3.6 (Macro) Demand-side policies (Fiscal): Crowding out: Partial & complete crowding out: IB Econ скачать в хорошем качестве

3.6 (Macro) Demand-side policies (Fiscal): Crowding out: Partial & complete crowding out: IB Econ

5 лет назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: 3.6 (Macro) Demand-side policies (Fiscal): Crowding out: Partial & complete crowding out: IB Econ в качестве 4k

У нас вы можете посмотреть бесплатно 3.6 (Macro) Demand-side policies (Fiscal): Crowding out: Partial & complete crowding out: IB Econ или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон 3.6 (Macro) Demand-side policies (Fiscal): Crowding out: Partial & complete crowding out: IB Econ в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

3.6 (Macro) Demand-side policies (Fiscal): Crowding out: Partial & complete crowding out: IB Econ

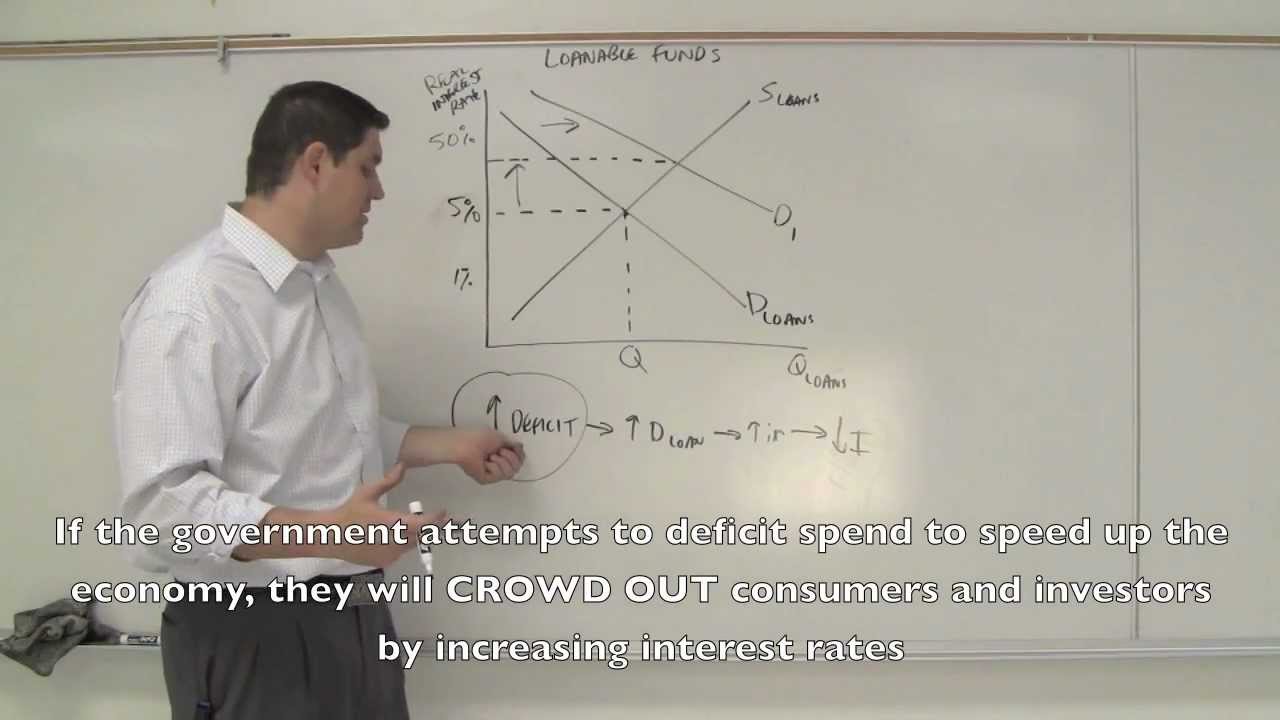

Video tutorial illustrating how to draw, analyze, & evaluate a limitation of expansionary fiscal policy called crowding out (partial crowding out & complete crowding out) using a money market & monetarist model. The demand-side policy applied leading to the increased AD is expansionary fiscal policy, which is closing an assumed recessionary gap. Demand side fiscal policies includes changes in income, corporate, &/or wealth taxes, as well as changes in government spending on public goods and services by the central government as a means to influence aggregate demand. Expansionary demand side fiscal policies would include the central government decreasing income taxes, corporate taxes, and/or wealth taxes as well as increasing government spending on public goods & services to encourage increased consumption & investment spending. The impact of increased government spending without increased tax revenue leads the central government to borrow funds thus leading to an increase in demand for money in the money market, which would raise interest rates. The rise in the interest rate would decrease household and firm borrowing and spending thus leading to partial or complete crowding out. Although this weakness of expansionary fiscal policy can be solved by coordination between the central government and central bank in which the central bank will increase the supply of money to maintain low interest rates and not crowd our consumption and investment spending. Note: IB Econ Paper analysis at time 8:15 ---------------------- Analysis: Expansionary fiscal policy (limitations in regards to the concept of crowding out) Graph A: Money market X-axis measures the quantity of money supplied & demanded Y-axis measures the rate of interest (value of money) Demand for money curve (Dm1) is downward sloping according to the law of demand Two perfectly inelastic supply of money curves (Sm1 & Sm2), since at any one point in time there is a fixed quantity of money in circulation Graph B: Expansionary fiscal policy leading to partial crowding out X-axis measures real GDP Y-axis measures price level (PL) Aggregate Demand 1=AD1=C+I+G+(X-M) AD is downward sloping: wealth effect, interest rate effect, & international trade effect Short Run Aggregate Supply 1=SRAS1 SRAS is upward sloping since as the PL rises with costs of production held constant in the short-run, the profit margin for firms increases thus increasing the incentive for firms to increase the quantity of output supplied SRAS1=AD1 (point C), provides the equilibrium PL at PL1 & equilibrium level of output at Y1 -------------- Graph A Dm1=Sm1 (Point A) provides an equilibrium rate of interest of IR1, & an equilibrium quantity supplied (Qs) & quantity demanded (Qd) of money at Qm1 ------------- Graph B The central government engages in an expansionary fiscal policy (a demand-side policy), perhaps as a result of the national economy being in a recessionary gap The central government, deciding to not decrease income &/or corporate &/or wealth taxes decides to increase government spending The central government will engage in budget deficit spending, & increase demand for money to be borrowed in the money market ------------- Graph A Increase demand for money Dm1 to Dm2 by the central government (point A to point B) Equilibrium interest rate rises from IR1 to IR2, with Qm constant at Qm1 ------------- Graph B With increased borrowed funds, the central government is able to increase government (G) spending, thus leading to AD shifting out from AD1 to AD2 Expansionary fiscal policy leads to increased real GDP from Y1 to Y2 Increased quantity of SRAS (point C to D), leads to firms employing more inputs (resources) in order to increase quantity of outputs supplied (Y1 to Y2) PL rises from PL1 to PL2 (demand pull inflation) ------------ Partial crowding out: But increased interest rates in the money market, crowds out the ability of households & firms to borrow funds cheaply There is reduced borrowing (financial capital) by households & firms leading to reduced consumption (C) & investment (I) spending AD decreases from AD2 to AD3 Reduced real GDP from Y2 to Y3 Reduced quantity of SRAS, point D to E (firms fire excess resources causing unemployment to rise) PL falls from PL2 to PL3 (deflation) ------------- Complete crowding out: AD2 decreases back to AD1 ------------- Crowding out can be avoid through coordination between the central government & central bank Increased demand in the money market by the central government (Dm1 to Dm2), can be offset through increased supply of money by the central bank: Sm1 to Sm2 (Qm2) to maintain IR1

Comments