Income Statement Explained: Comprehensive Income Statement Tutorial | Profit & Loss Statement скачать в хорошем качестве

Income Statement Explained: Comprehensive Income Statement Tutorial | Profit & Loss Statement

10 лет назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Income Statement Explained: Comprehensive Income Statement Tutorial | Profit & Loss Statement в качестве 4k

У нас вы можете посмотреть бесплатно Income Statement Explained: Comprehensive Income Statement Tutorial | Profit & Loss Statement или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Income Statement Explained: Comprehensive Income Statement Tutorial | Profit & Loss Statement в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Income Statement Explained: Comprehensive Income Statement Tutorial | Profit & Loss Statement

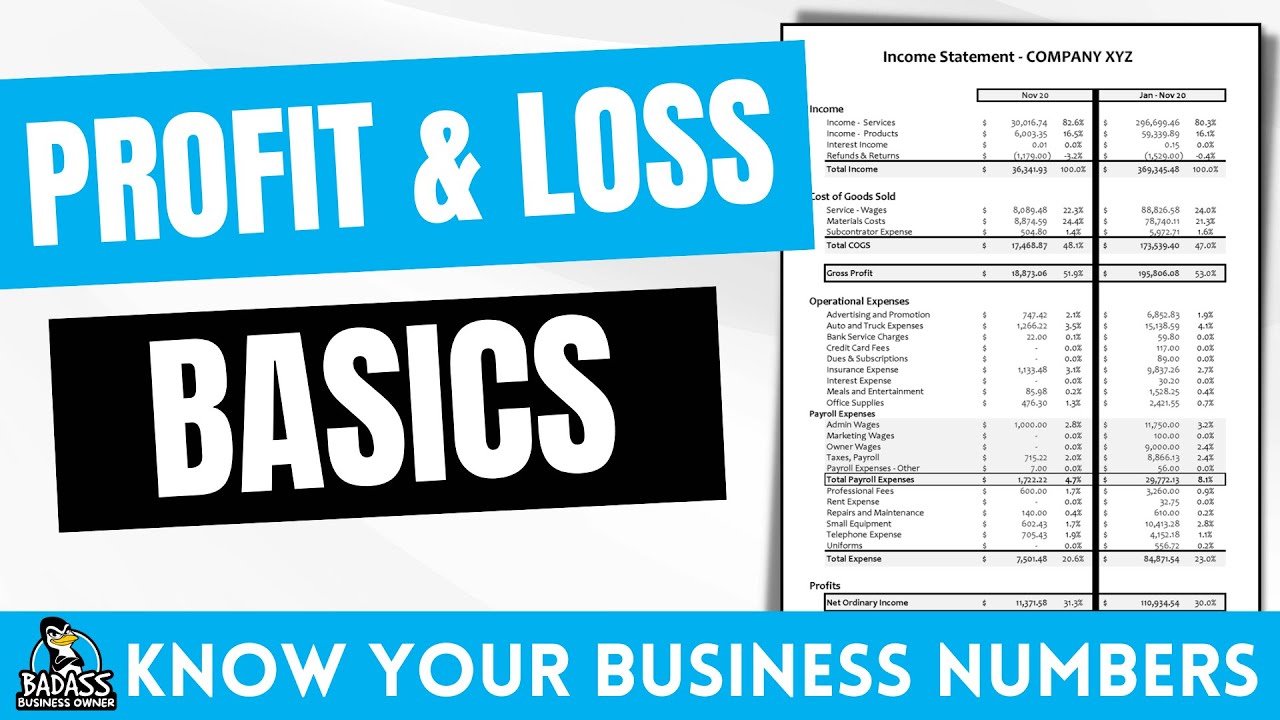

Get more in-depth lessons via Axel's Accofina books: (1) Financial Statement Basics https://www.amazon.com/Financial-Stat... (2) Ratio Analysis Fundamentals https://www.amazon.com/Ratio-Analysis... Income Statement Explained: Comprehensive Income Statement Tutorial - Profit & Loss Statement The Income Statement (aka Profit & Loss Statement) is one of the 4 Main Financial Statements. The income statement is one of the primary outputs of a financial accounting system. The four major financial accounting reports are: 1) Income Statement 2) Balance Sheet 3) Cash Flow Statement 4) Statement of Changes in Equity The income statement is a performance report. The income statement measures the performance of a business over a set time period based on its ability to earn profits over that set period. While a balance sheet (another key financial statement) shows a snapshot 'picture' in time, e.g. 21-Nov-2014, the income statement more closely resembles a ‘video’ as it measures performance over a set time period, e.g. 1-Jan-16 through 31-Dec-16. Note: the period need not be a year, it may be a month, quarter, half-year, etc. How does it measure performance over set period? In short: It tells you whether you made a Profit (Net Income) over the accounting period. It tells you whether your Revenue was higher than your Expenses. That is, Revenue - Expenses = Net Income (aka Profit) Specifically, it aggregates all sales and service revenue over the set period to create an Revenue (or income) figure. Then it lists all the major expenses throughout the same period and groups them into easily understood accounts, e.g. admin expenses, marketing expenses, etc. We then subtract the total expenses figure from the total revenue figure and what is remaining is that period’s ‘net income’ (if the figure is positive) or ‘net loss’ (if the figure is negative). Ideally a business wants to have net income. The benefits of income statement analysis are driven from how each line item, these being ‘accounts’ or sub-totals, shown in the income statement is used for further enquiry or action. For instance, you can analyse the ratio of net income to revenue to work out the profit margin, or you can analyse expenses over a number of income statements and see how expenses are growing or shrinking and make assumptions about management’s cost control. You may have just noticed how I mentioned that line items might be sub-totals (and not expense or income accounts). This is important to grasp as these sub-totals are also used for analysis. The idea is that the income statement is simply not just three lines: (1) revenue (2) expenses (3) net income. Instead the income statement has a number of sub-totals throughout (although they can change depending on the format of the document). This common income statement breakdown is called a 'Multi-Step' Income Statement. Now depending on the type and size of business, you may find all the following 'steps' in this common format: First you start with Revenue, then go to Gross Profit, then Operating Profit, followed by Income Before Tax before you reach what is termed "The Line", which is Income from Continuing Operations. And after some final adjustments after 'The Line', you will end up at Net Income, aka 'The Bottom Line'. If you have read this far, thanks(!), the simplest formula of the Income Statement is just: Revenue - Expenses = Net Income. And remember, the Income Statement, itself, has a variety of different names. You may hear the Income Statement being called the Profit and Loss Statement or the Statement of Operations, or the Statement of Earnings, or the Statement of Profit and Loss, or (as I was first taught) the Statement of Financial Performance. JUST REMEMBER: they are all the SAME document, they all refer to the same type of Income Statement document. It just a confusing quirk that often depends on where the business is located, how large and complex the business is or how old the statement was, i.e the name has often been changed by the Accounting Standard organisations in a short period of time. Finally, you may ask why this report is even produced? No, it's not just as an academic exercise or so we can give the statement to somebody who requests it. The Income Statement, like the others, allows external investors, creditors, employees, governments and other stakeholders a window inside the organisation. They can get a view of the company that may otherwise be limited to management or other internal stakeholders. With this view: They can make better economic decisions(!) For example, should I invest in, or lend to, this company? How much should I tax this company? What wage demands should we make? How is this company performing in comparison to my own? Etc. KEYWORDS: Income Statement, Profit & Loss Statement, Financial Statements, Financial Reporting, Accounting

Comments