Principles of Marine Insurance скачать в хорошем качестве

Principles of Marine Insurance

6 месяцев назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Principles of Marine Insurance в качестве 4k

У нас вы можете посмотреть бесплатно Principles of Marine Insurance или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Principles of Marine Insurance в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Principles of Marine Insurance

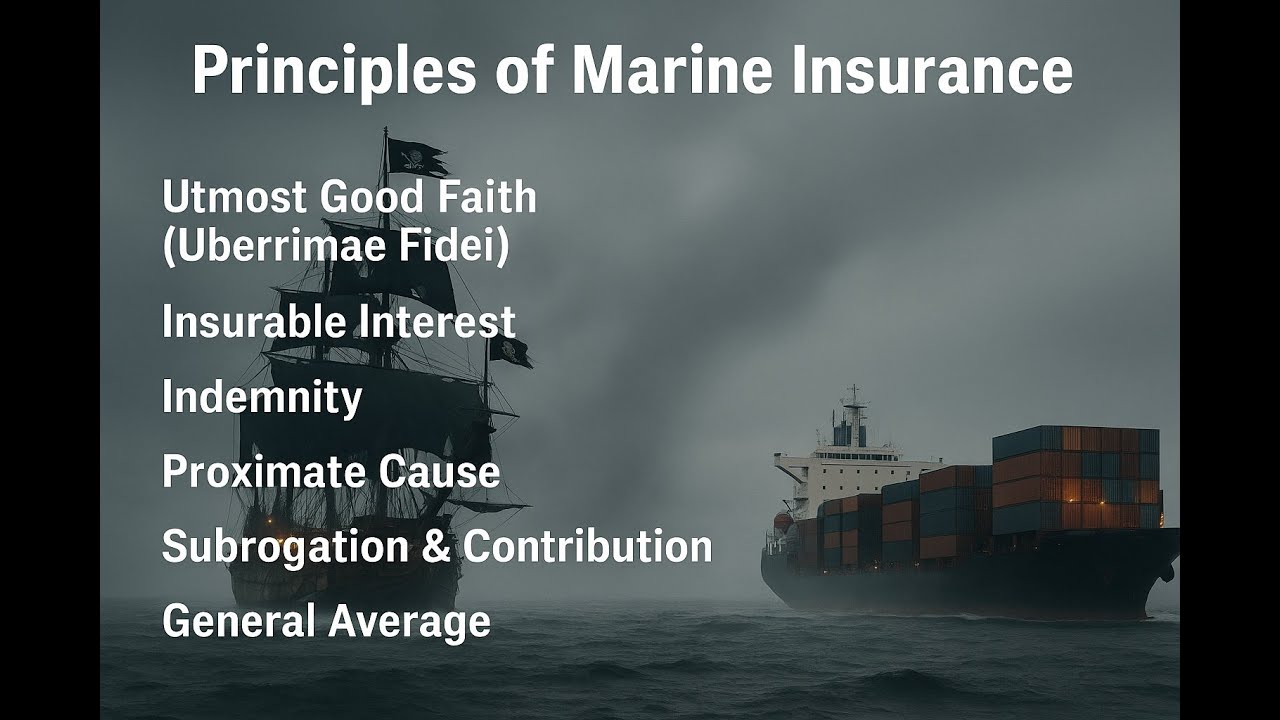

1. Principle of Utmost Good Faith (Uberrimae Fidei) The principle of utmost good faith requires both the insurer and the insured to act with complete honesty and transparency when entering into an insurance contract. This means all material facts—information that could influence the insurer’s decision to accept the risk or determine the premium—must be disclosed. Failure to do so can render the policy void. Insurers rely on accurate information to assess risk and set premiums. Concealing facts distorts this assessment, leading to unfair advantages or unjust denials of claims. 2. Principle of Insurable Interest The insured must have a financial stake in the subject matter of the insurance policy at the time of the loss. This ensures that insurance is used as a tool for compensation rather than speculation or gambling. This principle prevents individuals from insuring property in which they have no financial interest, which could otherwise lead to fraudulent claims. 3. Principle of Indemnity Marine insurance is designed to compensate the insured for their actual financial loss, not to provide a profit. The insured should be restored to the same financial position they were in before the loss occurred. This principle ensures that insurance remains a risk-mitigation tool rather than a means of financial gain. 4. Principle of Subrogation Once the insurer compensates the insured for a loss, the insurer inherits the insured’s legal rights to recover the amount from any third party responsible for the damage. Subrogation prevents the insured from double recovery (claiming from both the insurer and the negligent party) and helps insurers offset their losses. 5. Principle of Contribution If the same risk is insured with multiple insurers, each insurer contributes proportionately to the claim, ensuring the insured does not profit from overlapping policies. This prevents over-insurance and ensures fair distribution of liability among insurers. 6. Principle of Proximate Cause (Causa Proxima) The insurer is only liable if the dominant and most direct cause of the loss is a covered peril under the policy. This principle ensures that insurers only pay for losses caused by risks they agreed to cover. 7. Principle of Loss Minimization After the insured event occurs, the insured must take all reasonable steps to minimize the loss, even though the loss is covered. Example: If water enters the cargo hold during a storm, the ship's crew must try to pump the water out or shift the cargo to prevent further damage. Failing to do so may reduce the claim amount. 8. Principle of Contribution to General Average When voluntary sacrifice or expenditure is made to save the maritime venture, the loss is shared proportionately by all parties. Example: If a container of goods is thrown overboard to lighten the ship during a storm, all cargo owners and the shipowner share the loss, not just the owner of the lost cargo. This is settled under the General Average principle, a unique feature of marine insurance. 9. Principle of Warranties Warranties are conditions that must be strictly complied with. They can be express (stated in the policy) or implied (assumed by law). Example: A warranty may require that a vessel must sail within a certain date or be seaworthy. If a vessel departs late or with a known mechanical defect, and a loss occurs, the insurer may deny the claim for breach of warranty. 10. Principle of Seaworthiness (Implied Warranty) There is an implied warranty in every marine insurance contract that the ship must be seaworthy at the start of the voyage. Example: If the hull is corroded or lifeboats are missing at the start of the voyage, the ship is unseaworthy. If a loss occurs due to these issues, the insurer may not pay the claim

Comments