Efficient Frontier in Excel (2 Stocks): Build a Minimum Variance Portfolio Step-by-Step скачать в хорошем качестве

Efficient Frontier in Excel (2 Stocks): Build a Minimum Variance Portfolio Step-by-Step

4 дня назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Efficient Frontier in Excel (2 Stocks): Build a Minimum Variance Portfolio Step-by-Step в качестве 4k

У нас вы можете посмотреть бесплатно Efficient Frontier in Excel (2 Stocks): Build a Minimum Variance Portfolio Step-by-Step или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Efficient Frontier in Excel (2 Stocks): Build a Minimum Variance Portfolio Step-by-Step в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Efficient Frontier in Excel (2 Stocks): Build a Minimum Variance Portfolio Step-by-Step

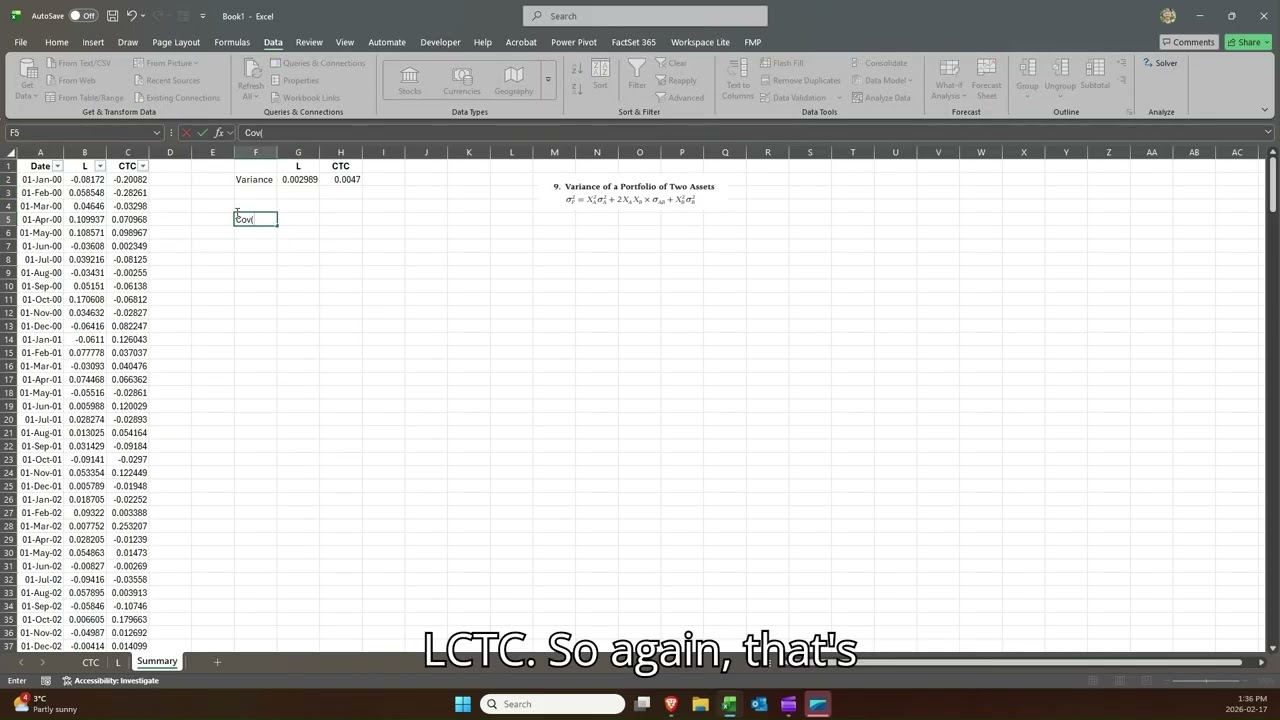

In this step-by-step Excel tutorial, you’ll learn how to construct the efficient set (efficient frontier) of a two-asset portfolio using real historical stock data. We download monthly price data from Yahoo Finance for Canadian Tire (CTC.A) and Loblaw (L.TO), clean the data in Excel, calculate monthly returns, and then compute: Variance Covariance Correlation Portfolio variance Portfolio standard deviation Expected (average) returns From there, we use Excel’s Data Table (What-If Analysis) to generate portfolio risk across weights from 0% to 100%, identify the minimum variance portfolio, and graph the efficient frontier using a scatter plot of risk vs. return. This tutorial walks through: ✔ Downloading and cleaning historical data ✔ Using Adjusted Close prices ✔ Calculating monthly returns ✔ Using Excel functions (VAR.S, COVARIANCE.S, CORREL, AVERAGE) ✔ Building the two-asset portfolio variance formula manually ✔ Finding the minimum variance weight ✔ Plotting the efficient frontier ⚠️ Disclaimer This video is for educational purposes only. The securities discussed (Canadian Tire and Loblaw) are used strictly as examples to demonstrate portfolio construction techniques in Excel. This content does not constitute investment advice, financial advice, or a recommendation to buy or sell any security. Always conduct your own research or consult a qualified financial professional before making investment decisions.

Comments