How is Property divided upon separation: Equalization basics Part 2 скачать в хорошем качестве

How is Property divided upon separation: Equalization basics Part 2

2 года назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: How is Property divided upon separation: Equalization basics Part 2 в качестве 4k

У нас вы можете посмотреть бесплатно How is Property divided upon separation: Equalization basics Part 2 или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон How is Property divided upon separation: Equalization basics Part 2 в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

How is Property divided upon separation: Equalization basics Part 2

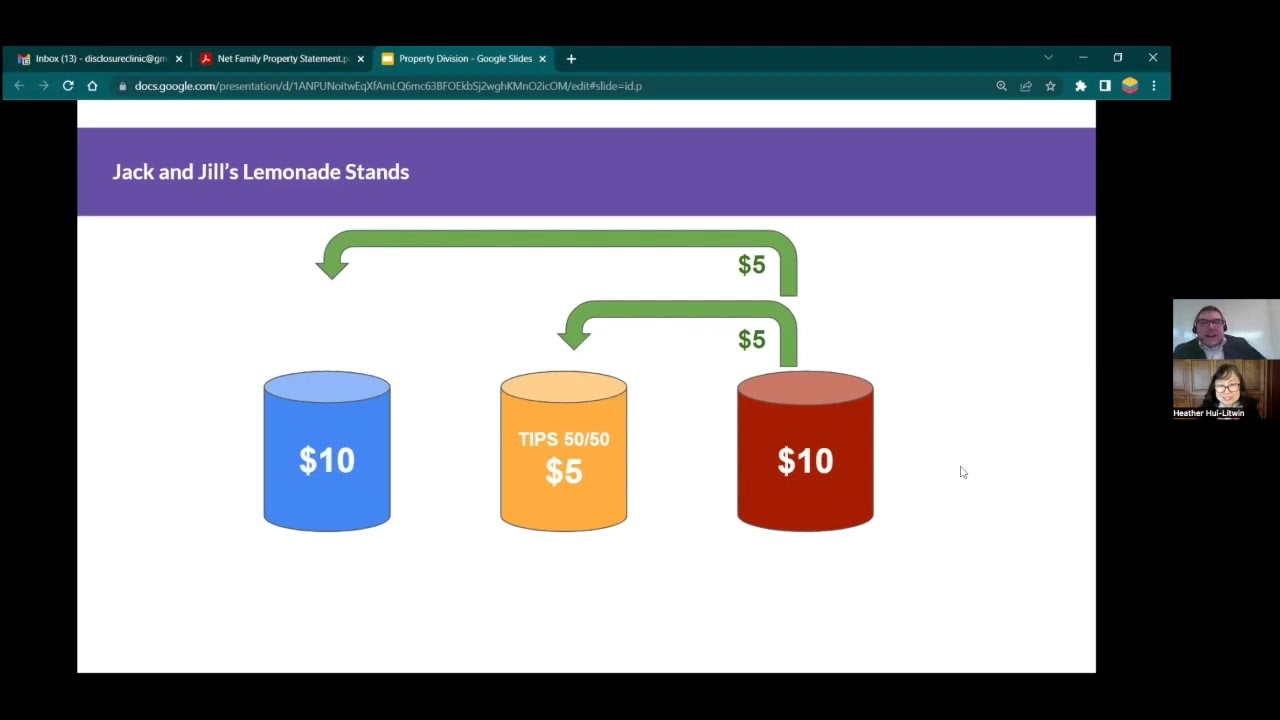

This video explains the law for property division between married couples. It also covers how to fill out the financial statement and Form 13B. Missed Part 1? Click here: • How is property divided upon separation? E... Timemarks 0:13 The Family Law Act presumes that each party intends to share the growth of their property during the marriage, using an equalization calculation based on the financial statement. 1:53 We need to know each party's net worth at the date of marriage and the valuation date. 2:15 Jack's net worth is $10 at the date of marriage and he had $12.5 at the valuation date. The growth of Jack's property is $12.5-$10=$2.5. 3:28 Quirk 1: Exclusion: Personal gifts should be deducted from the net worth at the valuation date. Therefore, $5 must be deducted from Jack's net worth at the valuation date as it was a gift from a third party 4:30 Inherited money can be deducted, but it must be proven that the money still exists at the valuation date (by tracing). 5:48 Quirk 2: Less than Zero = Zero: If a spouse's net family property is less than zero, it shall be deemed to be equal to zero. No negative net worth. Jack's net family property is -$2.5, but it is deemed to be zero. 6:26 Quirk 3: No Matrimonial Home Deduction: The value of the matrimonial home is not deducted from a spouse's net family property as a date of marriage asset. In this scenario, the stand is considered a matrimonial home. Jill's net family property was $72.5 at the valuation date and $20 at the marriage date; therefore she was sharing the entire value of the stand, not just its growth during the marriage. 8:16 The principle of No Matrimonial Home Deduction is controversial, possibly reflecting the legislation's intent to recognize shared ownership of the matrimonial home. 9:59 To conclude, the three quirks are: Exclusion, Less than Zero = Zero, and No Matrimonial Home Deduction. "Less than zero" is rare but occurs, typically in short-term marriages, while "Exclusion" applies generally in long-term relationships. 10:56 The net family property is calculated as the net worth at the valuation date minus the net worth at the marriage date. Jack's net family property is $0, while Jill's is $52.5. 11:02 Equalization payment: The spouse with the larger net family property must pay the other party half of the difference. Jill must pay Jack half the difference between their net worth, which is ($52.5 - $0)/2 = $26.25. 11:58 Jack ends up with $33.75: $26.25 (equalization payment) + $5 (from Pete) + $2.5 (from joint accounts). Jill had $48.5: $72.5 - $26.25 (equalization payment) + $2.5 (from joint accounts). 13:19 One takeaway is that calculations for married couples rely on specific data points, making the process straightforward mathematically. In contrast, unjust enrichment is fair but difficult to calculate over time due to varied fact patterns. 15:12 Equalization calculations presume couples share the growth of property, comforting those who take on non-monetary roles within the marriage. 15:37 Explaining how to fill out the financial statement. 15:54 Part 4(c) of the financial statement might be confusing, but its purpose is to collect data points by listing properties and calculating their values. 16:48 Certain properties, like debts, real property, and pensions, often require professional valuation or appraisal. 17:19 Liabilities such as current or future tax liabilities, contingent liabilities (e.g., as a guarantor), and other disposition costs also require formal valuation or appraisal. Most typical one is pension, which require formal valuation or appraisal as they might have tax liabilities. 18:09 Introducing Form 13B, which is designed to gather all assets and liabilities data at the date of marriage and the valuation date. 19:45 Unmarried couples do not use Form 13B as equalization does not apply to them. 19:57 In some provinces, such as British Columbia, equalization calculations are imposed on unmarried couples if they have lived together in a marriage-like relationship for two or more years. 20:40 There is ongoing debate about whether Ontario should apply equalization calculations to common-law partners. One view is that the consequences of marriage should not be imposed on those who choose not to marry. Another view is that calculating unjust enrichment in long-term relationships is costly, and equalization calculations provide certainty; therefore, the equalization approach should be adopted. Warning: The videos on Litigation Help are intended to provide general legal information only. They are not substitutes for legal advice from a legal professional. If you require legal help, please consult a professional directly Speakers Shmuel Stern Disclosureclinic.com Heather Hui-Litwin Litigation-help.com Thanks to S. Jian (J.D. Candidate) for creating the timemarks!

Comments