IAS 37 Accounting for Provisions and Contingent Liabilities скачать в хорошем качестве

IAS 37 Accounting for Provisions and Contingent Liabilities

6 часов назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: IAS 37 Accounting for Provisions and Contingent Liabilities в качестве 4k

У нас вы можете посмотреть бесплатно IAS 37 Accounting for Provisions and Contingent Liabilities или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон IAS 37 Accounting for Provisions and Contingent Liabilities в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

IAS 37 Accounting for Provisions and Contingent Liabilities

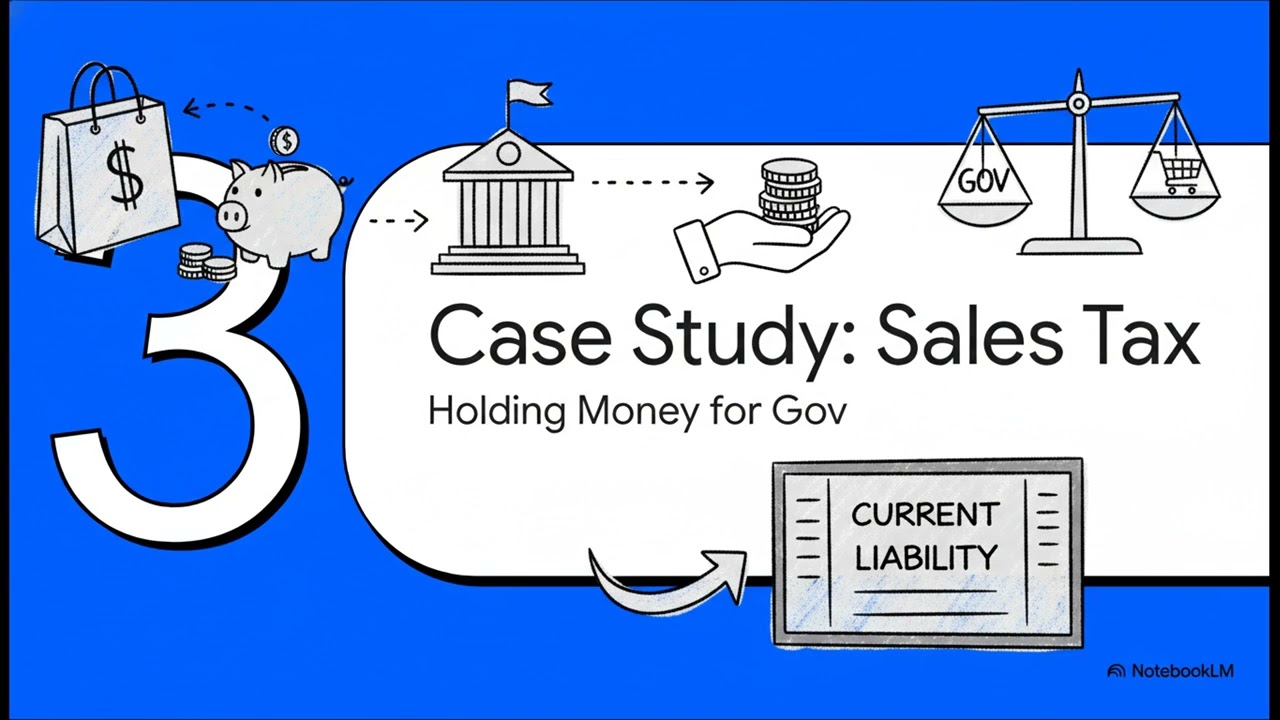

The video outlines the IAS 37 accounting standard, which establishes the framework for managing provisions, contingent liabilities, and contingent assets. A provision is defined as a debt with an unclear final cost or settlement date, distinguishable from standard payables by its inherent uncertainty. To record a provision, an organization must prove a present obligation resulting from a past event, show that a loss of funds is probable, and provide a reliable financial estimate. Conversely, contingent liabilities and assets represent potential obligations or gains that do not meet the strict criteria for formal recognition and are typically handled through financial disclosures. The documents also address specialized scenarios, such as onerous contracts—where costs outweigh benefits—and corporate restructuring plans. Measurement of these items often involves calculating a best estimate using statistical methods or assessing the present value of future cash flows.

Comments

-

3 года назад

3 года назад

-

2 года назад

2 года назад

-

6 часов назад

6 часов назад

-

22 часа назад

22 часа назад

-

3 часа назад

3 часа назад

-

21 час назад

21 час назад

-

4 месяца назад

4 месяца назад

-

7 дней назад

7 дней назад

-

Трансляция закончилась 14 часов назад

Трансляция закончилась 14 часов назад

-

10 часов назад

10 часов назад

-

11 дней назад

11 дней назад

-

15 часов назад

15 часов назад

-

5 дней назад

5 дней назад

-

1 день назад

1 день назад

-

1 год назад

1 год назад

-

2 месяца назад

2 месяца назад

-

9 часов назад

9 часов назад

-

1 месяц назад

1 месяц назад

-

5 месяцев назад

5 месяцев назад

-

6 часов назад

6 часов назад