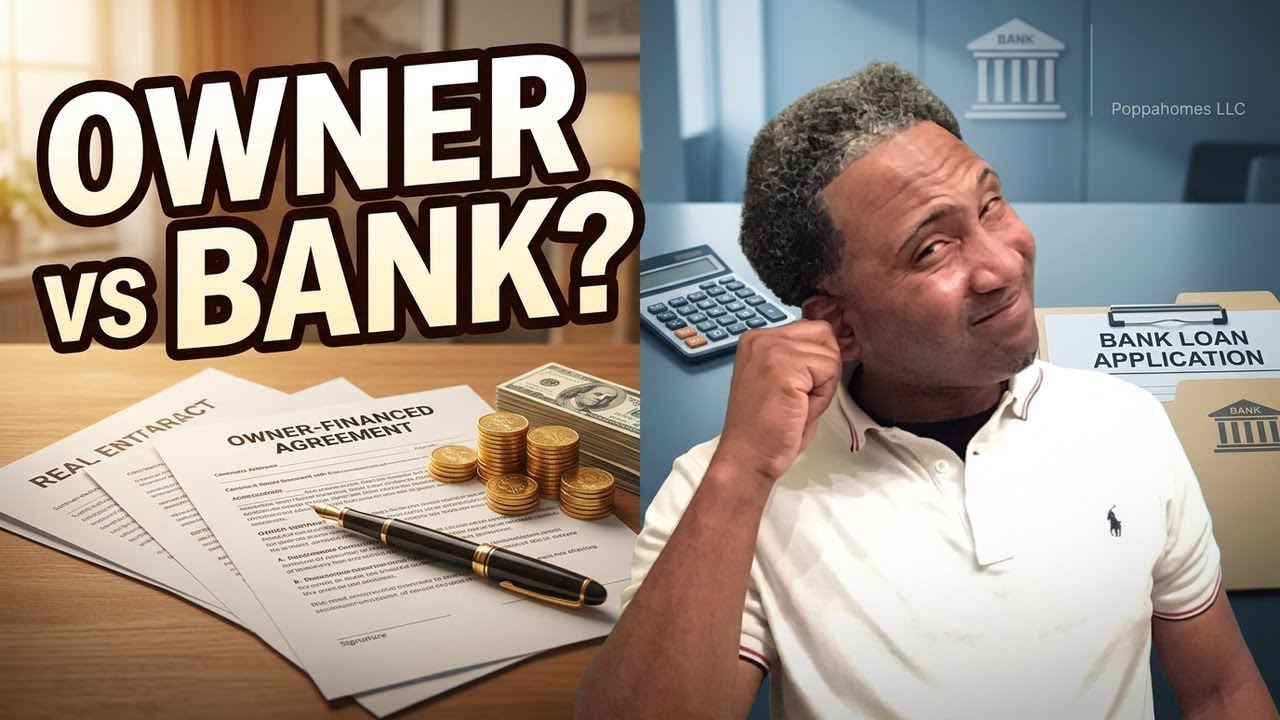

I bought two duplexes, almost identical, within the last year. For the first one, I went through the soul-crushing, mind-numbing process of getting a traditional bank loan. For the second, I used a strategy most people have never even heard of called seller financing. And the difference it made to my bank account—and my sanity—is pretty shocking. Welcome to Poppa Homes https://www.colemanmg.com/30k/ Invest With Poppa https://www.colemanmg.com/30k/Portfolio Poppa I Need a House https://www.colemanmg.com/30k/poppa-i... Poppa’s Buy Houses https://www.colemanmg.com/30k/shrevep... See, most people think there’s only one way to buy real estate: you save a huge pile of cash and then go beg a bank to approve you. But what if I told you that's not how the pros play? That there’s a way to buy property with way less cash out of pocket, close in a fraction of the time, and negotiate terms so good the bank would literally laugh you out of the room? This isn’t just theory. Today, I’m pulling back the curtain on two of my own deals. I'm going to show you all the numbers, the headaches, the whole nine yards. And by the end, you’ll see the surprising winner in the battle of traditional loans versus seller financing, and you can decide which path is right for you. *Section 1: The Traditional Loan Story - The Devil You Know* Alright, let's talk about Property Number One. We'll call it "The Bank Duplex." It was a classic bread-and-butter duplex in a great rental neighborhood. The numbers worked, the building was solid—I knew it would cash flow. Asking price was $300,000. Going the traditional route just felt like the “safe,” normal thing to do. So, I kicked off the process. And let me tell you, if you’ve never financed an investment property with a conventional loan, prepare for a marathon of misery. First up: the down payment. For an investment property, banks want 25% down. That’s $75,000 cash that vanished from my account before we even got to closing costs. For a lot of people, that’s a deal-killer right there. All that capital is instantly held hostage, tied up in a single property, unable to be used for your next deal. Then came the paperwork. It wasn't a pile; it was a mountain. Two years of tax returns, three months of statements for every bank account I have, pay stubs, and letters explaining any deposit over a few hundred bucks. The underwriter became my new, very annoying pen pal. Every email sent a jolt of anxiety through me. "We need to source this $500 transfer from last February." It’s a full-blown financial colonoscopy, and it is exhausting. The entire time, I felt like I was on trial, just trying to prove I was worthy of their money. But the waiting was the worst part. Days crawled into weeks. The seller started getting nervous. I was a wreck. The whole ordeal, from signing the contract to getting the keys, took 55 agonizing days. Okay, let's get to the numbers, because that’s why you’re here. For the Bank Duplex: *Purchase Price:* $300,000 *Down Payment (25%):* $75,000 *Loan Amount:* $225,000 *Interest Rate:* I locked in at 7.5%, a pretty standard rate for an investment property. *Closing Costs:* About $9,000 for appraisal fees, loan origination, title insurance… all the lovely bank fees. *Total Cash Out-of-Pocket:* A staggering $84,000. My monthly payment—principal, interest, taxes, and insurance—is about $2,175. The property rents for $3,000 a month. So after setting aside money for vacancies, repairs, and management, my net cash flow is around $325 a month. It’s not bad. It’s a solid base hit. But it took almost two months, cost me $84,000 in liquid cash, and probably took a year off my life. There had to be a better way. *Section 2: The Seller Financing Story - The Path Less Traveled* A few months later, another duplex popped up, just a few blocks from the first one. We'll call this one "The Seller-Financed Duplex." The owner was an older guy who'd managed it himself for 30 years and was just... done. He didn't want the tenant headaches, but he also didn’t want to get slammed with a massive capital gains tax bill from a cash sale. He was a motivated seller, and that’s the key that opens the door to this whole strategy. Instead of writing up a standard offer, I had my agent ask one simple question: "Would the owner consider financing the deal for you?" And just like that, the game changed. This wasn't about filling out forms anymore; it was a conversation. The seller and I actually sat down and talked. He told me what he needed: a steady income for retirement. I told him what I wanted: to buy his property without draining my bank account. #realestate #poppahomes #beforeandafter

Comments

-

Трансляция закончилась 14 часов назад

Трансляция закончилась 14 часов назад

-

1 год назад

1 год назад

-

3 месяца назад

3 месяца назад

-

10 часов назад

10 часов назад

-

3 года назад

3 года назад

-

15 часов назад

15 часов назад

-

3 года назад

3 года назад

-

1 месяц назад

1 месяц назад

-

13 часов назад

13 часов назад

-

15 часов назад

15 часов назад

-

1 год назад

1 год назад

-

2 года назад

2 года назад

-

2 года назад

2 года назад

-

4 недели назад

4 недели назад

-

6 месяцев назад

6 месяцев назад

-

8 часов назад

8 часов назад

-

7 месяцев назад

7 месяцев назад

-

9 часов назад

9 часов назад

-

11 месяцев назад

11 месяцев назад

-

1 месяц назад

1 месяц назад