🏫From Non-Stationary to Stationary: How ADF Tests Guide Your Time Series Models🤗 скачать в хорошем качестве

🏫From Non-Stationary to Stationary: How ADF Tests Guide Your Time Series Models🤗

4 дня назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: 🏫From Non-Stationary to Stationary: How ADF Tests Guide Your Time Series Models🤗 в качестве 4k

У нас вы можете посмотреть бесплатно 🏫From Non-Stationary to Stationary: How ADF Tests Guide Your Time Series Models🤗 или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон 🏫From Non-Stationary to Stationary: How ADF Tests Guide Your Time Series Models🤗 в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

🏫From Non-Stationary to Stationary: How ADF Tests Guide Your Time Series Models🤗

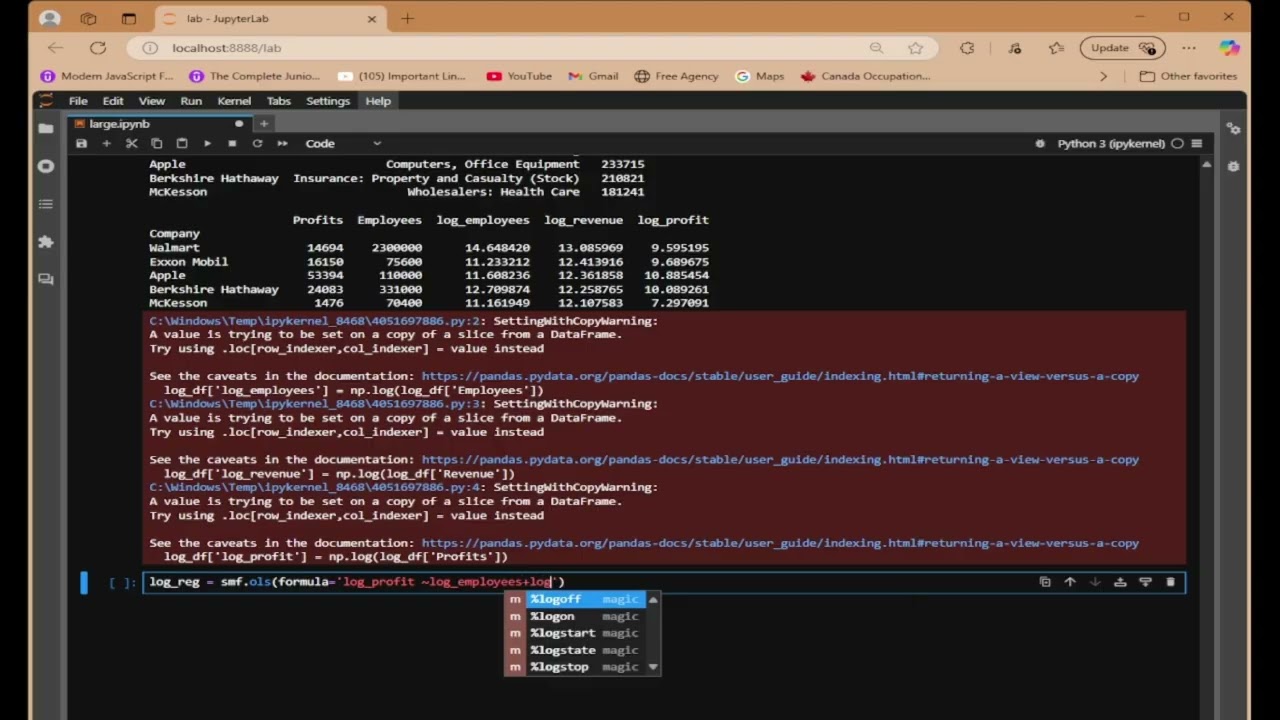

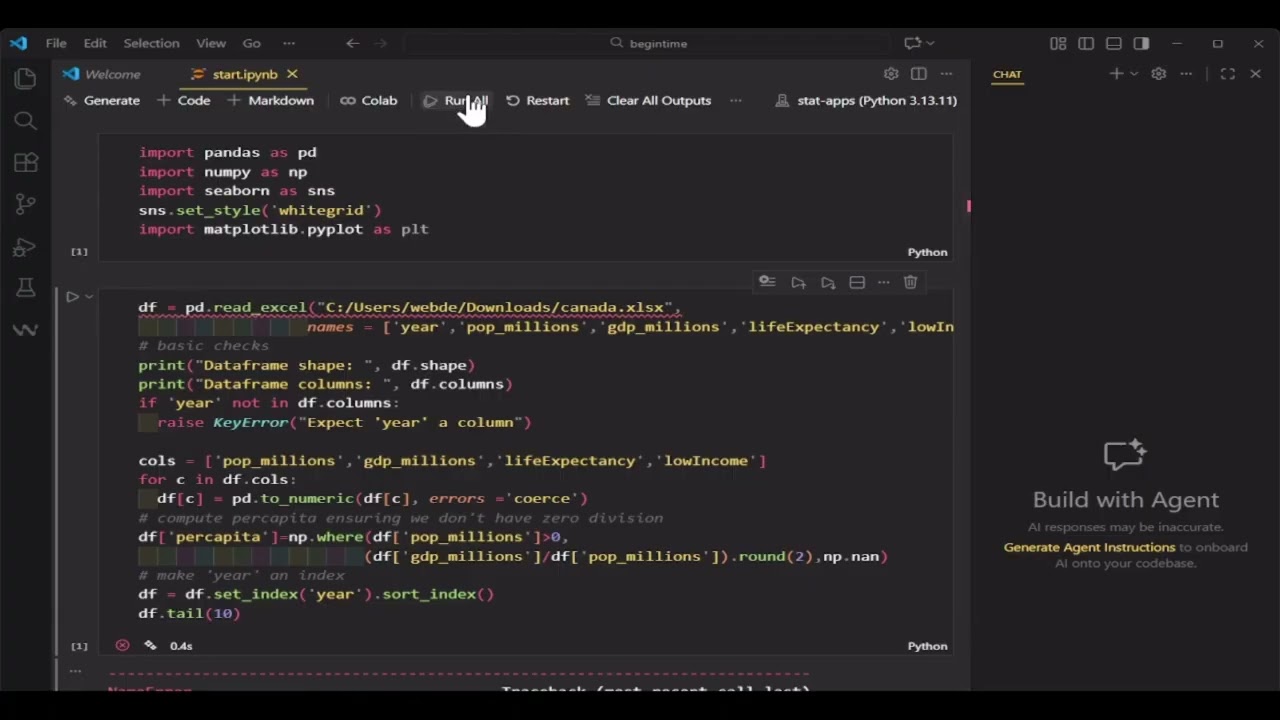

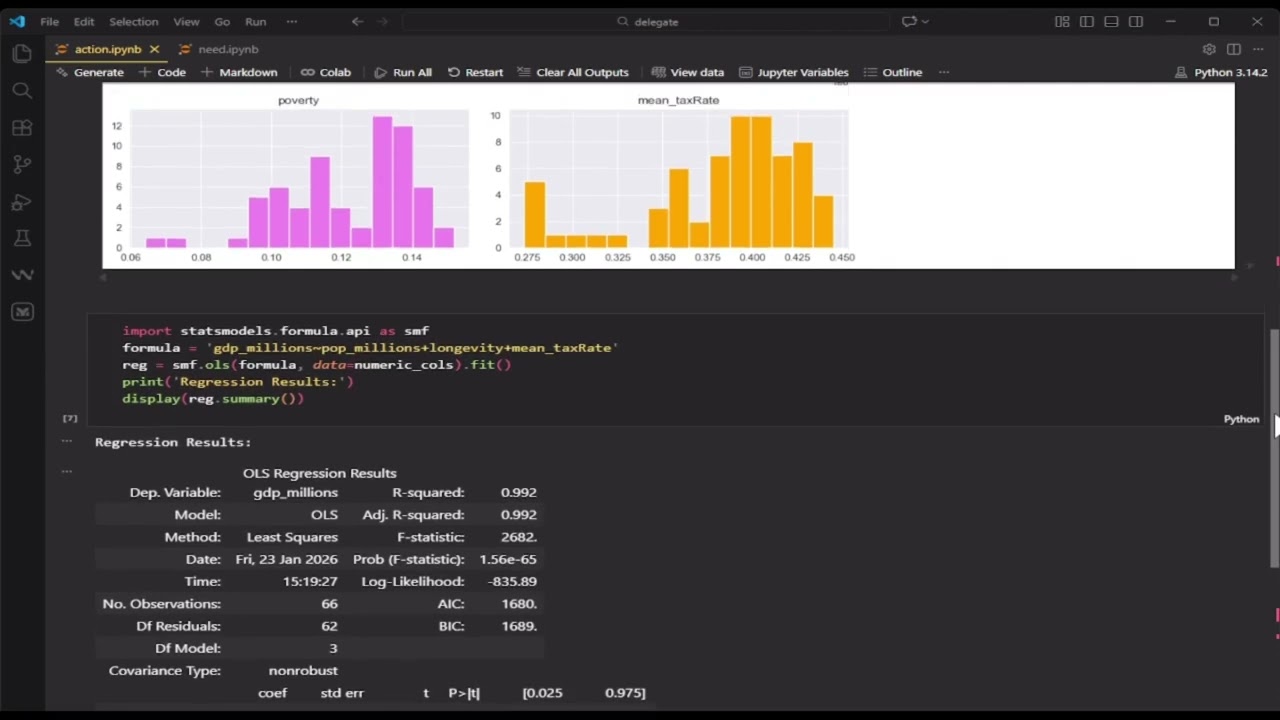

"Understanding and applying the Augmented Dickey-Fuller (ADF) test to ensure model validity in time series analysis. This notebook demonstrates a systematic approach to testing for stationarity: first running ADF tests on level variables to identify non-stationary series, then applying first differencing to achieve stationarity. Learn to interpret ADF results through two complementary methods—direct p-value evaluation and critical value comparison—ensuring your regression models are free from spurious autocorrelation. Perfect for econometricians and data scientists who need to validate their time series models before drawing statistical inferences." Full code available here: "https://github.com/webdev408/-Augment..." Please comment - I read all of them and answer as soon as possible. Your comments are guidelines for me.🙏 🙇Please subscribe and like the channel so that you have a reliable source to learn statistics, econometrics for data science and machine learning.👍

Comments