How to Solve Accumulating and Discounting Questions in CM1? Simple Explanation (Force of Interest) скачать в хорошем качестве

How to Solve Accumulating and Discounting Questions in CM1? Simple Explanation (Force of Interest)

4 недели назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: How to Solve Accumulating and Discounting Questions in CM1? Simple Explanation (Force of Interest) в качестве 4k

У нас вы можете посмотреть бесплатно How to Solve Accumulating and Discounting Questions in CM1? Simple Explanation (Force of Interest) или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон How to Solve Accumulating and Discounting Questions in CM1? Simple Explanation (Force of Interest) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

How to Solve Accumulating and Discounting Questions in CM1? Simple Explanation (Force of Interest)

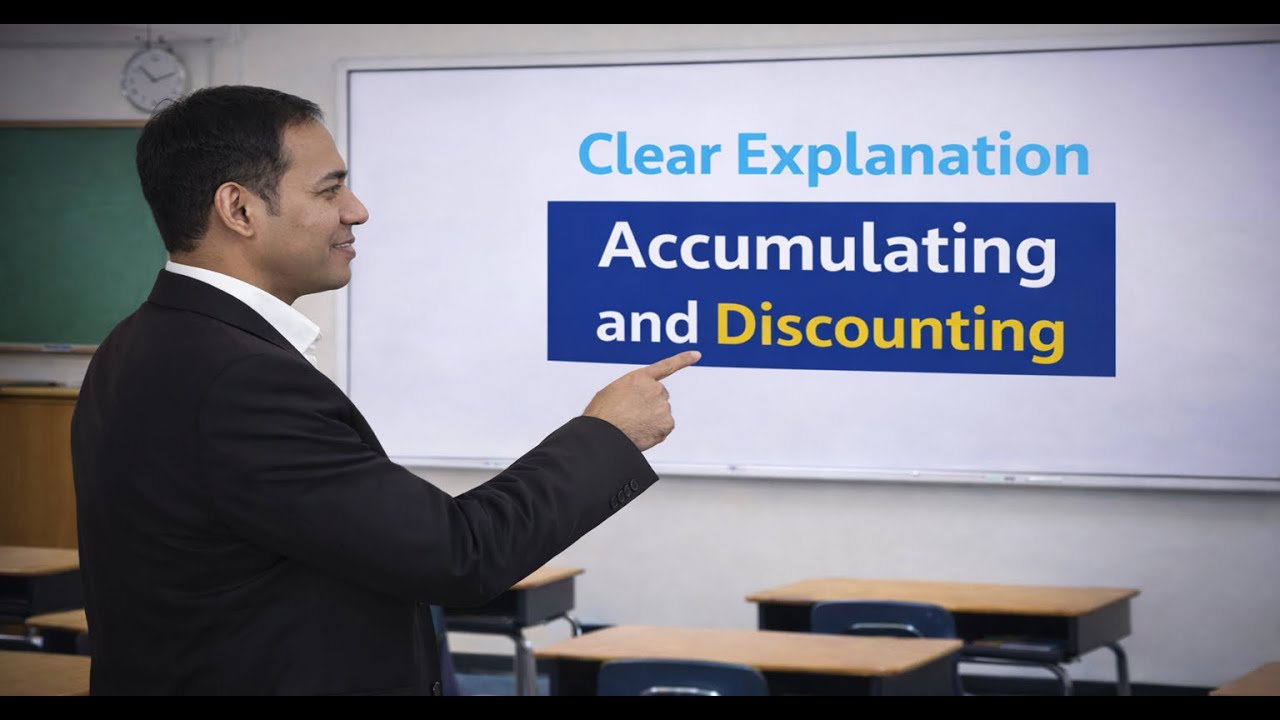

How to Solve Accumulating and Discounting Questions in CM1? Simple Explanation Linkedin / pratap-padhi Website https://smearseducation.com/ Join my FREE Skool Community to get all updates and support https://www.skool.com/sme-education-9... Watch my previous recordinds on CS2 Time Series 👉 • Master Time Series Forecasting:Guide to AR... CS2 Risk Modelling and Survival Analysis 👉 • What is a Stochastic Process? Easy explana... For my CM1 Previous recorded videos watch 👉 • How to calculate simple interest | Fundame... 👉 • CM1 Y Part2 Class1- A beginner's introduct... Timestamps 0:00 – Chapter overview. Accumulating vs discounting 1:10 – Constant interest and continuous compounding 2:05 – Meaning of force of interest δ 3:05 – Variable force δ(t) and integration idea 4:10 – Link between i, δ, v, and VT 5:20 – VT definition and reduction to Vⁿ 6:30 – Present value using VT 7:45 – Why V3 fails when time does not start at 0 9:10 – Accumulated value using 1 / VT 11:10 – Forward and backward movement rules 13:00 – Why V5 / V3 appears naturally 15:00 – Constant vs variable interest comparison 16:30 – Multi-cash-flow example logic 18:40 – Transition to continuous payments 20:00 – Meaning of rate of payment ρ(t) 22:30 – Present value of continuous payment streams 25:00 – Variable payment with constant interest 27:10 – Variable payment with variable interest 29:30 – Accumulated value of continuous payments 31:10 – Exam strategy and final guidance This video explains the Accumulating and Discounting chapter from CS1 using force of interest. You learn how to move money forward and backward in time when interest is constant and when interest changes continuously. The focus is on how students actually think during exams and how marks are lost due to symbol misuse. What you already know and how this chapter extends it You already know discounting using Vⁿ. You already know accumulation using (1 + i)ⁿ. You already know the link between i and δ. This chapter extends these ideas to situations where interest acts continuously and may vary with time. Key ideas built step by step • Accumulating vs discounting using interest rate i • Transition from i to force of interest δ • Continuous compounding using e^(δt) • Meaning of constant force vs time-dependent force δ(t) Force of interest intuition • Constant δ means steady growth at every instant • Variable δ(t) means growth rate changes with time • Accumulation becomes e^(∫δ(t)dt) • Discounting becomes e^(−∫δ(t)dt) VT notation. Core exam focus. • VT means present value of 1 due at time t • VT only works when time starts at 0 • VT replaces Vⁿ when δ(t) is given • VT reduces to Vⁿ when δ is constant Common student mistakes corrected • Writing V3 when time does not start at 0 • Treating V5 / V3 as V2 under variable δ(t) • Forgetting zero must be common to use VT • Using powers instead of integrals Accumulated value using VT • Present value uses VT • Accumulated value uses 1 / VT • Forward movement divides by VT • Backward movement multiplies by VT Key exam rule Interval length alone does not matter when δ(t) varies. The location of the interval matters. Worked structure for mixed time problems • Always connect through time 0 • Move backward using VT • Move forward using 1 / VT • Combine movements as ratios Example logic covered • Accumulated value of payments at different times • Present value of mixed cash flows • Correct handling of time gaps • Why V5 / V3 appears naturally Transition to Part 2 of the chapter Part 1 • Single payment • Time-varying interest • VT and accumulation logic Part 2 • Continuous payment streams • Introduction of rate of payment ρ(t) Continuous payment stream explained • Payments arrive continuously • Payment over small interval is ρ(t)dt • Each payment is discounted separately • Integration replaces summation Key formula for present value of continuous payments Present Value ∫ from a to b of ρ(t) × discount factor dt Key formula for accumulated value of continuous payments Accumulated Value ∫ from a to b of ρ(t) × accumulation factor dt Three exam-relevant cases explained Constant payment, constant interest Variable payment, constant interest variable interest What makes questions difficult • Two layers of integration • Splitting time intervals correctly • Choosing correct discount direction • Avoiding invalid symbols Exam strategy advice • Draw the timeline first • Mark time 0 clearly • Decide present or accumulated value • Write integral limits carefully • Substitute δ(t) only after limits are fixed #CM1#ActuarialScience#AccumulatingAndDiscounting #ForceOfInterest#ContinuousCompounding #VTNotation #FinancialMathematics #ActuarialExams#IFoA#IAI#InterestTheory

Comments

-

1 год назад

1 год назад

-

6 дней назад

6 дней назад

-

1 месяц назад

1 месяц назад

-

3 дня назад

3 дня назад

-

2 недели назад

2 недели назад

-

Трансляция закончилась 1 день назад

Трансляция закончилась 1 день назад

-

Трансляция закончилась 1 год назад

Трансляция закончилась 1 год назад

-

3 месяца назад

3 месяца назад

-

1 день назад

1 день назад

-

1 день назад

1 день назад

-

16 часов назад

16 часов назад

-

3 года назад

3 года назад

-

1 день назад

1 день назад

-

4 часа назад

4 часа назад

-

1 день назад

1 день назад

-

3 дня назад

3 дня назад

-

2 дня назад

2 дня назад

-

3 дня назад

3 дня назад

-

3 дня назад

3 дня назад

-

1 день назад

1 день назад