Dependence Uncertainty and Risk - Prof. Paul Embrechts скачать в хорошем качестве

Dependence Uncertainty and Risk - Prof. Paul Embrechts

4 года назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Dependence Uncertainty and Risk - Prof. Paul Embrechts в качестве 4k

У нас вы можете посмотреть бесплатно Dependence Uncertainty and Risk - Prof. Paul Embrechts или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Dependence Uncertainty and Risk - Prof. Paul Embrechts в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Dependence Uncertainty and Risk - Prof. Paul Embrechts

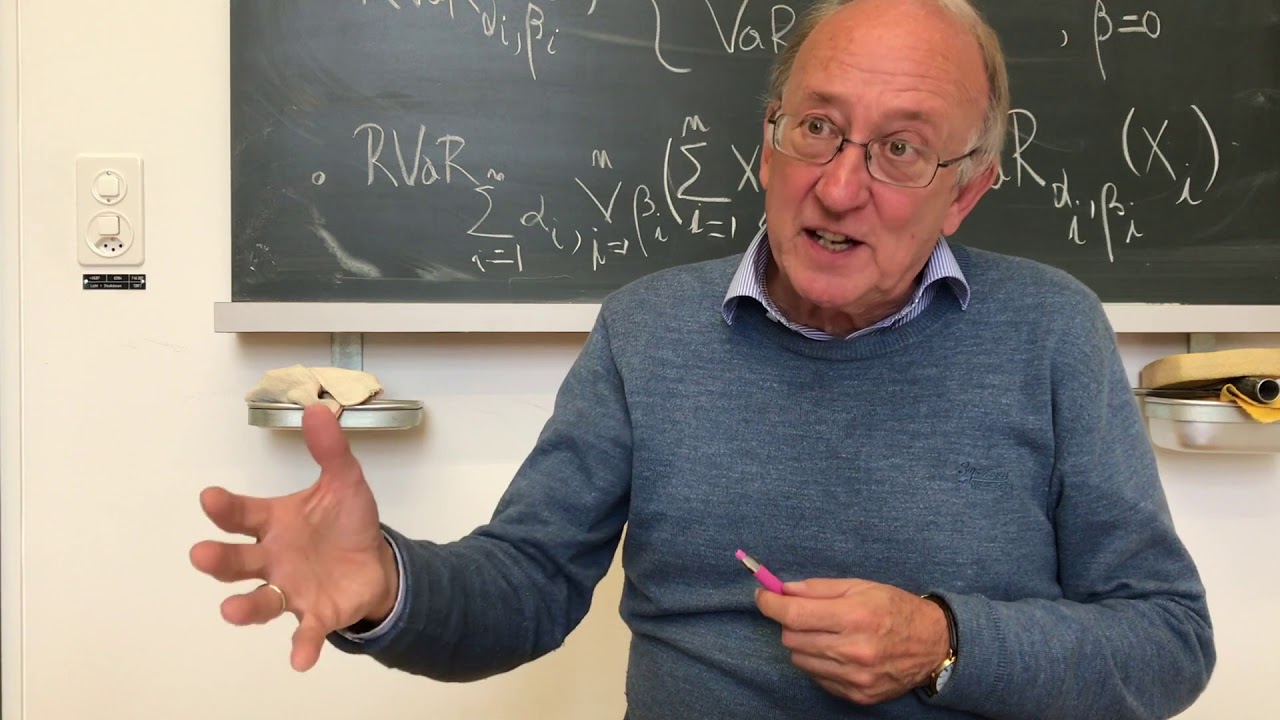

Abstract I will frame this talk in the context of what I refer to as the First and Second Fundamental Theorem of Quantitative Risk Management (1&2-FTQRM). An alternative subtitle for 1-FTQRM would be "Mathematical Utopia", for 2-FTQRM it would be "Wall Street Reality". I will mainly concentrate on uncertainty at the level of interdependence between risk factors and be interested in the derivation of extremal (inf-sup) bounds for risk measures, like Value-at-Risk and Expected Shortfall, of portfolios as functions of these factors. A workshop to commemorate the centenary of publication of Frank Knight’s "Risk, Uncertainty, and Profit" and John Maynard Keynes’ “A Treatise on Probability” This workshop is organised by the University of Oxford and supported by The Alan Turing Institute. For further details and regular updates, please visit the official event website About the event The year 2021 marks the centenary of two monumental publications in economics and probability theory, namely Risk, Uncertainty, and Profit by Frank Hyneman Knight and A Treatise on Probability by John Maynard Keynes. In Risk, Uncertainty, and Profit, Knight put forward the vital difference between risk, where empirical evaluation of unknown outcomes can still be applicable, and uncertainty, where no quantified measurement is valid but subjective estimate. In A Treatise on Probability, Keynes argued that the concept of probability should be about the logical implication from premises to hypotheses, in contrast to the classical quantified perspective of probability. The fundamental uncertainty proposed in both works has then deeply influenced the development of economic and probability theory in the past century and it still resonates with our lives today, considering the ups and downs that the world economy is experiencing. This workshop is a tribute to their invaluable legacy. Speakers: Professor Dr Francesca Biagini, Ludwig Maximilian University of Munich Professor Sara Biagini, LUISS Guido Carli Professor Simon Blackburn, Trinity College, Cambridge Professor Dr Paul Embrechts, ETH Zurich Professor Itzhak Gilboa, HEC Paris Professor Lars Hansen, University of Chicago Professor Fabio Maccheroni, Bocconi University Professor Massimo Marinacci, Bocconi University Professor Marcel Nutz, Columbia University Professor Shige Peng, Shandong University Professor Dr Frank Riedel, Bielefeld University Professor Ross Emmett, Arizona State University Organizers: Sam Cohen, Lars Hansen, Tomasz R. Bielecki, Igor Cialenco, Mike Tehranchi and Haoyang Cao

Comments

-

4 года назад

4 года назад

-

7 лет назад

7 лет назад

-

10 лет назад

10 лет назад

-

6 лет назад

6 лет назад

-

4 года назад

4 года назад

-

1 день назад

1 день назад

-

4 часа назад

4 часа назад

-

2 года назад

2 года назад

-

Трансляция закончилась 7 дней назад

Трансляция закончилась 7 дней назад

-

1 год назад

1 год назад

-

1 день назад

1 день назад

-

2 дня назад

2 дня назад

-

1 год назад

1 год назад

-

3 месяца назад

3 месяца назад

-

5 лет назад

5 лет назад

-

2 года назад

2 года назад

-

1 день назад

1 день назад

-

3 года назад

3 года назад

-

Трансляция закончилась 14 часов назад

Трансляция закончилась 14 часов назад

-

7 дней назад

7 дней назад