Drawing Power (DP) - How to Calculate Drawing Power for a Cash Credit Account | DP Limit Calculation скачать в хорошем качестве

Drawing Power (DP) - How to Calculate Drawing Power for a Cash Credit Account | DP Limit Calculation

2 года назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Drawing Power (DP) - How to Calculate Drawing Power for a Cash Credit Account | DP Limit Calculation в качестве 4k

У нас вы можете посмотреть бесплатно Drawing Power (DP) - How to Calculate Drawing Power for a Cash Credit Account | DP Limit Calculation или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Drawing Power (DP) - How to Calculate Drawing Power for a Cash Credit Account | DP Limit Calculation в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Drawing Power (DP) - How to Calculate Drawing Power for a Cash Credit Account | DP Limit Calculation

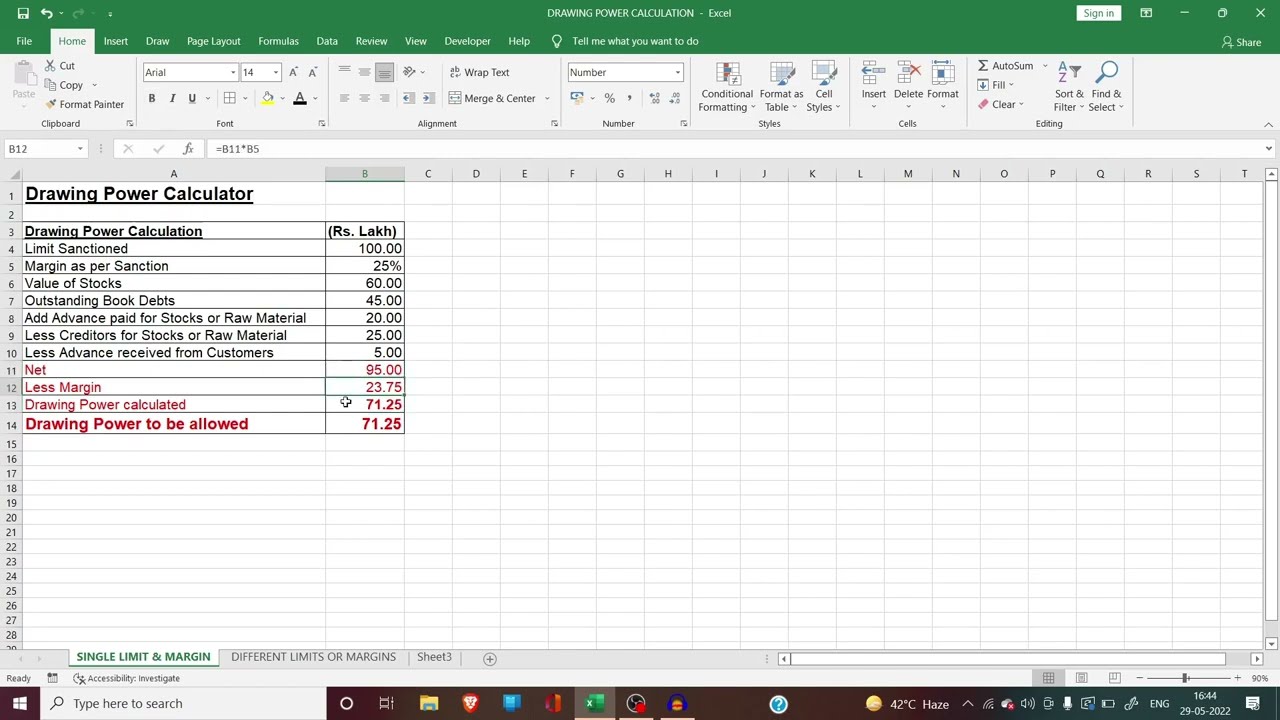

Drawing Power (DP) - How to Calculate Drawing Power for a Cash Credit Limit (CC) / Working Capital Limit account | DP Limit Calculation in Bank Branch Audit with examples discussed by CA. (IP) Vivek Khurana. Bank Branch Audit Update. How to Calculate Drawing Power for a Cash Credit / Working Capital Facility? With Examples. Cash Credit Limit (CC) / Working Capital Limit:- in Stock Audit / Concurrent Audit / Statutory Audit in Banks The Cash Credit limit (known as working capital limit) is sanctioned by banks and financial institutions to business organizations to run their day to day functions and achieve growth of business. This facility offers the borrowers flexibility and comfort to withdraw funds from the bank as per their financial requirement from time to time. The working capital facility is sanctioned for a period of one year and same may be renewed by the bank (or financial institution) every year with the same limit or enhanced limit or reduced limit to the borrower firm / company which is assessed on the basis of firm’s financial result of the preceding (reporting) year as well as on projected balance sheet for the ensuing (subsequent) year. Drawing Power generally addressed as “DP” is an important concept for Cash Credit (CC) facility availed from banks and financial institutions. It is the limit up to which a borrower can withdraw funds within the Cash Credit limit. Updating drawing power for working capital by the bank is an important credit monitoring exercise. The borrower is allowed utilize the funds from the cash credit account within the sanctioned cash credit limit or drawing power arrived by the bank for the particular month whichever is less. The Drawing Power is arrived on the basis the stock, book debts and creditors statement submitted by the borrower based on the closing position of the earlier month. Drawing Power can be calculated based on the specific margins and other terms and conditions contained in the Sanction letter. Here, margin is the owner’s contribution to the business. (In most of the cases, a margin on the stock is 25% and for book debts 40% of net debtors which may vary from bank to bank and industry to industry.) Banks have a practice of updating drawing power based on monthly / quarterly closing stock-book debt and trade creditors’ statements submitted by the firm/company. Drawing Power = Net Value of Stock + Net Value of Debtors. Where, Net Value of Stock = (Stock – Creditors)*(100% – % margin on stock) and Net Value of Debtors = (Debtors*(100% – % margin on debtors)) As Per RBI guidelines, Drawing Power is required to be arrived at based on the stock statement. Further, stock statements relied upon by the banks for determining drawing power should not be older than three months. Drawing Power can be calculated based on the specific margins and other terms and conditions contained in the Sanction letter. The final drawing power shall be lower of the sanctioned limit or the DP. “Stock” considered for calculating DP should be insured stock. Stock not covered under insurance, if considered for drawing power does not reflect the true drawing power since bank runs a huge risk, in the case of any mishappening. Usually, book debts of not more than 90 days old are considered for DP calculation. However, if the business has a longer credit cycle, more than 90 days debtors might be considered as per sanction terms. DISCLAIMER :- This Video is for the purposes of information / knowledge and shall not be treated as solicitation in any manner or of for any other purposes whatsoever. It shall not to be used for any legal advice /opinion and shall not to be used to rendering any professional opinion. Viewers are advised to kindly go through to original Government publications / notifications and published case laws or judicial pronouncements. The statements and opinions expressed in video are those of the speaker and do not necessarily reflect those of the CA Sansaar or any of its employees. CASansaar Team does not take any responsibility for the views of the Speaker. Our Social Links - Follow CA Sansaar YouTube / casansaarca Twitter / casansaar Facebook / casansaarca Linkedin / casansaar

Comments

-

Трансляция закончилась 1 год назад

Трансляция закончилась 1 год назад

-

8 лет назад

8 лет назад

-

Трансляция закончилась 9 часов назад

Трансляция закончилась 9 часов назад

-

1 год назад

1 год назад

-

4 года назад

4 года назад

-

1 год назад

1 год назад

-

1 месяц назад

1 месяц назад

-

1 месяц назад

1 месяц назад

-

![Самый богатый человек в Вавилоне. Джордж Самюэль Клейсон. [Аудиокнига]](https://imager.clipsaver.ru/XEEvmlkPZUw/max.jpg) 2 года назад

2 года назад

-

5 лет назад

5 лет назад

-

2 года назад

2 года назад

-

2 года назад

2 года назад

-

2 года назад

2 года назад

-

5 лет назад

5 лет назад

-

11 месяцев назад

11 месяцев назад

-

3 года назад

3 года назад

-

8 часов назад

8 часов назад

-

3 года назад

3 года назад

-

3 года назад

3 года назад

-

7 лет назад

7 лет назад