Section-10 of Income Tax Act, 1961 Vs. Section-11 of the Income Tax Act, 2025 with Schedules скачать в хорошем качестве

Section-10 of Income Tax Act, 1961 Vs. Section-11 of the Income Tax Act, 2025 with Schedules

1 день назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Section-10 of Income Tax Act, 1961 Vs. Section-11 of the Income Tax Act, 2025 with Schedules в качестве 4k

У нас вы можете посмотреть бесплатно Section-10 of Income Tax Act, 1961 Vs. Section-11 of the Income Tax Act, 2025 with Schedules или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Section-10 of Income Tax Act, 1961 Vs. Section-11 of the Income Tax Act, 2025 with Schedules в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Section-10 of Income Tax Act, 1961 Vs. Section-11 of the Income Tax Act, 2025 with Schedules

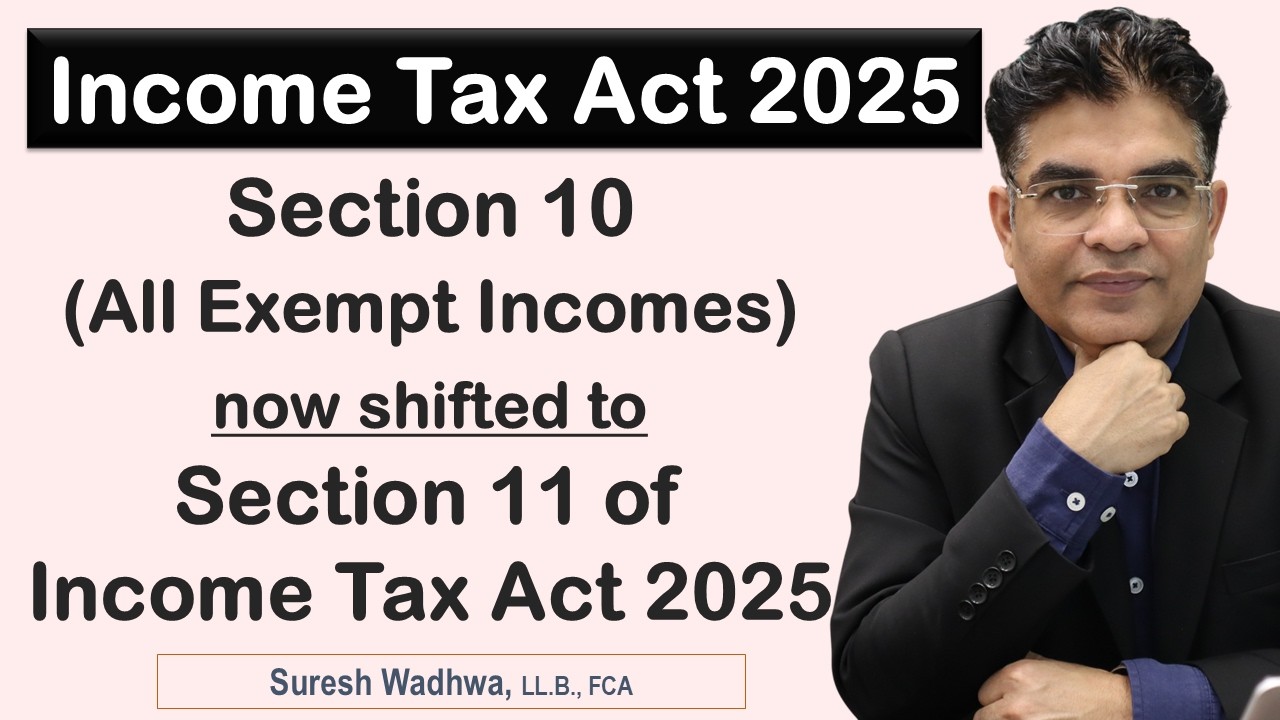

Section-10 of Income Tax Act, 1961 will now be Section-11 of the Income Tax Act, 2025 with Schedules This video is intended for educational and academic purposes, particularly for Chartered Accountants, Advocates, tax consultants, and students studying Direct Tax Law who wish to understand the structural transition from the Income Tax Act, 1961 to the proposed Income Tax Act, 2025. One of the most notable changes under the Income Tax Act, 2025 is the re-structuring and relocation of exemptions presently contained under Section 10 of the Income Tax Act, 1961. Under the existing Income Tax Act, 1961, Section 10 contains a large number of provisions granting exemption to various categories of income. These include exemptions relating to agricultural income, share of profit from partnership firms, allowances and perquisites, scholarships, certain incomes of charitable or statutory bodies, and various other specified receipts. Over the decades, this section has expanded considerably and now consists of a long list of sub-sections, provisos, explanations, and conditions, making it relatively complex and scattered in its structure. In the Income Tax Act, 2025, the legislature has attempted to simplify and reorganise the law by restructuring these exemptions in a more systematic and reader-friendly manner. As part of this exercise, the exemptions presently covered under Section 10 of the Income Tax Act, 1961 are proposed to be re-wired and repositioned under Section 11 of the Income Tax Act, 2025. However, instead of reproducing the entire list of exemptions within the main provision itself, the new Act introduces a Schedule-based framework. Accordingly, Section 11 of the Income Tax Act, 2025 operates as the enabling provision which provides that specified incomes shall not be included in the computation of total income, subject to the conditions and entries prescribed in Schedule II to Schedule VII of the Act. The purpose of introducing Schedules II to VII is to organise different categories of exempt income in a structured and modular format. Each Schedule is expected to deal with specific types of exemptions, thereby improving the overall clarity and usability of the legislation. This approach reduces congestion in the main section and allows the law to be presented in a more logical and simplified manner. Therefore, while the substantive concept of exempt income largely continues, the legislative architecture has been redesigned. What was earlier scattered within multiple clauses of Section 10 of the Income Tax Act, 1961 will now be systematically distributed across the Schedules of the Income Tax Act, 2025, with Section 11 serving as the central reference provision for exempt incomes. This structural shift is part of the broader objective of the proposed Income Tax Act, 2025, which aims to make the tax law shorter, simpler, and easier to interpret, while retaining most of the existing policy framework. In this video, we discuss: • How Section 10 of the Income Tax Act, 1961 has been reorganised in the new law • Why the legislature has introduced a Schedule-based exemption framework • The role of Section 11 of the Income Tax Act, 2025 • The significance of Schedules II to VII in classifying exempt income • What this change means for tax professionals, CA students, and taxpayers #IncomeTaxAct2025 #Section10IncomeTax #Section11IncomeTax #DirectTaxLaw #CAStudents #TaxLawIndia #incometaxupdates

Comments