How to Avoid a Short Sale in CA When you have Low Equity скачать в хорошем качестве

How to Avoid a Short Sale in CA When you have Low Equity

Трансляция закончилась 6 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: How to Avoid a Short Sale in CA When you have Low Equity в качестве 4k

У нас вы можете посмотреть бесплатно How to Avoid a Short Sale in CA When you have Low Equity или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон How to Avoid a Short Sale in CA When you have Low Equity в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

How to Avoid a Short Sale in CA When you have Low Equity

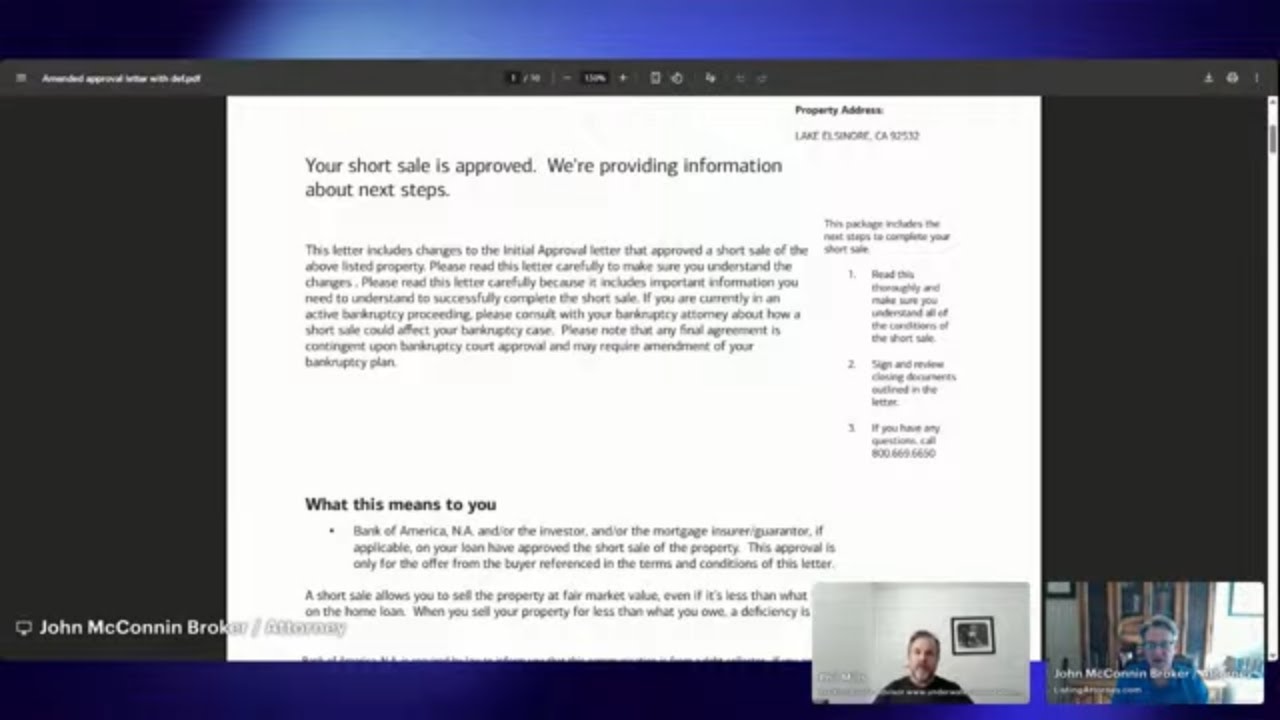

TL;DR – Summary Are you "upside down" or facing a low-equity sale in California? In this deep-dive, Phil Mills and Attorney-Broker John McConnin break down the Triad Analysis—a three-pronged strategy to manage your exposure to the Bank, the IRS/FTB, and credit damage. We show you how to leverage the California foreclosure timeline to stay in your home longer, save money, and exit on your own terms. The Triad Analysis: Our Three-Lens Approach We don't just "list" homes; we analyze your situation through three critical lenses to ensure you aren't walking into a financial ambush: Exposure to the Bank: Analyzing recourse vs. non-recourse debt and stopping deficiency judgments. Exposure to the IRS & Franchise Tax Board: Navigating the "phantom tax" of debt forgiveness and minimizing your capital gains liability. Credit Preservation: Strategic moves to minimize or improve the long-term damage to your credit profile. What You’ll Learn in This Video The California Timeline: How to use the law to stay in your house as long as possible while you save up for your next chapter. Leveraging the Law: Why standard real estate agents miss the legal nuances that can cost you thousands in statutory penalties or tax bills. The Attorney Advantage: Why your "listing agent" needs to be a legal advocate who understands CCP 580d and 580e People Also Ask (FAQ) Q: How long can I stay in my house after I stop paying? A: With the current California timeline and strategic use of listing periods, homeowners can often remain in the property for 10 months or more while planning their transition. Q: Will the IRS tax me on the money the bank "forgave"? A: It depends on the nature of the loans and the loan workout you choose. We look for ways to characterize that debt to avoid it being treated as ordinary income. Contact & Author Schema Host: John McConnin | john@listingattorney.com Location: San Diego, CA Credentials: Broker = Attorney | DRE # 01445675 | St Bar # 154852 Website: www. upsidedownrealestate.com

Comments

-

Трансляция закончилась 9 часов назад

Трансляция закончилась 9 часов назад

-

4 недели назад

4 недели назад

-

4 года назад

4 года назад

-

11 дней назад

11 дней назад

-

1 год назад

1 год назад

-

1 месяц назад

1 месяц назад

-

Трансляция закончилась 2 дня назад

Трансляция закончилась 2 дня назад

-

7 дней назад

7 дней назад

-

6 дней назад

6 дней назад

-

6 часов назад

6 часов назад

-

12 часов назад

12 часов назад

-

2 года назад

2 года назад

-

3 месяца назад

3 месяца назад

-

6 часов назад

6 часов назад

-

5 месяцев назад

5 месяцев назад

-

1 год назад

1 год назад

-

Трансляция закончилась 2 дня назад

Трансляция закончилась 2 дня назад

-

4 года назад

4 года назад

-

3 месяца назад

3 месяца назад

-

3 года назад

3 года назад