Portfolio Risk and Return – Part II (2025 Level I CFA® Exam – PM – Module 2) скачать в хорошем качестве

Portfolio Risk and Return – Part II (2025 Level I CFA® Exam – PM – Module 2)

3 года назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Portfolio Risk and Return – Part II (2025 Level I CFA® Exam – PM – Module 2) в качестве 4k

У нас вы можете посмотреть бесплатно Portfolio Risk and Return – Part II (2025 Level I CFA® Exam – PM – Module 2) или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Portfolio Risk and Return – Part II (2025 Level I CFA® Exam – PM – Module 2) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Portfolio Risk and Return – Part II (2025 Level I CFA® Exam – PM – Module 2)

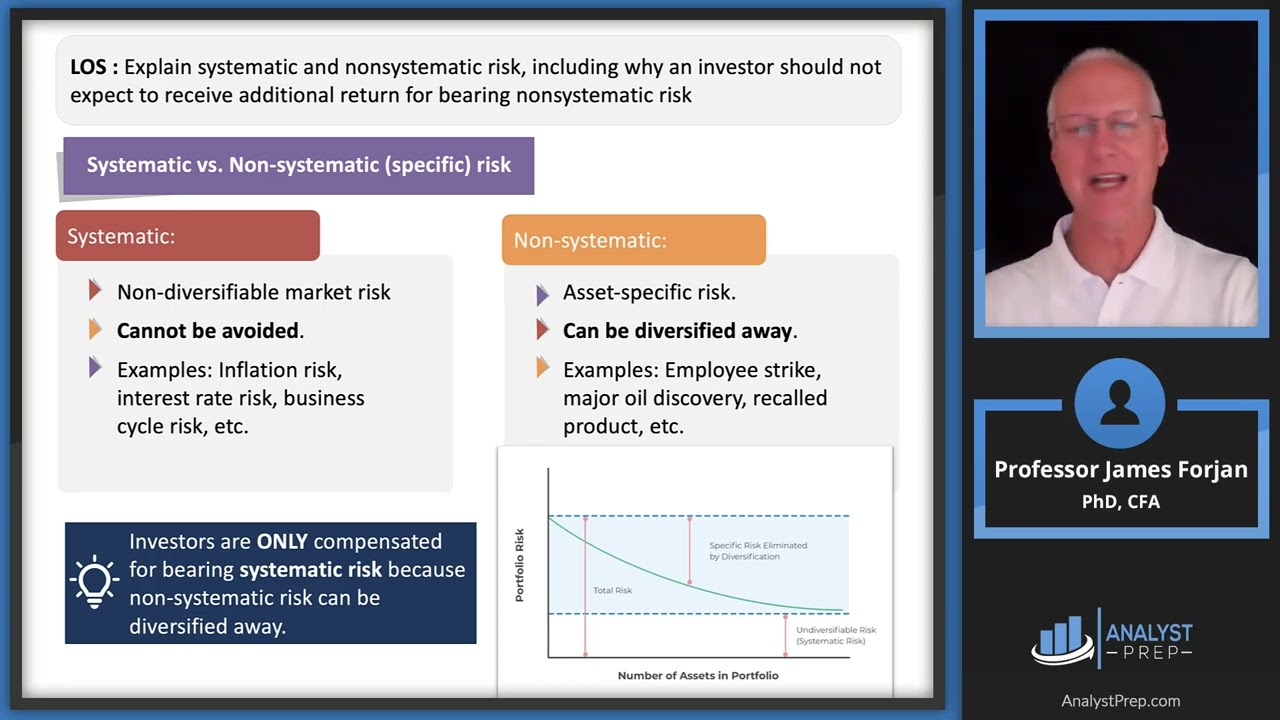

Master Portfolio Risk & Return – Part II (CFA Level I | Portfolio Management). This lesson links the efficient frontier to the CAL/CML, explains systematic vs. nonsystematic risk, builds intuition for beta, and applies CAPM and the Security Market Line to security selection. We finish with performance evaluation: Sharpe, Treynor, M², and Jensen’s alpha for exam readiness. Study with AnalystPrep: Level I: https://analystprep.com/shop/cfa-leve... Level II: https://analystprep.com/shop/learn-pr... Levels I, II & III (Lifetime access): https://analystprep.com/shop/cfa-unli... Prep Packages for the FRM® Program: FRM Part I & Part II (Lifetime access): https://analystprep.com/shop/unlimite... Topic 9 – Portfolio Management Module 2 – Portfolio Risk and Return – Part II 0:00 Introduction and Learning Outcome Statements 4:45 LOS : Describe the implications of combining a risk-free asset with a portfolio of risky assets. 6:49 LOS : Explain the capital allocation line (CAL) and the capital market line (CML). 12:08 LOS : Explain systematic and nonsystematic risk, including why an investor should not expect to receive additional return for bearing nonsystematic risk. 16:00 LOS : Explain return generating models (including the market model) and their uses. 24:32 LOS : Calculate and interpret beta. 29:31 LOS : Explain the capital asset pricing model (CAPM), including its assumptions, and the security market line (SML). 39:43 LOS : Calculate and interpret the expected return of an asset using the CAPM. 41:04 LOS : Describe and demonstrate applications of the CAPM and the SML. 48:18 LOS : Calculate and interpret the Sharpe ratio, Treynor ratio, M2, and Jensen’s alpha. #CFA #CFALevel1 #PortfolioManagement #RiskAndReturn #CAPM #SML #CML #SharpeRatio #TreynorRatio #JensensAlpha #Beta #SystematicRisk #InvestmentAnalysis #AnalystPrep

Comments