You May Need 50% Less to Retire Than You Think (Here’s the Math) скачать в хорошем качестве

You May Need 50% Less to Retire Than You Think (Here’s the Math)

3 часа назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: You May Need 50% Less to Retire Than You Think (Here’s the Math) в качестве 4k

У нас вы можете посмотреть бесплатно You May Need 50% Less to Retire Than You Think (Here’s the Math) или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон You May Need 50% Less to Retire Than You Think (Here’s the Math) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

You May Need 50% Less to Retire Than You Think (Here’s the Math)

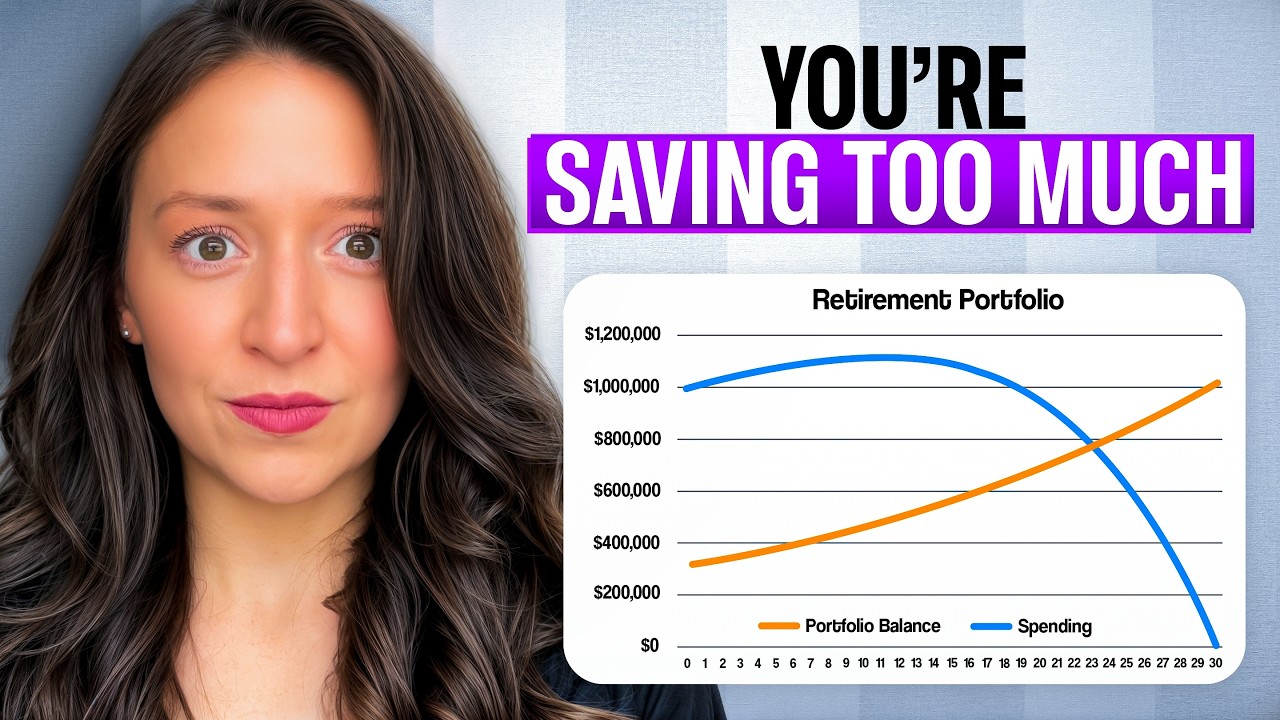

Most retirement advice is built around a single rigid rule: the 4% rule. While this rule is often presented as the gold standard for retirement planning, it can dramatically overstate how much money you actually need to retire, especially if you plan to retire early or have future income like Social Security. In this video, Erin breaks down why many people are unknowingly over-saving for retirement and how flexible withdrawal strategies, time-segmented retirement planning, and real-world spending behavior can fundamentally change the math. Using a detailed, research-backed example, this video shows how a couple targeting $90,000 per year in retirement income could retire with 50–60% less than the traditional retirement number they’ve been told, or alternatively, how the same portfolio could unlock retirement five to ten years earlier than expected. By separating retirement into phases, accounting for Social Security as an income floor, and allowing for variable spending instead of fixed inflation-adjusted withdrawals, the required portfolio size drops dramatically without increasing risk. This video explains why retirement planning based solely on the 4% rule often ignores human behavior, changing spending patterns, and the reality that retirees naturally adjust their expenses over time. You’ll learn how bridge-to-Social-Security strategies work, how guardrails and dynamic spending rules are supported by retirement research, and why withdrawal rates only matter during the lifetime income phase, not during finite pre-retirement or early retirement periods. If you’re wondering how much you really need to retire, whether you can retire earlier than you thought, or how flexible spending can reduce retirement risk while increasing freedom, this video walks through the math step by step. Whether you’re planning early retirement, optimizing a $1–$3 million portfolio, or questioning whether the standard retirement narrative applies to your life, this framework helps you build a retirement plan that reflects how people actually live, not just how spreadsheets assume they do. 00:00 Intro – Why Retirement Is Not About “Hitting the Number” 01:31 The One Shift That Lets You Retire Earlier With Less Money 02:26 The Traditional Retirement Model Everyone Is Taught 03:19 The Pre-Social Security Income Gap (Ages 60–67) 03:43 The Hidden Problem With the 4% Rule No One Explains 04:58 Why Flexible Spending Changes Retirement Math 05:35 Phase 1: Building a Retirement Bridge Before Social Security (60–67) 07:35 Phase 2: The Core Retirement Portfolio After Social Security (67+) 09:26 Rewinding the Math: Why You Don’t Need Your Full Portfolio at 60 11:02 What If You Actually Do Have $2.25 Million? 11:20 Conservative Assumptions That Stack the Odds Against Early Retirement 13:01 How Just 3% Real Returns Change Everything 13:47 The Retirement Aha Moment Most People Never See 16:52 Bloopers Some of my favorite books: https://amzn.to/3KF3tlr Camera & equipment I use: https://amzn.to/3Z20lof Disclaimer: Please note that this video is made for entertainment purposes only and not to be taken as financial advice. Always make sure to do your own research. Join the family & subscribe to my channel here: / erintalksmoney Thanks for watching, I appreciate you!

Comments