TractIQ and MSM Discuss the 2026 Self-Storage Almanac Data and Industry Trends for the Upcoming Year скачать в хорошем качестве

TractIQ and MSM Discuss the 2026 Self-Storage Almanac Data and Industry Trends for the Upcoming Year

10 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: TractIQ and MSM Discuss the 2026 Self-Storage Almanac Data and Industry Trends for the Upcoming Year в качестве 4k

У нас вы можете посмотреть бесплатно TractIQ and MSM Discuss the 2026 Self-Storage Almanac Data and Industry Trends for the Upcoming Year или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон TractIQ and MSM Discuss the 2026 Self-Storage Almanac Data and Industry Trends for the Upcoming Year в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

TractIQ and MSM Discuss the 2026 Self-Storage Almanac Data and Industry Trends for the Upcoming Year

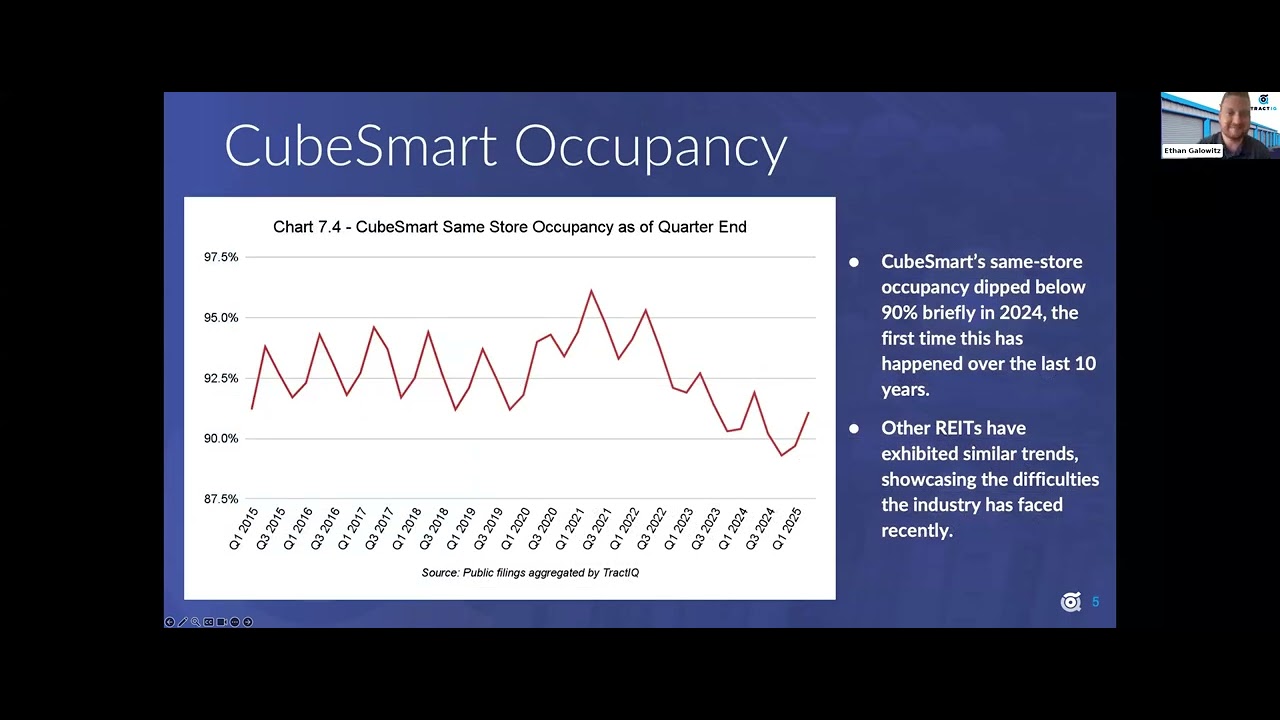

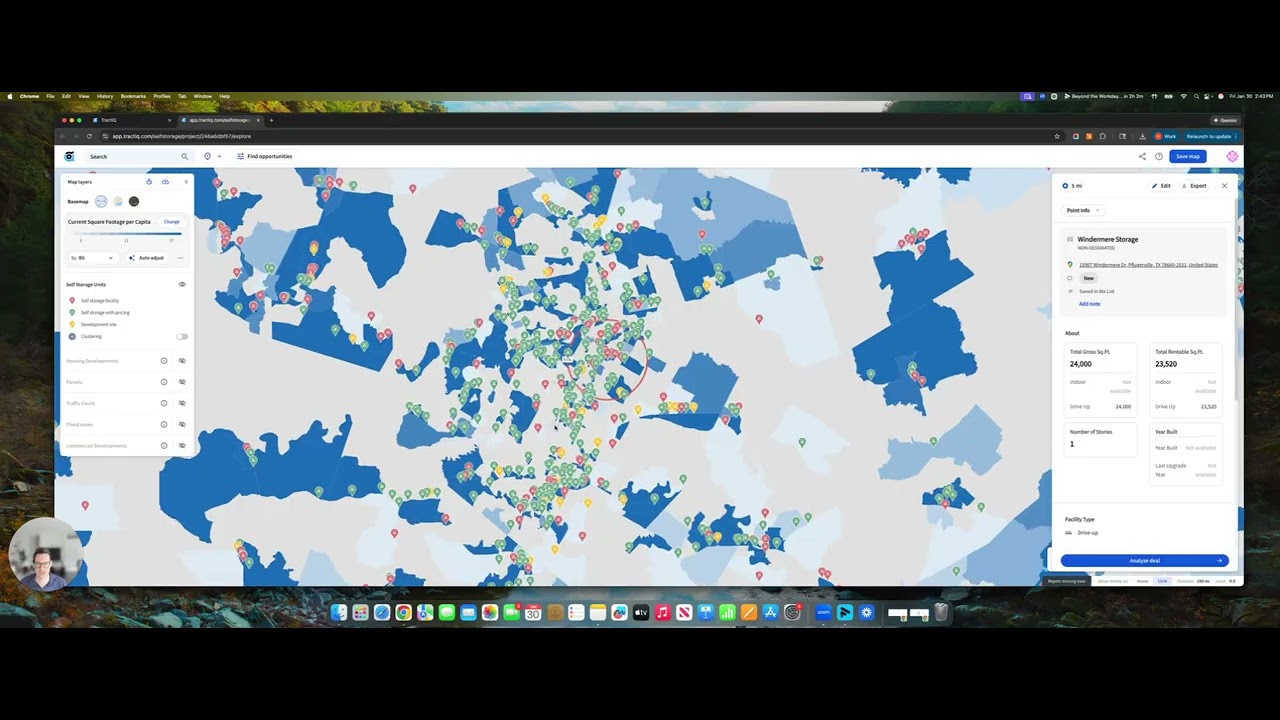

Public self-storage REITs continue to report strong same-store occupancy, with averages hovering in the low-to-mid 90% range through 2024 and into 2025. At a glance, that headline number suggests stability. But for investors, operators, and brokers trying to underwrite real deals, REIT averages only tell part of the story. This dataset highlights quarterly same-store occupancy across major self-storage REIT portfolios, weighted by rentable square footage. Recent quarters show occupancy generally ranging between approximately 93% and 95%, reinforcing the narrative that institutional portfolios remain resilient even as the market normalizes post-pandemic. However, REIT data reflects a highly curated subset of the market: stabilized, professionally managed, institutional-grade assets. These portfolios benefit from scale, brand recognition, and sophisticated revenue management. For most buyers evaluating individual facilities or regional portfolios, REIT averages are not representative of what’s actually happening on the ground. REIT reporting aggregates thousands of properties into a single metric. What it doesn’t show is how dramatically occupancy varies by market, asset type, or operator. It doesn’t reveal which facilities are quietly underperforming, where demand is softening, or how smaller operators are really faring. And it certainly doesn’t replace property-level underwriting. This is exactly why TractIQ built a new standard for self-storage intelligence. While REIT disclosures provide a useful macro benchmark, TractIQ goes deeper—sourcing verified occupancy directly from CMBS loan disclosures at the individual facility level. That means investors can finally see how specific properties are performing, not just how public portfolios report averages. Why does this matter? Because occupancy trends are a leading indicator of deal quality. And they allow buyers to underwrite based on reality—not assumptions, surveys, or rules of thumb. As the self-storage sector moves into a more normalized operating environment, underwriting discipline matters more than ever. Momentum-driven investing is giving way to data-driven decision-making. Sellers will increasingly need to support pricing with real operating performance. Buyers who rely solely on REIT averages or market estimates will be at a competitive disadvantage. This dataset offers a valuable starting point: a clear view into how institutional portfolios are performing today. But more importantly, it underscores the gap between high-level reporting and actionable underwriting data. If you’re serious about sourcing better deals, identifying risk earlier, and underwriting with confidence, REIT occupancy alone isn’t enough. Download the dataset to see how institutional occupancy trends compare—and discover why facility-level performance is quickly becoming the new standard in self-storage investing.

Comments

-

3 недели назад

3 недели назад

-

Трансляция закончилась 10 дней назад

Трансляция закончилась 10 дней назад

-

3 часа назад

3 часа назад

-

5 дней назад

5 дней назад

-

10 дней назад

10 дней назад

-

3 дня назад

3 дня назад

-

4 дня назад

4 дня назад

-

11 дней назад

11 дней назад

-

3 недели назад

3 недели назад

-

11 дней назад

11 дней назад

-

6 дней назад

6 дней назад

-

2 недели назад

2 недели назад

-

Трансляция закончилась 3 дня назад

Трансляция закончилась 3 дня назад

-

3 недели назад

3 недели назад

-

11 дней назад

11 дней назад

-

13 часов назад

13 часов назад

-

9 дней назад

9 дней назад

-

1 день назад

1 день назад

-

5 часов назад

5 часов назад

-

Трансляция закончилась 5 дней назад

Трансляция закончилась 5 дней назад