Time Series Analysis: SARIMA Explained Simply - Forecasting Seasonal Peaks скачать в хорошем качестве

Time Series Analysis: SARIMA Explained Simply - Forecasting Seasonal Peaks

2 недели назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Time Series Analysis: SARIMA Explained Simply - Forecasting Seasonal Peaks в качестве 4k

У нас вы можете посмотреть бесплатно Time Series Analysis: SARIMA Explained Simply - Forecasting Seasonal Peaks или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Time Series Analysis: SARIMA Explained Simply - Forecasting Seasonal Peaks в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Time Series Analysis: SARIMA Explained Simply - Forecasting Seasonal Peaks

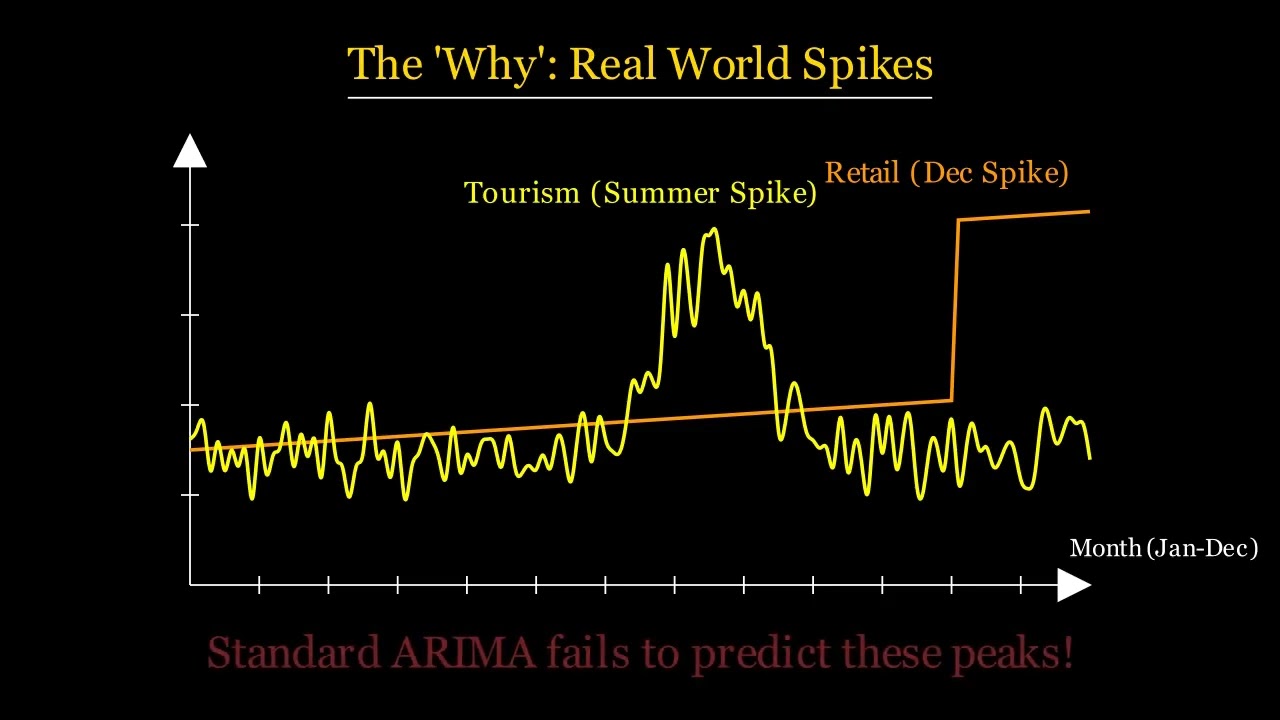

Welcome to an advanced masterclass on Time Series Analysis. Today, we delve into one of the most powerful forecasting tools in a data scientist's arsenal: the SARIMA model. We will specifically focus on how to capture and predict those massive recurring peaks we see in retail during Christmas and in tourism during the Summer. To understand SARIMA, we first look at the Anatomy of a Time Series. Any complex signal can be decomposed into four distinct components: Trend, Cycle, Residuals (White Noise), and our guest of honor: Seasonality. We analyze real-world examples: The Christmas Spike: Amazon's Q4 revenue surge. The Summer Spike: Airline ticket prices and electricity demand peaking in July/August. The Problem: Standard ARIMA models fail here because they treat these regular spikes as "anomalies." SARIMA treats them as predictable patterns. We break down the notation: SARIMA (p, d, q) x (P, D, Q)s. Lowercase (p, d, q): The non-seasonal part. Uppercase (P, D, Q): The seasonal part. The Period (s): The length of the cycle (e.g., s=12 for monthly data). We explain the mechanics of Seasonal Differencing (D=1)—subtracting last July's value from this July's value to stabilize the trend—and how to use ACF and PACF plots to spot spikes at seasonal intervals (lags 12, 24, 36). Finally, we discuss model selection using the AIC (Akaike Information Criterion) to find the perfect fit without over-fitting. 📚 Bibliography & Academic Entities: This lesson aligns with the advanced forecasting frameworks found in: "Time Series Analysis: Forecasting and Control" – Box & Jenkins "Forecasting: Principles and Practice" – Rob J. Hyndman "Basic Econometrics" – Damodar N. Gujarati

Comments