How to Retire Before 65 Without Going Broke on Healthcare скачать в хорошем качестве

How to Retire Before 65 Without Going Broke on Healthcare

2 дня назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: How to Retire Before 65 Without Going Broke on Healthcare в качестве 4k

У нас вы можете посмотреть бесплатно How to Retire Before 65 Without Going Broke on Healthcare или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон How to Retire Before 65 Without Going Broke on Healthcare в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

How to Retire Before 65 Without Going Broke on Healthcare

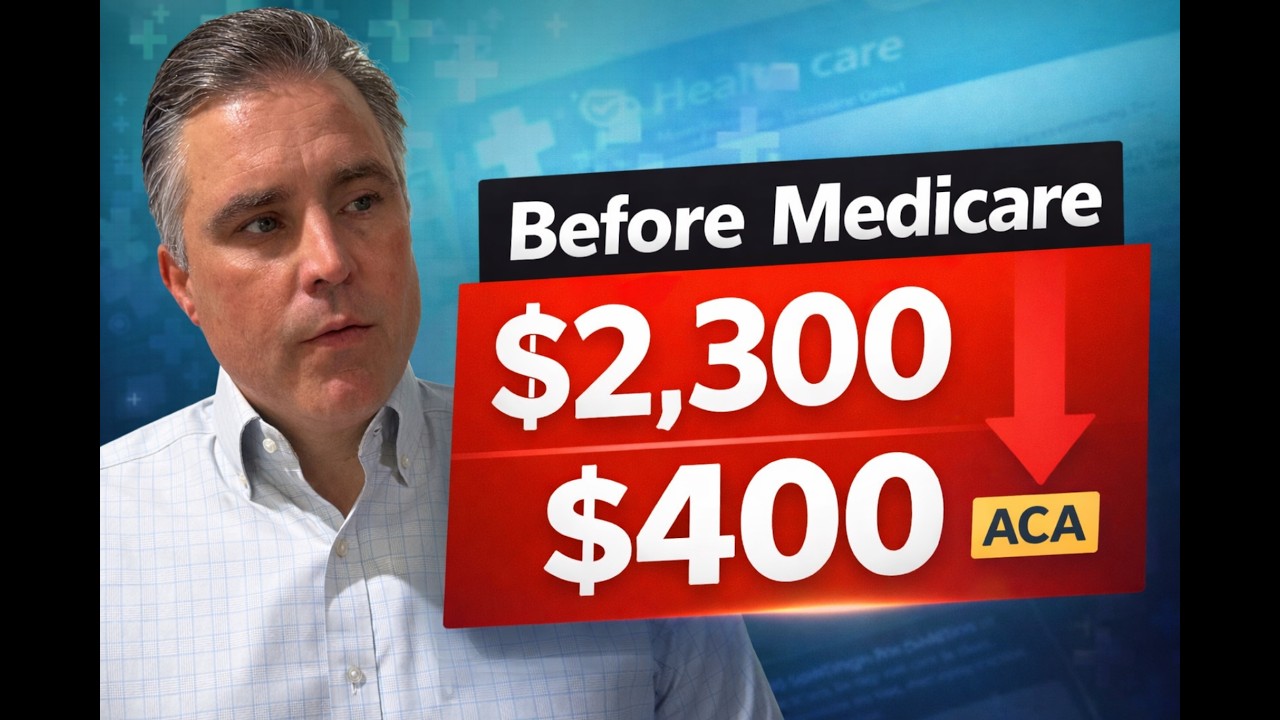

📅 Want Help Evaluating Your Own Retirement Readiness? If you have questions about your specific situation, you can schedule a complimentary 30-minute conversation using the link below. 👉 https://retirementwealthpro.com/contact Many people delay retirement for one reason: Healthcare. A lot of people assume that if they retire before Medicare starts at 65, they’ll have to pay $2,000–$3,000 per month for health insurance. But that isn’t always the case. In this video, I walk through a real retirement planning example showing how a couple retiring at age 62 was able to reduce their health insurance cost from roughly $2,300 per month to around $400 per month by coordinating their retirement income properly. The key is understanding how Affordable Care Act (ACA) subsidies work — and how retirement income planning can determine whether you qualify. Many retirees don’t realize that ACA subsidies are based on income, not how much money you have saved. That means two people with the exact same net worth could pay dramatically different healthcare premiums depending on how they structure their withdrawals. In this video we cover: • Why healthcare stops many people from retiring early • How ACA healthcare subsidies actually work • Why retirement income planning matters before Medicare • A real example showing how premiums dropped from $2,300/month to about $400/month • Why Roth conversions may not make sense during the pre-Medicare window For people retiring before Medicare, thoughtful planning during these few years can potentially save tens of thousands of dollars in healthcare costs. If healthcare costs are one of the reasons you’re hesitant to retire, this is an important strategy to understand. Retirement Wealth Pro (RWP) is not affiliated with or endorsed by the Social Security Administration, Medicare, the Security Exchange Commission (SEC), or any other government agency. RWP does not provide tax, estate, or legal advice. Consult with your tax, estate, or legal professional prior to making any financial decisions for your personal situation. Investment advisory services offered through CreativeOne Wealth, LLC, a Registered Investment Adviser. Retirement Wealth Professionals and CreativeOne Wealth are unaffiliated entities. We are not affiliated with or endorsed by the Social Security Administration, Medicare, the Security Exchange Commission (SEC), or any government agency. RWP does not provide tax, estate or legal advice.

Comments

-

16 часов назад

16 часов назад

-

11 часов назад

11 часов назад

-

1 месяц назад

1 месяц назад

-

Трансляция закончилась 4 дня назад

Трансляция закончилась 4 дня назад

-

1 час назад

1 час назад

-

2 недели назад

2 недели назад

-

3 часа назад

3 часа назад

-

2 часа назад

2 часа назад

-

Трансляция закончилась 21 час назад

Трансляция закончилась 21 час назад

-

1 день назад

1 день назад

-

3 дня назад

3 дня назад

-

2 дня назад

2 дня назад

-

Трансляция закончилась 1 день назад

Трансляция закончилась 1 день назад

-

1 день назад

1 день назад

-

12 часов назад

12 часов назад

-

3 недели назад

3 недели назад

-

5 часов назад

5 часов назад

-

1 день назад

1 день назад

-

12 часов назад

12 часов назад

-

1 день назад

1 день назад