Effective and Key Rate Duration - Measuring Non Parallel Yield Curve Shifts (CFA Level 1) скачать в хорошем качестве

Effective and Key Rate Duration - Measuring Non Parallel Yield Curve Shifts (CFA Level 1)

3 месяца назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Effective and Key Rate Duration - Measuring Non Parallel Yield Curve Shifts (CFA Level 1) в качестве 4k

У нас вы можете посмотреть бесплатно Effective and Key Rate Duration - Measuring Non Parallel Yield Curve Shifts (CFA Level 1) или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Effective and Key Rate Duration - Measuring Non Parallel Yield Curve Shifts (CFA Level 1) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Effective and Key Rate Duration - Measuring Non Parallel Yield Curve Shifts (CFA Level 1)

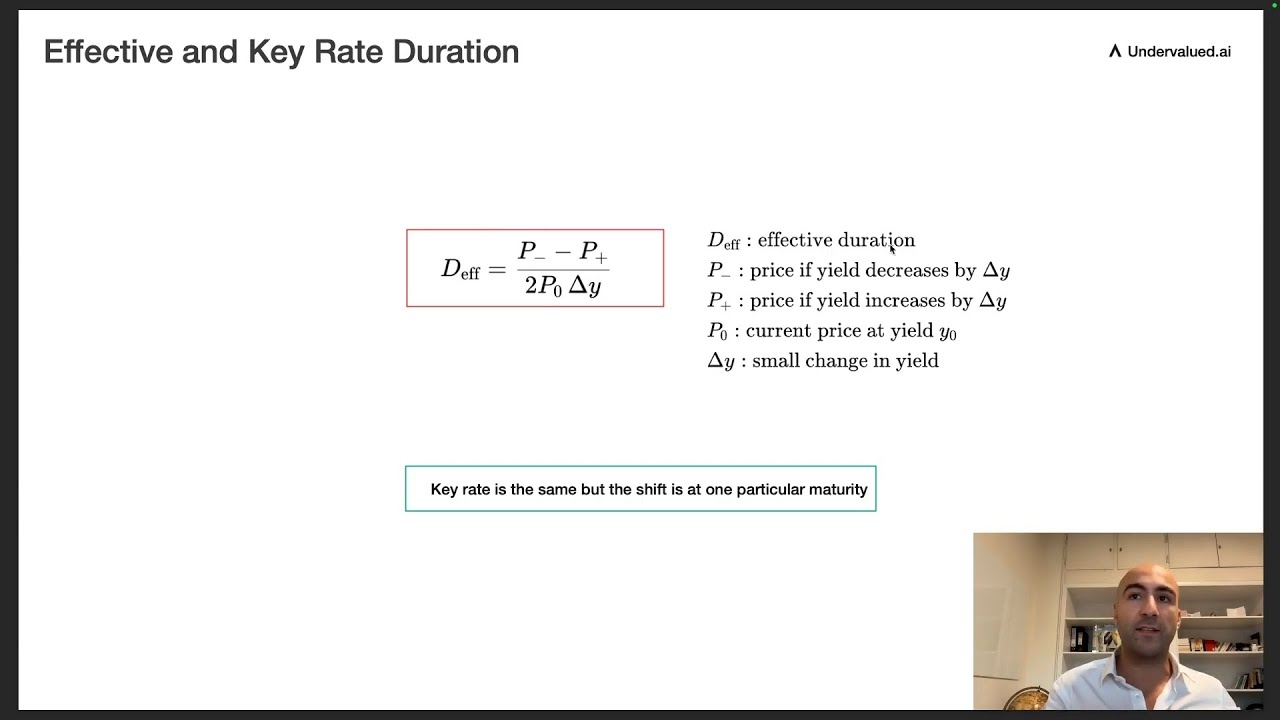

This clip introduces effective duration as an interest rate sensitivity measure for bonds whose cash flows can change when yields move, such as callable and putable bonds. It explains that effective duration is calculated by repricing the bond for small up and down shifts in yields and using the resulting price changes to estimate sensitivity. The segment then defines key rate duration as applying the same idea to individual points on the yield curve to analyze non parallel shifts by shocking specific maturities while holding others constant. For the full 2-hour CFA Level 1 crash course and all slides in one place, see the main video: • CFA Level 1 Crash Course: Key Concepts Ove... You can download all slides in PDF format using the link provided in the description of that main video. This content is for educational purposes only and is not affiliated with, endorsed by, or in any way officially connected to CFA Institute. #cfa #cfalevel1 #EffectiveDuration #KeyRateDuration #EmbeddedOptions #YieldCurveRisk #NonParallelShifts

Comments

![Эффект Джанибекова [Veritasium]](https://imager.clipsaver.ru/N9HlQ-XVnFk/max.jpg)