Standard Costs скачать в хорошем качестве

Standard Costs

5 лет назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Standard Costs в качестве 4k

У нас вы можете посмотреть бесплатно Standard Costs или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Standard Costs в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Standard Costs

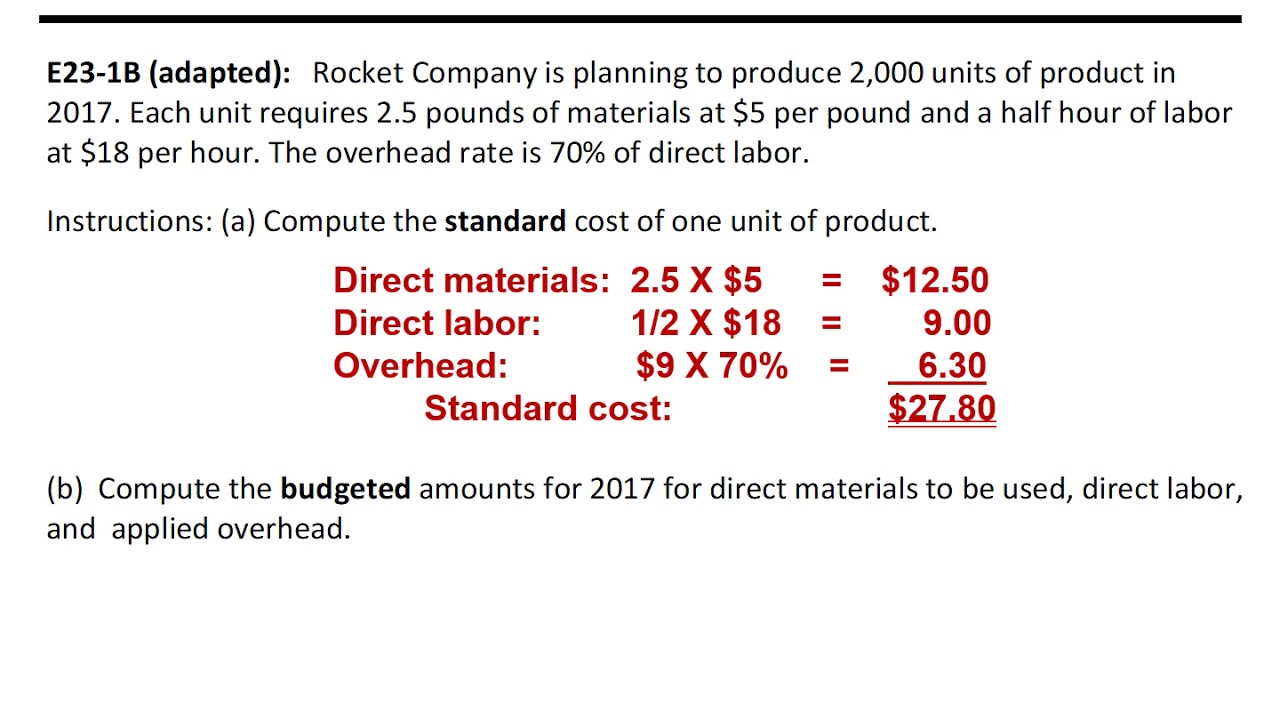

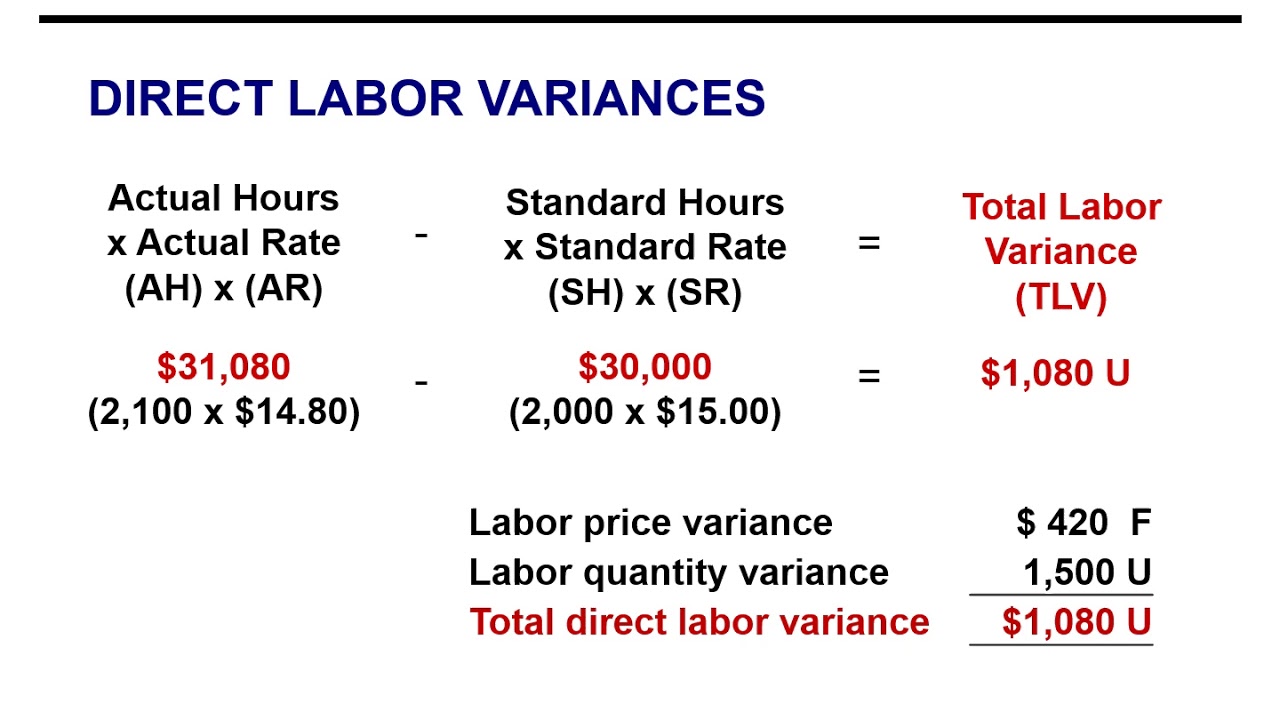

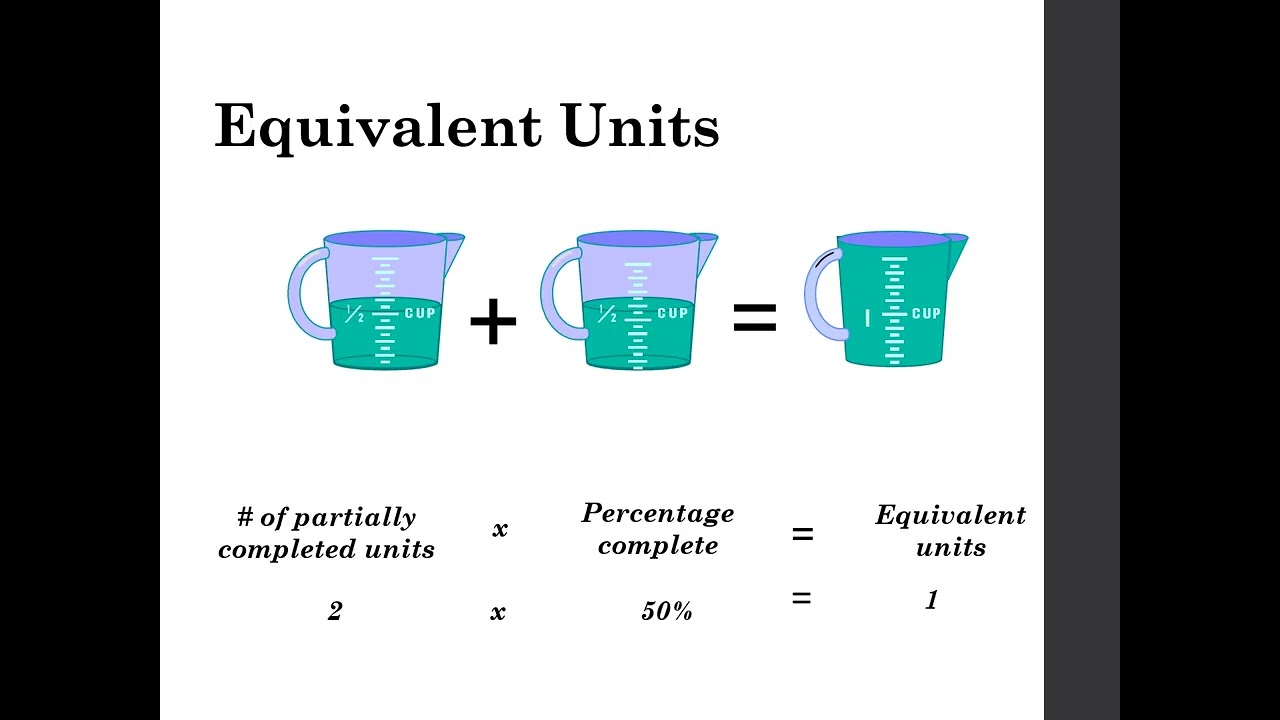

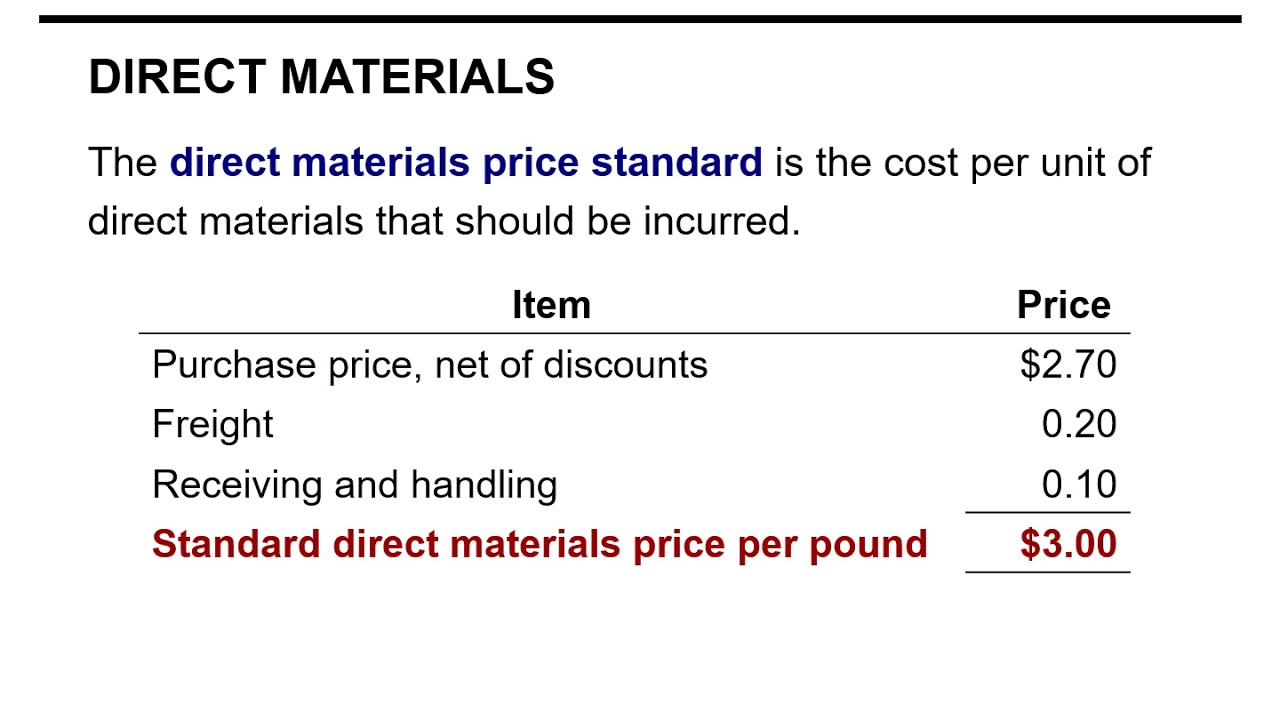

Both standards and budgets are predetermined costs. The primary difference is that a standard is a unit amount, whereas a budget is a total amount. A standard may be regarded as the budgeted cost per unit of product. The direct materials price standard should be based on the delivered cost of raw materials plus an allowance for receiving and handling. The direct materials quantity standard should establish the required quantity plus an allowance for waste and spoilage. The direct labor price standard should be based on current wage rates and anticipated adjustments such as COLAs. It also generally includes payroll taxes and fringe benefits. Direct labor quantity standards should be based on required production time plus an allowance for rest periods, cleanup, machine setup, and machine downtime. For manufacturing overhead, a standard predetermined overhead rate is used. It is based on an expected standard activity index such as standard direct labor hours or standard machine hours.

Comments