What are the biggest legal mistakes first-time homebuyers can make? скачать в хорошем качестве

What are the biggest legal mistakes first-time homebuyers can make?

4 месяца назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: What are the biggest legal mistakes first-time homebuyers can make? в качестве 4k

У нас вы можете посмотреть бесплатно What are the biggest legal mistakes first-time homebuyers can make? или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон What are the biggest legal mistakes first-time homebuyers can make? в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

What are the biggest legal mistakes first-time homebuyers can make?

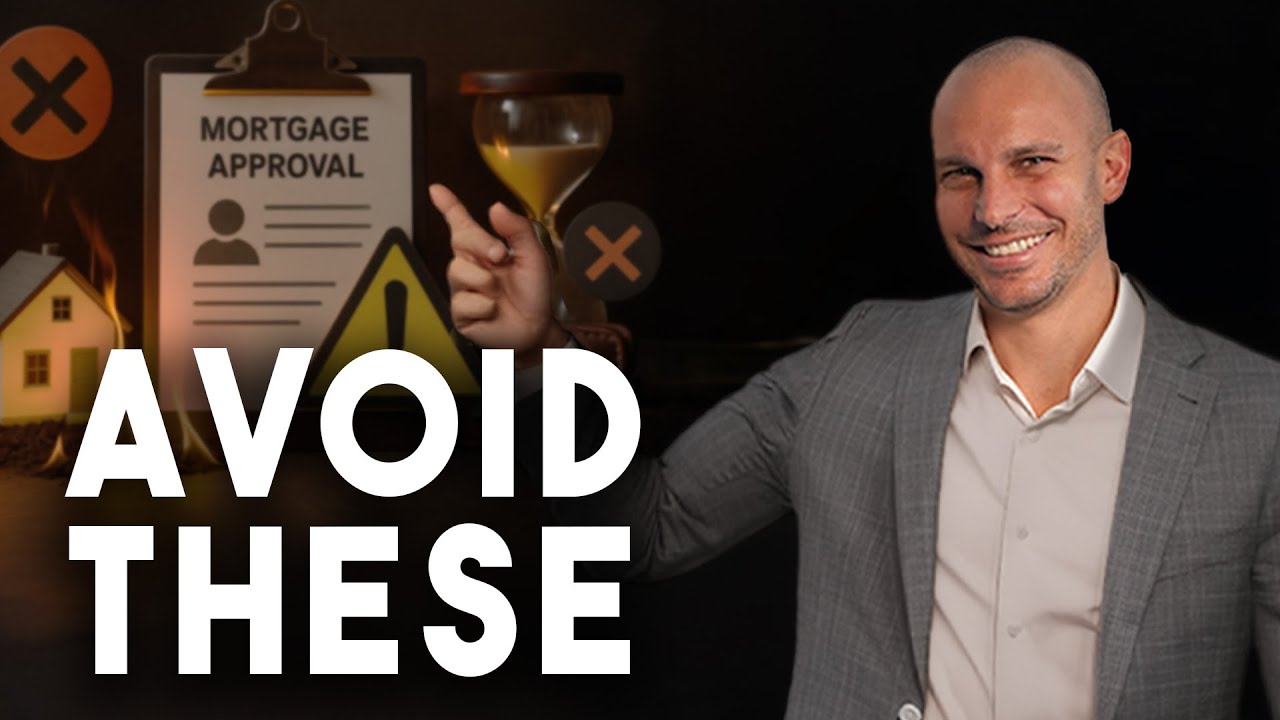

What are the biggest legal mistakes first-time homebuyers can make? Here’s the gist of Larry & Jerron’s chat on the biggest legal mistakes first-time homebuyers make. The pair say most blown deals (and legal headaches) trace back to financing and deadlines. Jerron leads with a common failure: buyers aren’t properly vetted by their lenders and accept financing contingencies that are too aggressive—think 15–20 days—so the lender can’t issue approval in time. If the buyer doesn’t timely cancel under that contingency, their escrow (earnest money) can be at risk. He and Larry emphasize that many lenders give only cursory pre-quals, which collapses deals later and exposes deposits. Larry sees buyers choose the wrong team—agent, lender, sometimes attorney—and then miss critical contract dates like loan commitment or inspection. When those dates pass unnoticed, the escrow can be jeopardized. He stresses that everyone on the buyer’s side must track deadlines obsessively to protect the deposit. Jerron agrees: job one is safeguarding escrow; closing comes a close second, but if a deal fails, you shouldn’t lose your deposit. They describe real-world pain: a buyer’s moving van waits on a Friday because the loan funds didn’t arrive at the closing office; the seller won’t release keys without proceeds, so the buyer is stuck for days. The cure? Work with the right lender and a responsive team of pros (agent, lender, inspectors, attorney) who hit dates and communicate. Larry adds that sellers actively vet buyers: he calls the agent and lender to see if they “have it together.” Red flags include a lender who won’t pick up the phone and an aloof or unknowledgeable agent—signals of potential failure or disputes. On lender choice, Jerron says that if two offers are otherwise equal, he’ll favor the buyer using a dedicated mortgage lender over a big brick-and-mortar bank. Large banks often have many hands on a file and blow through contractual deadlines, while mortgage-only lenders tend to move with more urgency. Finally, Larry reminds buyers to deliver all requested documents promptly so the lender can actually close on time—another simple way to keep deposits safe and keys on schedule.

Comments

-

Трансляция закончилась 14 часов назад

Трансляция закончилась 14 часов назад

-

1 день назад

1 день назад

-

3 недели назад

3 недели назад

-

2 дня назад

2 дня назад

-

3 дня назад

3 дня назад

-

2 недели назад

2 недели назад

-

1 месяц назад

1 месяц назад

-

Трансляция закончилась 3 дня назад

Трансляция закончилась 3 дня назад

-

7 дней назад

7 дней назад

-

11 дней назад

11 дней назад

-

12 часов назад

12 часов назад

-

-

13 дней назад

13 дней назад

-

15 часов назад

15 часов назад

-

7 дней назад

7 дней назад

-

Трансляция закончилась 46 минут назад

Трансляция закончилась 46 минут назад

-

10 дней назад

10 дней назад

-

Трансляция закончилась 1 день назад

Трансляция закончилась 1 день назад

-

-

![🔴 EXPRESS BIEDRZYCKIEJ | DR KATARZYNA KASIA, ROCH KOWALSKI [NA ŻYWO]](https://imager.clipsaver.ru/NFgUHinVQLc/max.jpg) Трансляция закончилась 30 минут назад

Трансляция закончилась 30 минут назад