Скачать с ютуб Partnerships | Advantages and Disadvantages в хорошем качестве

Partnerships | Advantages and Disadvantages

4 года назад

Скачать бесплатно и смотреть ютуб-видео без блокировок Partnerships | Advantages and Disadvantages в качестве 4к (2к / 1080p)

У нас вы можете посмотреть бесплатно Partnerships | Advantages and Disadvantages или скачать в максимальном доступном качестве, которое было загружено на ютуб. Для скачивания выберите вариант из формы ниже:

Загрузить музыку / рингтон Partnerships | Advantages and Disadvantages в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Partnerships | Advantages and Disadvantages

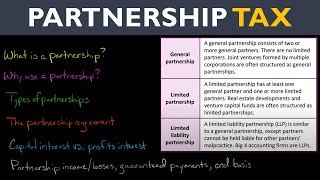

A partnership is easy to form, since you don't need to file articles of incorporation or create an LLC. However, partners don't enjoy limited legal liability (except for limited partners who are only liable for partnership debts to the extent of their investment, and limited liability partnerships where partners are only liable for their own actions). A partnership is a flow-through entity, which means there is only one layer of taxation (in contrast to a C corporation, which is subject to double taxation) and partners can deduct their share of the partnership's losses. However, guaranteed payments to partners and partners' profit allocations are both subject to self-employment tax. Moreover, guaranteed payments reduce the amount of the Qualified Business Income (QBI) deduction. A further disadvantage of partnerships is that you need the consent of every single partner to add a new partner; this can make it difficult to take on new investors. Partnerships have several advantages over other entity types. First, pretty much any entity can be a partner (in contrast to S corporations, which have restrictions on who can be a shareholder). Second, partnerships can make special allocations according to the partnership agreement. For example, you could have two 50/50 partners and yet allocate 100% of the depreciation deductions to one partner (for the IRS to respect a special allocation, it must have substantial economic effect). Third, you can often distribute property from a partnership without taking a tax hit (when a corporation distributes appreciated property there is a taxable gain). Fourth, you can increase a partner's basis by adding debt to the partnership. Thus, if the partner's basis is at zero, the partnership can take on debt to increase the partner's basis (this would allow the partner to deduct additional losses of the partnership, should they occur). Fifth, you can contribute property to a partnership without incurring tax per Section 721 (this is also true for corporations per section 351, but with corporations you have the 80% control requirement).— Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world. — SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS: • A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING • A 44-PAGE GUIDE TO U.S. TAXATION • A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS • MANY MORE FREE PDF GUIDES AND SPREADSHEETS http://eepurl.com/dIaa5z — SUPPORT EDSPIRA ON PATREON * / prof_mclaughlin — GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT https://edspira.thinkific.com — LISTEN TO THE SCHEME PODCAST Apple Podcasts: https://podcasts.apple.com/us/podcast... Spotify: https://open.spotify.com/show/4WaNTqV... Website: https://www.edspira.com/podcast-2/ — GET TAX TIPS ON TIKTOK / prof_mclaughlin — ACCESS INDEX OF VIDEOS https://www.edspira.com/index — CONNECT WITH EDSPIRA Facebook: / edspira Instagram: / edspiradotcom LinkedIn: / edspira — CONNECT WITH MICHAEL Twitter: / prof_mclaughlin LinkedIn: / prof-michael-mclaughlin — ABOUT EDSPIRA AND ITS CREATOR https://www.edspira.com/about/ https://michaelmclaughlin.com

Comments