Popular Retirement Advice That Can Backfire (If You Have $1.5M+) скачать в хорошем качестве

Popular Retirement Advice That Can Backfire (If You Have $1.5M+)

4 месяца назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Popular Retirement Advice That Can Backfire (If You Have $1.5M+) в качестве 4k

У нас вы можете посмотреть бесплатно Popular Retirement Advice That Can Backfire (If You Have $1.5M+) или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Popular Retirement Advice That Can Backfire (If You Have $1.5M+) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Popular Retirement Advice That Can Backfire (If You Have $1.5M+)

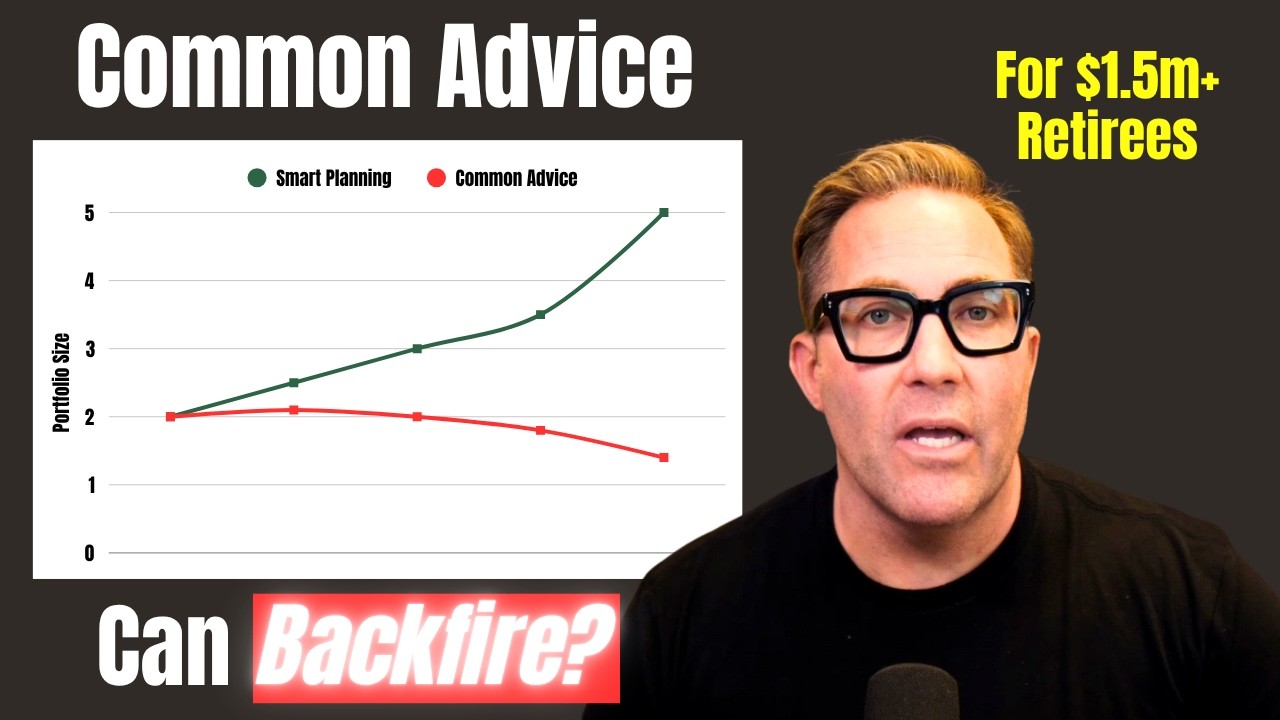

Get an idea of where you stand financially: https://app.rightcapital.com/account/... A stress-free retirement is a good one, and we want to help you get there. Ready for a retirement checkup? Book a free call → https://www.shopefinancial.com/meet Get exclusive retirement insights: https://lp.constantcontactpages.com/s... See how we work→ https://www.shopefinancial.com/ Subscribe to the channel → / @patrickshope —— While conventional retirement advice works for average investors, following popular strategies designed for people with modest savings can backfire spectacularly when you have substantial wealth. Understanding these high net worth retirement planning pitfalls could save you from expensive mistakes and help you optimize your wealth preservation strategy for your specific financial situation. Inside, you'll discover: • Roth Conversion IRMAA Mistakes - How careless $400,000+ Roth conversions trigger expensive Medicare IRMAA surcharges that can cost $5,000+ annually per person • Why strategic multi-year Roth conversion planning prevents Medicare premium penalties and optimizes long-term tax savings • Over-Insurance Trap for Wealthy Retirees - When self-insurance beats expensive premiums for high net worth individuals with substantial assets • Real examples showing how $2+ million portfolios can self-insure long-term care and life insurance more effectively than paying costly premiums • Beyond the 4% Rule for Affluent Retirees - Why rigid withdrawal strategies limit wealthy retirees and dynamic guardrails approaches maximize retirement income • How flexible withdrawal strategies allow $130,000 in good market years vs. $90,000 in rough patches instead of fixed 4% rule limitations • Asset Location Tax Optimization - The invisible mistake that drains wealthy portfolios through poor tax-inefficient asset placement strategies • Critical coordination between investment advisors and tax professionals to minimize avoidable taxes on substantial wealth —— 0:00 – Popular advice for average savers can backfire for wealthy retirees 0:22 – Four counterintuitive mistakes to avoid 1:28 – Mistake #1: “Roth converting your way into poverty” (IRMAA, MAGI spikes, multi-year plan) 3:00 – IRMAA mechanics & ranges 3:45 – Mistake #2: Over-insuring when you could self-insure (LTC, life insurance, risk sizing) 5:20 – Simple LTC self-insure math vs premiums 6:25 – Mistake #3: Rigid 4% rule for seven-figure portfolios vs flexible “guardrails” spending 7:40 – Mistake #4: Asset location tax drag (putting the wrong assets in the wrong accounts) 8:25 – Preserving wealth ≠ using the same playbook used to build it —— Branch address: 180 Little Lake Dr 2b, Ann Arbor, MI 48103 Branch phone number: (734) 479-1400 Investment advisory services offered though Sigma Planning Corporation, a registered investment advisor. Shope & Associates, LLC is independent of Sigma Planning Corporation. This material was generated in part by Anthropic, a form of Artificial Intelligence, based on prompts and information provided by Patrick Shope. Past market performance is no guarantee of future investment performance or success. The projections or other information generated by the provided tool are hypothetical, based on limited inputs and assumptions, not guarantees of future results —— Sources: https://www.cms.gov/newsroom/fact-she... https://www.medicare.gov/publications... https://secure.ssa.gov/poms.nsf/lnx/0... https://investor.genworth.com/news-ev... https://acl.gov/ltc/basic-needs/how-m... https://www.irs.gov/newsroom/irs-rele... https://www.irs.gov/instructions/i706

Comments

-

1 месяц назад

1 месяц назад

-

5 месяцев назад

5 месяцев назад

-

12 дней назад

12 дней назад

-

5 дней назад

5 дней назад

-

5 дней назад

5 дней назад

-

5 месяцев назад

5 месяцев назад

-

3 года назад

3 года назад

-

6 месяцев назад

6 месяцев назад

-

1 месяц назад

1 месяц назад

-

3 месяца назад

3 месяца назад

-

10 дней назад

10 дней назад

-

19 часов назад

19 часов назад

-

2 недели назад

2 недели назад

-

6 месяцев назад

6 месяцев назад

-

1 день назад

1 день назад

-

2 дня назад

2 дня назад

-

8 часов назад

8 часов назад

-

7 дней назад

7 дней назад

-

Трансляция закончилась 2 года назад

Трансляция закончилась 2 года назад

-

13 дней назад

13 дней назад