2/2| RANTAIAN |DIRECT METHOD | PREPARE STATEMENT OF CASH FLOWS - TUTORIAL | FAR210/FAR160 JAN2018-Q5 скачать в хорошем качестве

2/2| RANTAIAN |DIRECT METHOD | PREPARE STATEMENT OF CASH FLOWS - TUTORIAL | FAR210/FAR160 JAN2018-Q5

5 лет назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: 2/2| RANTAIAN |DIRECT METHOD | PREPARE STATEMENT OF CASH FLOWS - TUTORIAL | FAR210/FAR160 JAN2018-Q5 в качестве 4k

У нас вы можете посмотреть бесплатно 2/2| RANTAIAN |DIRECT METHOD | PREPARE STATEMENT OF CASH FLOWS - TUTORIAL | FAR210/FAR160 JAN2018-Q5 или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон 2/2| RANTAIAN |DIRECT METHOD | PREPARE STATEMENT OF CASH FLOWS - TUTORIAL | FAR210/FAR160 JAN2018-Q5 в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

2/2| RANTAIAN |DIRECT METHOD | PREPARE STATEMENT OF CASH FLOWS - TUTORIAL | FAR210/FAR160 JAN2018-Q5

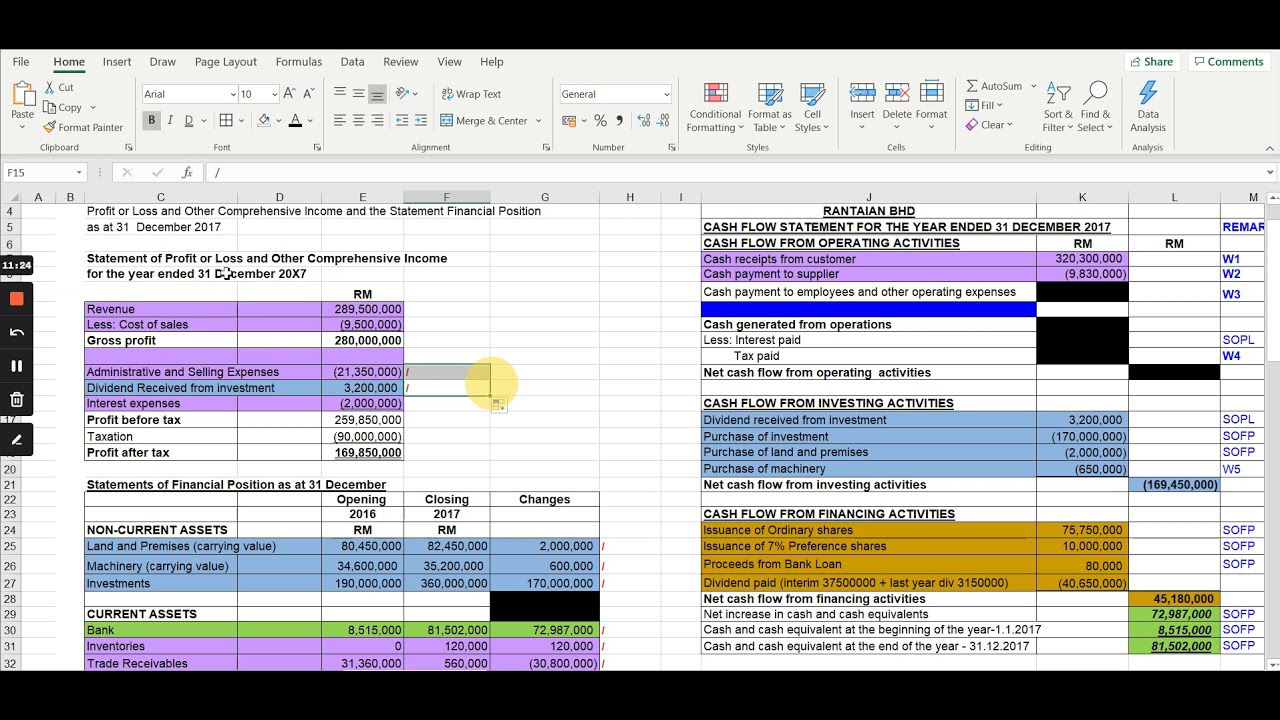

#IAS7#MFRS107 Dear lovely students, viewers and subscribers: Thank you for watching. I am so honoured to have you as my viewers and subscribers. If you have not subscribed please do to motivate me further as a I am not a full time YouTube content creator. Keep sharing my channel and links with others to spread it out and benefit more who are in need. TO STUDENTS: 1.Kindly download the question at https://drive.google.com/file/d/1AXaE... and print out before you start watching the discussion of answer. 2.Please attempt to complete this question relating to the preparation of statement of cash flow using the DIRECT METHOD on your own. 3. Compare your answer by watching the step by step discussion of the answers provided in the videos. This is a comprehensive TUTORIAL 2 of 2 videos showing step by step the PREPARATION of the Statement of Cash Flows under the DIRECT METHOD adopting the 6 STEPS COLOUR CODED APPROACH. Please click the link to watch the firstly watch the Part 1 of the discussion video -Tutorial 1/2 at • 1/2| RANTAIAN |DIRECT METHOD | PREPARE STA... The Statement of Cash Flows (SOCF) Template used here covers 4 Sections as follows: Section 1: Cash Flow From Operating Activities; Section 2: Cash Flow From Investing Activities; Section 3: Cash Flow From Financing Activities; and Section 4: Cash and Cash equivalents. IMPORTANT HIGHLIGHTS: Under IAS 7/MFRS 107, the computation of Cash Flow From Operating Activities under the Direct Method and Indirect Method are different. Nevertheless, the total amounts remain the same. However, the computations and presentation format are identical for both METHODS in relation to the all items and amounts of Cash Flow From Investing Activities and Cash Flows From Financing Activities.

Comments

-

5 лет назад

5 лет назад

-

2 дня назад

2 дня назад

-

5 лет назад

5 лет назад

-

4 года назад

4 года назад

-

8 дней назад

8 дней назад

-

Трансляция закончилась 2 часа назад

Трансляция закончилась 2 часа назад

-

2 часа назад

2 часа назад

-

2 дня назад

2 дня назад

-

4 часа назад

4 часа назад

-

1 день назад

1 день назад

-

2 часа назад

2 часа назад

-

Трансляция закончилась 1 день назад

Трансляция закончилась 1 день назад

-

Трансляция закончилась 1 день назад

Трансляция закончилась 1 день назад

-

Трансляция закончилась 2 дня назад

Трансляция закончилась 2 дня назад

-

1 год назад

1 год назад

-

Трансляция закончилась 2 дня назад

Трансляция закончилась 2 дня назад

-

Трансляция закончилась 9 дней назад

Трансляция закончилась 9 дней назад

-

1 месяц назад

1 месяц назад

-

8 дней назад

8 дней назад

-

7 часов назад

7 часов назад