Phantom Income: Why Your Syndication Investors Could Owe Taxes With No Cash in Hand скачать в хорошем качестве

Phantom Income: Why Your Syndication Investors Could Owe Taxes With No Cash in Hand

7 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Phantom Income: Why Your Syndication Investors Could Owe Taxes With No Cash in Hand в качестве 4k

У нас вы можете посмотреть бесплатно Phantom Income: Why Your Syndication Investors Could Owe Taxes With No Cash in Hand или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Phantom Income: Why Your Syndication Investors Could Owe Taxes With No Cash in Hand в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Phantom Income: Why Your Syndication Investors Could Owe Taxes With No Cash in Hand

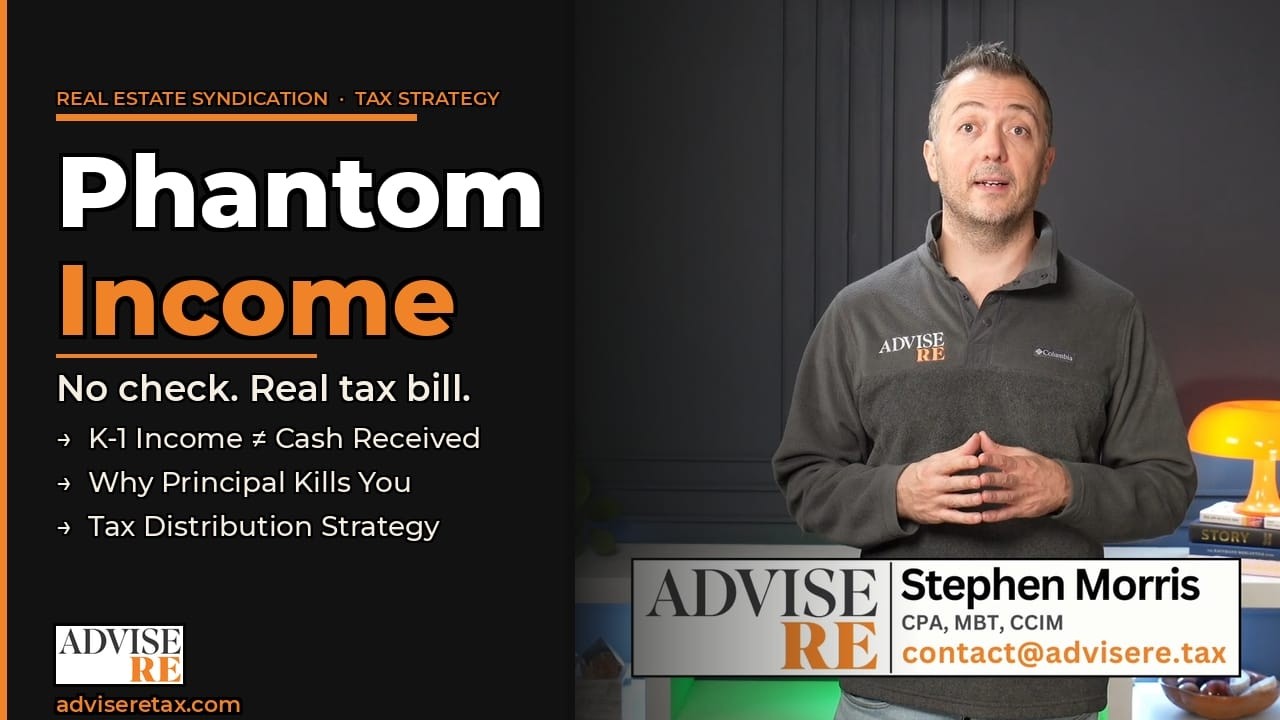

Your investor gets a K-1 showing $10,000 of rental income. They never received a check. Now they owe $3,700 in taxes — and they're calling you. This is phantom income, and it's one of the most common — and most avoidable — surprises in real estate syndications. In this video, Stephen Morris (CPA, MBT, CCIM) breaks down exactly how phantom income happens, why principal payments are the root cause, and the cash management strategy every syndicator should implement from day one to protect investor relationships. 📌 What you'll learn: What phantom income is and how it shows up on a K-1 Why principal paydown creates taxable income without cash How depreciation eventually runs out — and what happens next The tax distribution strategy: how to hold back reserves the right way Why investor memory is short and your planning needs to be long How to protect your reputation and keep investors coming back for the next deal --- ❓ FREQUENTLY ASKED QUESTIONS: Q: What exactly is phantom income in a real estate syndication? A: Phantom income occurs when a K-1 reports taxable income to an investor that exceeds the actual cash they received as a distribution. The investor owes real taxes on income they never saw in their bank account. Q: Why does this happen? A: The primary culprit is debt principal paydown. Mortgage principal payments reduce the loan balance (building equity) but are not tax deductible. So even when all operating cash is consumed by debt service, the IRS sees a portion of that as income. Q: When does phantom income typically appear? A: Usually in the middle-to-later years of a hold, after accelerated depreciation has been used up. In early years, depreciation often shelters income or creates losses. Once that shield is gone and the property is performing well, taxable income can spike above distributions. Q: What is a tax distribution? A: A tax distribution is cash reserved and distributed to investors specifically to cover their tax liability on K-1 income. Rather than distributing 100% of available cash flow each month, a well-run syndicator holds back a portion and distributes it at year-end or tax season to cover investor tax bills. Q: How much should I hold back for tax distributions? A: It depends on your projections, but a common approach is to model the expected taxable income per investor unit, estimate their tax liability at the highest marginal rate (37% federal), and ensure that amount is available in reserves. Working with a CPA to forecast this annually is essential. Q: Is phantom income disclosed in the PPM? A: It should be. If you're a syndicator, your Private Placement Memorandum should disclose the risk of phantom income to investors. Failure to do so can create legal exposure. Talk to your securities attorney. Q: Can investors deduct syndication losses to offset phantom income in other years? A: Potentially, depending on their passive activity status. Real Estate Professionals (REPs) may have more flexibility. This is highly individual — investors should consult their own CPA. --- 🏢 Syndicating deals or investing in syndications and need tax guidance? Reach out at 👉 adviseretax.com 🔔 Subscribe for real estate tax and syndication strategy: @advisere --- TAGS: phantom income real estate, real estate syndication taxes, K-1 phantom income, tax distribution syndication, real estate partnership taxes, passive income K-1, real estate CPA, syndication investor taxes, principal paydown tax, real estate depreciation, Stephen Morris CPA, Advise RE, real estate investing taxes, partnership K-1 explained, syndicator tax planning

Comments