How Lenders Actually Calculate Income (Most Borrowers Get This Wrong) скачать в хорошем качестве

How Lenders Actually Calculate Income (Most Borrowers Get This Wrong)

5 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: How Lenders Actually Calculate Income (Most Borrowers Get This Wrong) в качестве 4k

У нас вы можете посмотреть бесплатно How Lenders Actually Calculate Income (Most Borrowers Get This Wrong) или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон How Lenders Actually Calculate Income (Most Borrowers Get This Wrong) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

How Lenders Actually Calculate Income (Most Borrowers Get This Wrong)

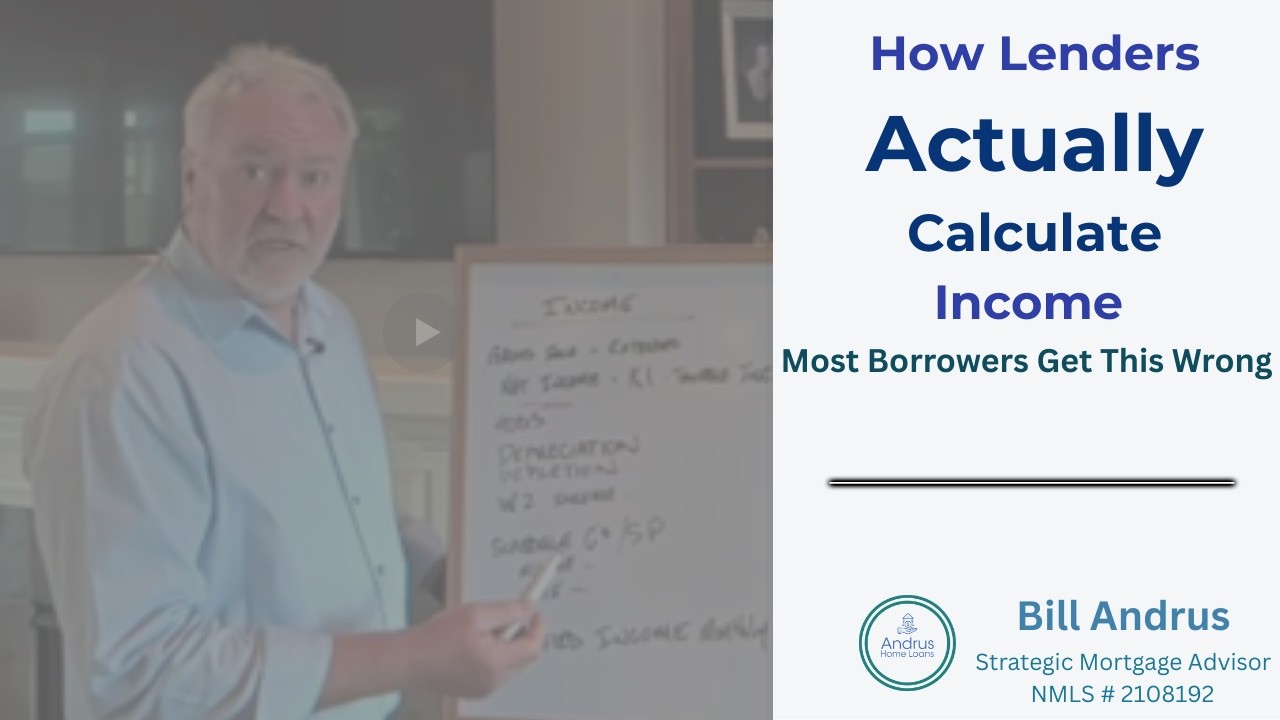

If you're self-employed and using your gross income to estimate what you qualify for, you're probably looking at the wrong number. In this video, I break down how lenders actually calculate qualifying income — and why the number that matters most is often very different from what borrowers expect. We cover: • How 1120 and K-1 income is evaluated • What gets added back (depreciation, depletion, etc.) • How Schedule C income is analyzed • The difference between taxable income and qualifying income • Why understanding structure changes your approval outcome My goal is clarity first. When you understand how income is calculated, you make confident decisions. And confident decisions are how you win. If this was helpful, subscribe for weekly mortgage strategy insights focused on income structuring, DTI strategy, rate positioning, and long-term approval planning. Serving Oregon, Washington, and California. Bill Andrus Strategic Mortgage Advisor NMLS #2108192 Licensed in OR, WA, CA Fairway Independent Mortgage Corporation NMLS #2289 Equal Housing Opportunity

Comments

![Trump i Netanjahu uderzają. Rosja i Chiny bezsilne [Analiza]](https://imager.clipsaver.ru/NJ0t3ykIjLU/max.jpg)