Your Income is Dropping? Here's What Lenders Do Next скачать в хорошем качестве

Your Income is Dropping? Here's What Lenders Do Next

5 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Your Income is Dropping? Here's What Lenders Do Next в качестве 4k

У нас вы можете посмотреть бесплатно Your Income is Dropping? Here's What Lenders Do Next или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Your Income is Dropping? Here's What Lenders Do Next в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Your Income is Dropping? Here's What Lenders Do Next

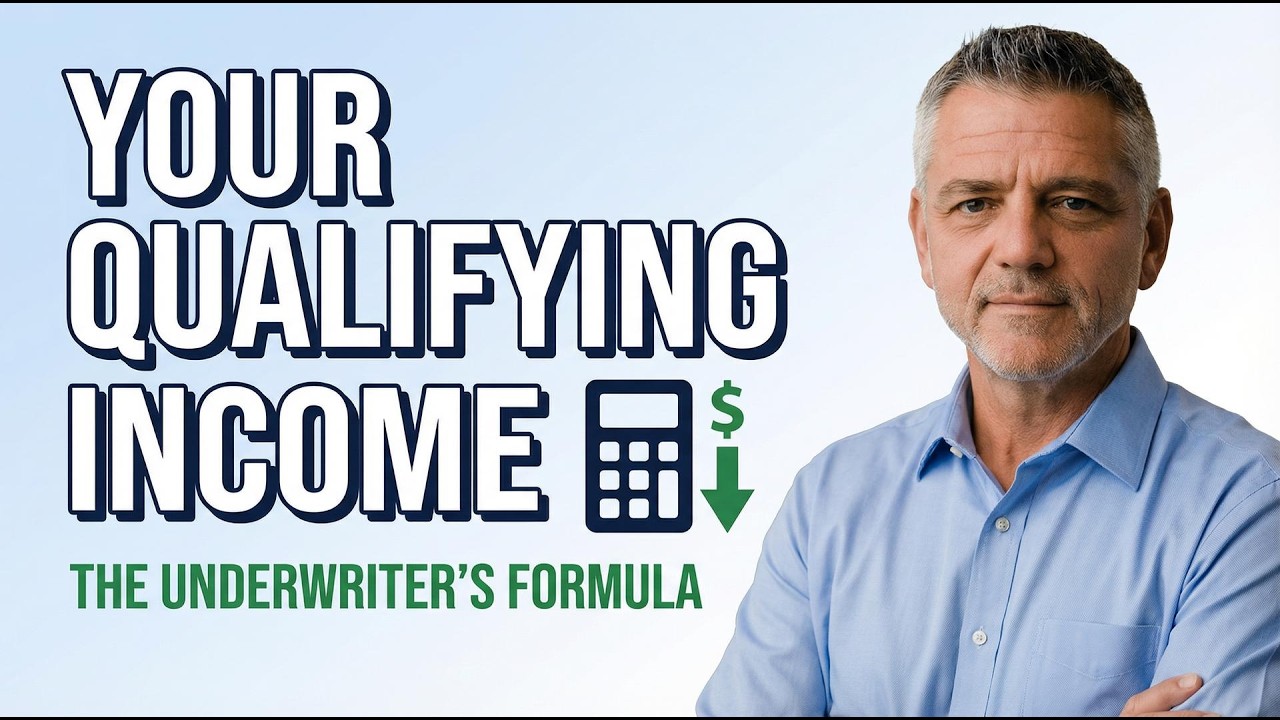

How do mortgage underwriters calculate qualifying income? If your paycheck doesn't match your mortgage approval amount, here's the underwriter's formula — step by step, dollar by dollar. You earn $120,000 a year… so why did the lender only qualify you on $85,000? 👉 Have a question about YOUR qualifying income? Ask confidentially here: https://www.seanbiggins.com/YouTube After 36 years in mortgage banking and thousands of closed loans, I've seen buyers lose homes simply because they didn't understand how income is analyzed. Whether you're a first-time home buyer, self-employed borrower, or trying to understand your debt-to-income ratio — this is the underwriter's playbook. We cover: • The Ability-to-Repay (ATR) Rule — What "verified, documented, stable, and likely to continue" really means under CFPB Regulation Z. • Lender Overlays — Why some lenders are stricter than Fannie Mae, Freddie Mac, FHA, or VA guidelines. • Base vs. Variable Income — Overtime, bonuses, commissions, 2-year averaging, and how declining income impacts approval. • Self-Employed Income — Why underwriters use tax returns (net profit, not gross revenue), depreciation add-backs, and documentation requirements. • Employment Gaps & W-2 to 1099 Changes — The 6-month rule and how switching to 1099/self-employment can reset your qualifying clock. • Grossing Up Non-Taxable Income — How Social Security, VA disability, and child support may be adjusted 15–25% to improve your debt-to-income ratio. Key Takeaways • Underwriters typically average 2 years of variable income • Self-employed qualifying income = net profit, not gross revenue • A 6+ month employment gap can require requalification • Non-taxable income (VA disability, Social Security) may be grossed up up to 25% Official Underwriting Guidelines Referenced: Fannie Mae Selling Guide https://selling-guide.fanniemae.com/ Freddie Mac Seller/Servicer Guide (Chapter 5300 Stable Monthly Income) https://guide.freddiemac.com/ FHA Handbook 4000.1 https://www.hud.gov/program_offices/h... VA Pamphlet 26-7, Chapter 4 – Credit Underwriting (KnowVA) https://www.knowva.ebenefits.va.gov/s... CFPB Ability-to-Repay Rule (Regulation Z §1026.43) https://www.consumerfinance.gov/rules... I'm Sean Biggins — 36-year mortgage veteran and Realtor®. No hype. Just underwriting mechanics explained clearly. Need a trusted agent referral anywhere in the U.S.? Request here: https://www.seanbiggins.com/contact.php (Referral fees may apply; no additional cost to you.) Confidential question? https://www.seanbiggins.com/YouTube SC Realtor License #139940 #MortgageUnderwriting #QualifyingIncome #DebtToIncomeRatio #FirstTimeHomeBuyer #SelfEmployedMortgage Educational content only. Not legal, tax, or financial advice. Guidelines and regulations change. Always consult licensed professionals regarding your specific situation.

Comments

-

2 недели назад

2 недели назад

-

Трансляция закончилась 1 день назад

Трансляция закончилась 1 день назад

-

4 дня назад

4 дня назад

-

Трансляция закончилась 8 часов назад

Трансляция закончилась 8 часов назад

-

2 часа назад

2 часа назад

-

Трансляция закончилась 9 часов назад

Трансляция закончилась 9 часов назад

-

11 часов назад

11 часов назад

-

7 дней назад

7 дней назад

-

11 часов назад

11 часов назад

-

Трансляция закончилась 2 дня назад

Трансляция закончилась 2 дня назад

-

9 часов назад

9 часов назад

-

1 день назад

1 день назад

-

2 месяца назад

2 месяца назад

-

Трансляция закончилась 1 день назад

Трансляция закончилась 1 день назад

-

1 день назад

1 день назад

-

7 дней назад

7 дней назад

-

7 часов назад

7 часов назад

-

8 дней назад

8 дней назад

-

12 часов назад

12 часов назад

-

1 месяц назад

1 месяц назад