Florida Industry Update (02/16/2026) скачать в хорошем качестве

Florida Industry Update (02/16/2026)

11 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Florida Industry Update (02/16/2026) в качестве 4k

У нас вы можете посмотреть бесплатно Florida Industry Update (02/16/2026) или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Florida Industry Update (02/16/2026) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Florida Industry Update (02/16/2026)

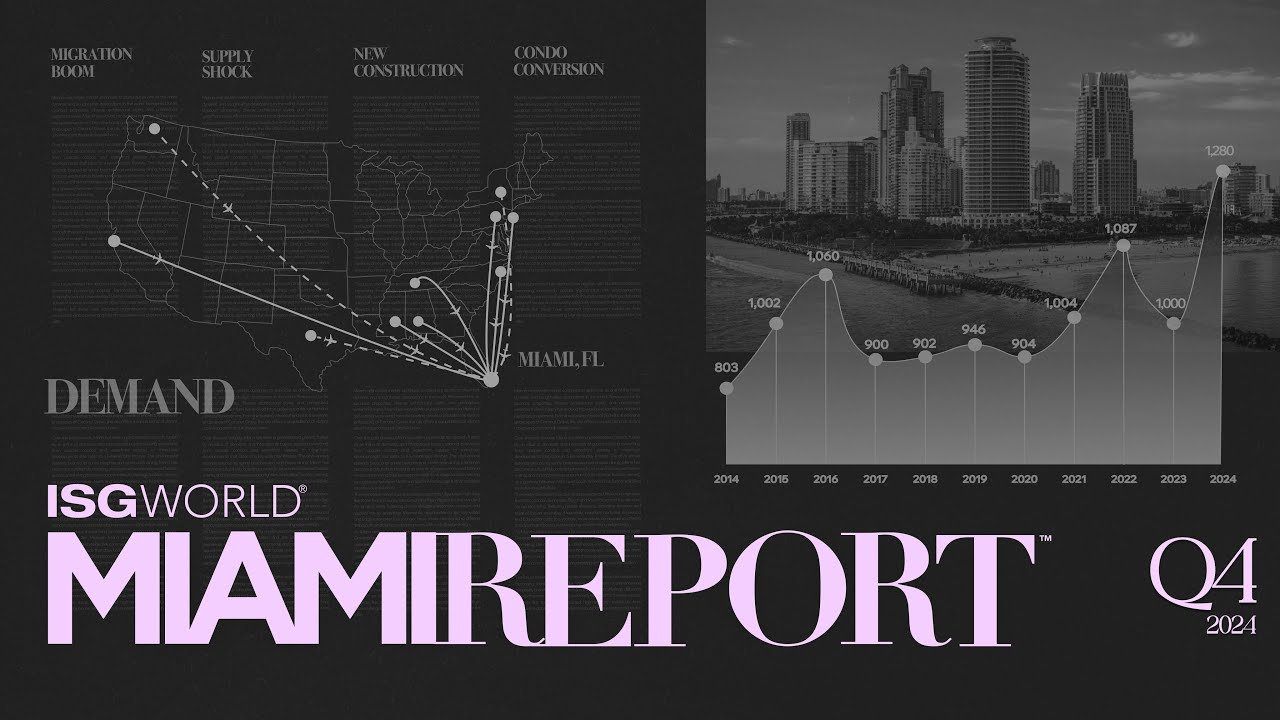

Rates Snapshot (from today’s image) 30 Yr Fixed: 6.04% | 15 Yr Fixed: 5.61% FHA 30 Yr: 5.62% | Jumbo 30 Yr: 6.27% 7/6 SOFR: 5.37% | VA 30 Yr: 5.64% Freddie Mac (updated weekly): 30 Yr 6.09%, 15 Yr 5.44% What we’re covering 1) Affordability is improving nationally Buyers now need 4% less income than a year ago to afford the typical home. In 37 of the 50 largest metros, affordability is improving. Implication: Lower rates are reopening conversations — especially with sidelined buyers. 2) Demand is rebounding as rates hover near 6% Weekly pending sales: 59,469 (2026) vs 60,316 (2025). Price cuts are down to 32.13% vs 33% last year. Implication: Buyers are stepping back in — and sellers have slightly more leverage than late 2025. 3) Investors hold 30% of purchases Small and mid-size investors are driving activity. Investor share remains elevated due to affordability pressure. Implication: Expect continued competition in entry-level and rental-friendly segments. 4) South Florida still dominates “hottest markets” list Top local ZIPs include: 33181 (Miami) 33480 (Palm Beach) 33127 (Miami) 33405 (West Palm Beach) 33133 (Miami) 33037 (Key Largo) 33444 (Delray Beach) Implication: Luxury and coastal demand remains strong. What agents can do this week: Re-engage 2024–2025 buyers who paused due to rates. Target landlords and small investors — capital is still active. Double down on pricing strategy — price cuts are easing. Market ZIP-level momentum in Miami, Palm Beach, and Delray. Lead with payment clarity, not just list price.

Comments

-

1 месяц назад

1 месяц назад

-

5 месяцев назад

5 месяцев назад

-

-

8 часов назад

8 часов назад

-

Трансляция закончилась 7 месяцев назад

Трансляция закончилась 7 месяцев назад

-

8 дней назад

8 дней назад

-

1 день назад

1 день назад

-

1 день назад

1 день назад

-

1 месяц назад

1 месяц назад

-

3 месяца назад

3 месяца назад

-

1 год назад

1 год назад

-

4 месяца назад

4 месяца назад

-

Трансляция закончилась 1 год назад

Трансляция закончилась 1 год назад

-

3 часа назад

3 часа назад

-

1 месяц назад

1 месяц назад

-

2 года назад

2 года назад

-

12 дней назад

12 дней назад

-

1 день назад

1 день назад

-

11 дней назад

11 дней назад

-

4 часа назад

4 часа назад