Finance Theory — 16.2: Understanding Beta скачать в хорошем качестве

Finance Theory — 16.2: Understanding Beta

20 часов назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Finance Theory — 16.2: Understanding Beta в качестве 4k

У нас вы можете посмотреть бесплатно Finance Theory — 16.2: Understanding Beta или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Finance Theory — 16.2: Understanding Beta в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Finance Theory — 16.2: Understanding Beta

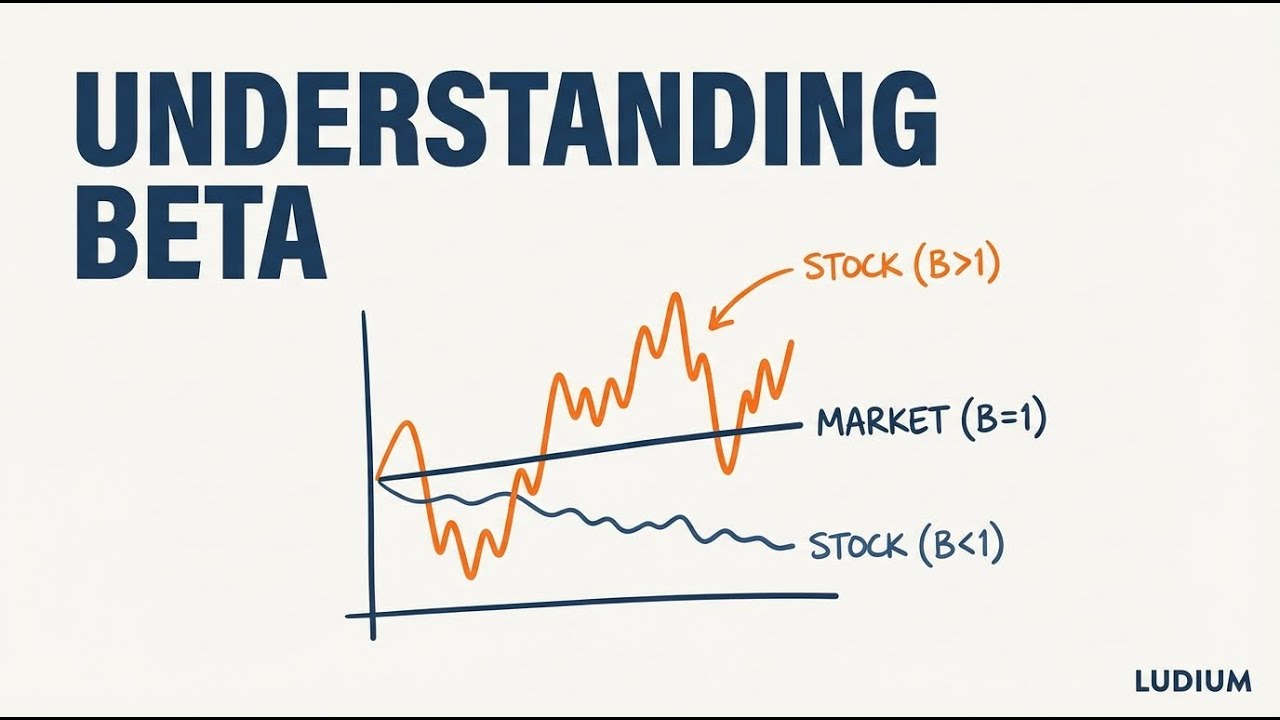

Why would a sophisticated investor accept returns below a savings account? The answer lies in beta — the single number that captures how an asset co-moves with the market. This video builds beta from first principles, showing why covariance dominates portfolio risk, how the Security Market Line prices systematic risk, and what special cases like zero-beta and negative-beta assets reveal about the true nature of risk. Key concepts covered: • Why covariance terms overwhelm variance terms as portfolios grow (n² − n vs n) • Beta formula: Cov(Rᵢ, Rₘ) / Var(Rₘ) and what each component means • The Security Market Line (SML) vs the Capital Market Line (CML) • Beta = 1: earning the market return with market-level systematic risk • Beta = 0: earning only the risk-free rate despite potentially high volatility • Negative beta: assets that earn below the risk-free rate as portfolio insurance • Gold and gold miners as real-world examples of low and near-negative beta • The 2007–2009 subprime crisis: how correlation convergence destroyed diversification • The core lesson: risk is co-movement, not volatility in isolation ━━━━━━━━━━━━━━━━━━━━━━━━ SOURCE MATERIALS The source materials for this video are from • Ses 16: The CAPM and APT II

Comments