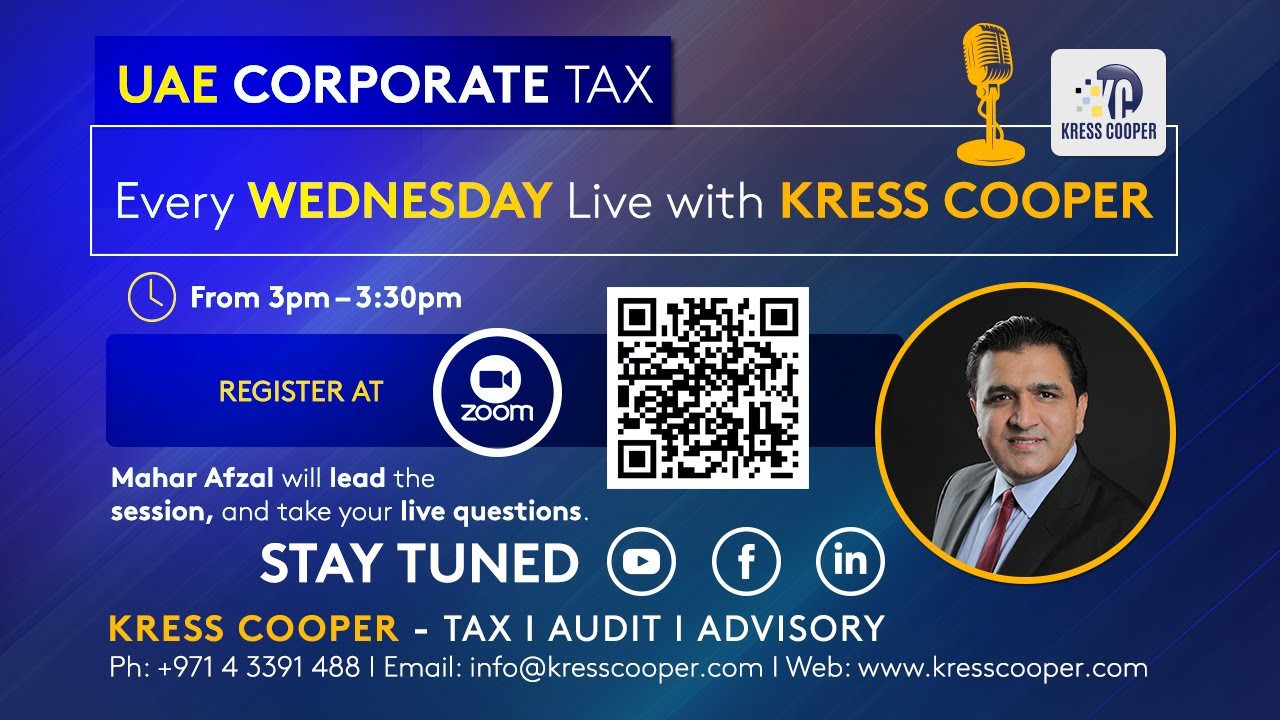

UAE CT: Application of Corporate Tax on Real Estate Sector скачать в хорошем качестве

UAE CT: Application of Corporate Tax on Real Estate Sector

Трансляция закончилась 2 года назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: UAE CT: Application of Corporate Tax on Real Estate Sector в качестве 4k

У нас вы можете посмотреть бесплатно UAE CT: Application of Corporate Tax on Real Estate Sector или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон UAE CT: Application of Corporate Tax on Real Estate Sector в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

UAE CT: Application of Corporate Tax on Real Estate Sector

The real estate industry involves different players such as developers, contractors, sub-contractors, and brokers, each with specific roles. The parties can be categorized as either resident or non-resident persons. Resident parties can further be classified as resident juridical persons or resident natural persons. Any developer, contractor, sub-contractor, or broker registered as a limited liability company, public joint stock company, etc. which has a separate legal personality from its owner is referred to as a juridical person. Any developer, contractor, sub-contractor, or broker registered as a limited liability company, public joint stock company, etc. which has a separate legal personality from its owner is referred to as a juridical person. If such a company is registered in a free zone, it is known as a free zone juridical person. A free zone person who meets the criteria of a qualifying free zone person is called a "Qualifying Free Zone Person (QFZP)." Resident juridical parties established in the UAE or outside the UAE but controlled and managed from within the UAE are subject to corporate tax (CT) on their worldwide taxable income. A person operating as a sole establishment, civil company, unincorporated partnership, or freelancer without a separate legal personality from their owners but conducting business in the UAE is considered a natural resident person. Such individuals are liable to pay CT on their worldwide income related to their UAE business only.

Comments

-

1 год назад

1 год назад

-

5 дней назад

5 дней назад

-

1 год назад

1 год назад

-

1 год назад

1 год назад

-

1 год назад

1 год назад

-

Трансляция закончилась 2 года назад

Трансляция закончилась 2 года назад

-

Трансляция закончилась 2 недели назад

Трансляция закончилась 2 недели назад

-

1 год назад

1 год назад

-

Трансляция закончилась 1 год назад

Трансляция закончилась 1 год назад

-

7 лет назад

7 лет назад

-

Трансляция закончилась 6 часов назад

Трансляция закончилась 6 часов назад

-

13 часов назад

13 часов назад

-

Трансляция закончилась 2 месяца назад

Трансляция закончилась 2 месяца назад

-

1 год назад

1 год назад

-

17 часов назад

17 часов назад

-

1 год назад

1 год назад

-

1 год назад

1 год назад

-

1 год назад

1 год назад

-

2 года назад

2 года назад

-

4 года назад

4 года назад