Absorption Costing Versus Marginal Costing - 4 Steps in Absorption Costing (AAT, ICB) скачать в хорошем качестве

Absorption Costing Versus Marginal Costing - 4 Steps in Absorption Costing (AAT, ICB)

3 года назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Absorption Costing Versus Marginal Costing - 4 Steps in Absorption Costing (AAT, ICB) в качестве 4k

У нас вы можете посмотреть бесплатно Absorption Costing Versus Marginal Costing - 4 Steps in Absorption Costing (AAT, ICB) или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Absorption Costing Versus Marginal Costing - 4 Steps in Absorption Costing (AAT, ICB) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Absorption Costing Versus Marginal Costing - 4 Steps in Absorption Costing (AAT, ICB)

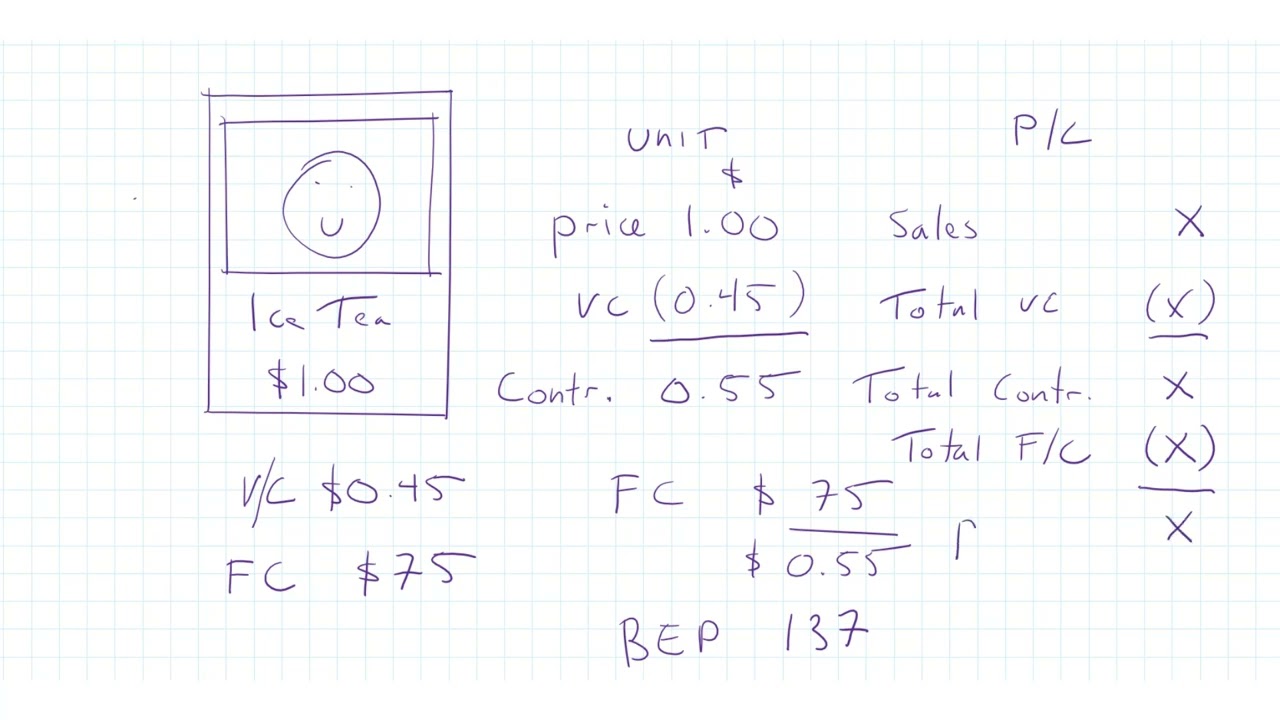

In this video I discuss the four stages of absorption when we look at absorbing overheads costs including allocation, apportionment and absorption. I also discuss rate per unit and the alternative rate of absorption as well as the differences between absorption and marginal costing to help with your understanding. Affiliate links - Equipment used: https://amzn.to/3A1KVnP - Camera https://amzn.to/3x32MZw - Camera stand https://amzn.to/35WzDUg - Foldable Desk This would be useful to anyone studying AAT Level 3 or Level 4 (AAT level 4) or even CIMA, ACCA or ACA. Overheads can be split into direct costs and indirect costs. Direct costs are directly attributable to a cost centre whereas indirect costs are more difficult to attribute and need to be apportioned across many different cost centres. Indirect costs can be variable, fixed or semi-variable (which include both fixed and variable elements). We also need to ensure that in the third step of apportionment, we re-charge service cost centre costs to the various other production cost centres.

Comments