Calculating CPP's Break Even Point | Canada Pension Plan Explained скачать в хорошем качестве

Calculating CPP's Break Even Point | Canada Pension Plan Explained

4 года назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Calculating CPP's Break Even Point | Canada Pension Plan Explained в качестве 4k

У нас вы можете посмотреть бесплатно Calculating CPP's Break Even Point | Canada Pension Plan Explained или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Calculating CPP's Break Even Point | Canada Pension Plan Explained в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Calculating CPP's Break Even Point | Canada Pension Plan Explained

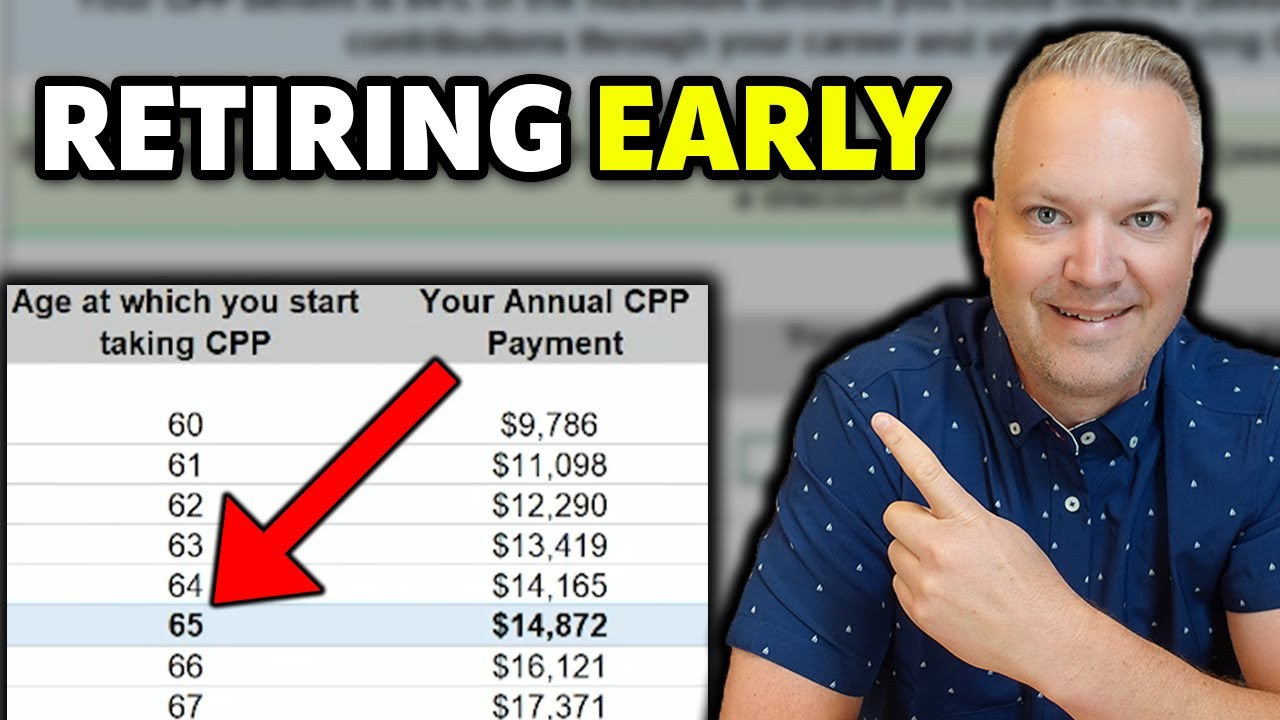

My Service Canada = https://www.canada.ca/en/employment-s... Episode one: • When Should You Start Collecting CPP? | Ca... Episode three: • 5 Reasons To Start Collecting CPP At 60 | ... Episode four: • 5 Reasons To Start Collecting CPP At 65 | ... Episode five: • 5 Reasons To Start Collecting CPP At 70 | ... Calculating the break even point on collecting your CPP is extremely important as it will help guide you to decide when to start collecting payments. Let's assume your CPP at age 65 is $1,000 per month...if you take CPP at age 60, your monthly amount will be $640 per month From age 60-65 you will have collected $38,400 The monthly difference between age 65 and age 60 is $360 ($1000-$640). Thus if we take the amount collected ($38,400) and divide it by the monthly difference ($360) we get 106.67 – let’s round that to 107. This means it will take 107 months to make back that difference, or 8 years and 11 months. So now we add 8 years and 11 months to age 65 and we come out with 73 years and 11 months. So, if you live past age 73 and 11 months, then it would make more sense to delay taking your CPP to age 65 versus taking it at age 60. Obviously there is much more to this than a simple calculation and we will cover these in our next 3 videos: taking CPP and 60, 65 and 70. Everyone’s situation is different, so the best plan for you likely is not the best plan for your neighbor. And remember, the breakeven point is just part of the calculation – if you were to invest the CPP payments from age 60 in a TFSA, then that would boost the overall amount you have later and further benefit taking the CPP earlier - but we all know you aren’t going to save your CPP payments! OAS Clawback: https://www.canada.ca/en/services/ben... CPP Benefits: https://www.canada.ca/en/services/ben... CPP Break Even Calculator: https://www.taxtips.ca/calculators/cp... ••••• If you have any questions about this video's topic or retirement planning in general, visit https://www.parallelwealth.com/ or use the links below to learn more about our services. ➡️Fee For Service Retirement Planning: https://www.parallelwealth.com/planning ➡️Retirement Income Program™: https://www.parallelwealth.com/invest... ➡️Parallel Wealth Masterclass: https://www.parallelwealth.com/education Additional 3rd Party Links and Resources: 🔗️Retirement Income for Life: Getting More without Saving More (Second Edition): https://amzn.to/3tvIdVN 🔗️Free Credit Report with Borrowell: https://bit.ly/borrowellPWFG 🔗️CPP Calculator: https://research-tools.pwlcapital.com... The above affiliate links are provided for your convenience. If you click on a link and end up purchasing a product or service, this channel may receive compensation for the referral. We have personally vetted each product and service we provide links to. ••••• DISCLAIMER: This presentation is for informational purposes only and should not be considered financial, investment, tax, or estate planning advice. All investments carry risk, and past performance does not guarantee future results. Any forward-looking statements are based on assumptions and may not reflect actual outcomes. The content on this channel is for educational purposes only and does not provide specific investment or planning recommendations. Viewers should consult a qualified professional for retirement, tax, or estate planning guidance. Parallel Wealth and Adam Bornn are not responsible for any decisions made based on this content.

Comments