Vector Error Correction Model VECM Explained with Full Application скачать в хорошем качестве

Vector Error Correction Model VECM Explained with Full Application

15 часов назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Vector Error Correction Model VECM Explained with Full Application в качестве 4k

У нас вы можете посмотреть бесплатно Vector Error Correction Model VECM Explained with Full Application или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Vector Error Correction Model VECM Explained with Full Application в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Vector Error Correction Model VECM Explained with Full Application

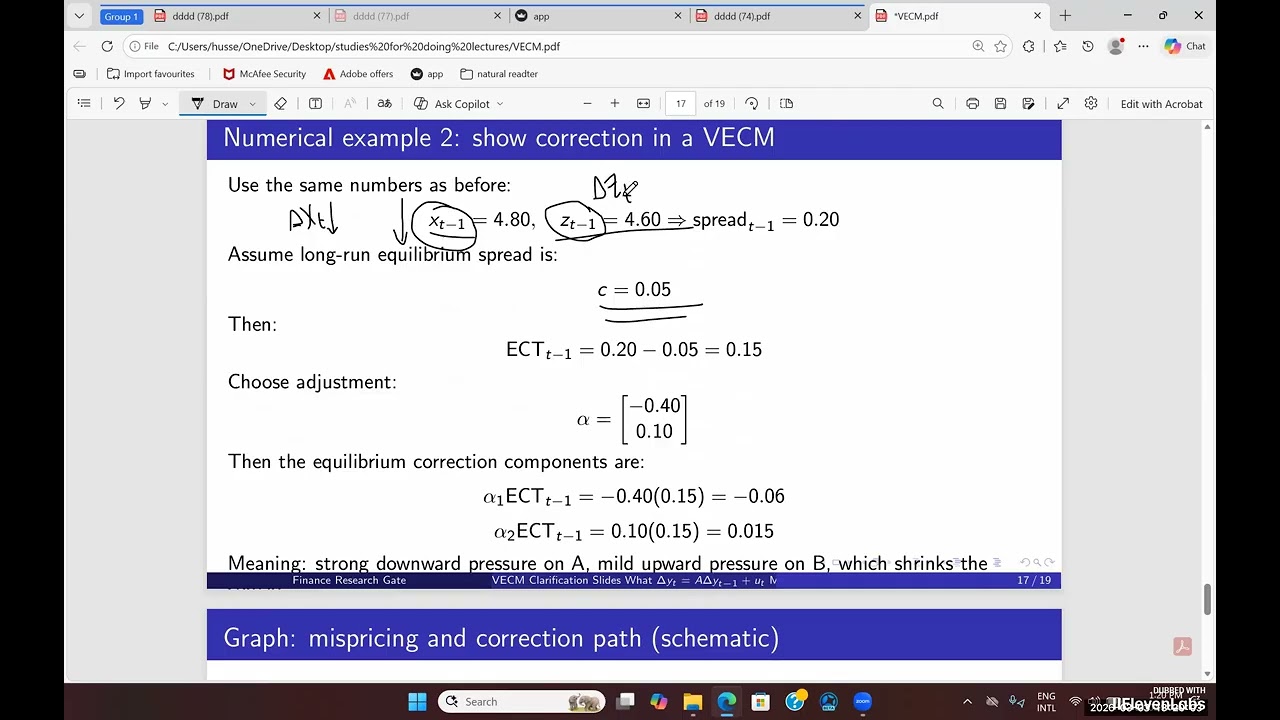

In this lecture, we walk step-by-step through estimating and interpreting a Vector Error Correction Model (VECM) using real financial data. We begin with the Johansen cointegration test to determine the cointegration rank and discuss how deterministic specifications (co, ci, li, lo) affect the long-run relationship. We then estimate the VECM, interpret the cointegration vector (β), and explain the adjustment coefficients (α) as speeds of correction toward long-run equilibrium. Special attention is given to the Error Correction Term (ECT) and how it drives short-run changes in each variable. We use the Finance Research Gate website. https://finresgate.com/app/

Comments

![Биология поведения человека. Лекция #1. Введение [Роберт Сапольски, 2010. Стэнфорд]](https://imager.clipsaver.ru/ik9t96SMtB0/max.jpg)