How to Research the Historical Options Straddle Strategy Performance Around Earnings скачать в хорошем качестве

How to Research the Historical Options Straddle Strategy Performance Around Earnings

2 года назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: How to Research the Historical Options Straddle Strategy Performance Around Earnings в качестве 4k

У нас вы можете посмотреть бесплатно How to Research the Historical Options Straddle Strategy Performance Around Earnings или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон How to Research the Historical Options Straddle Strategy Performance Around Earnings в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

How to Research the Historical Options Straddle Strategy Performance Around Earnings

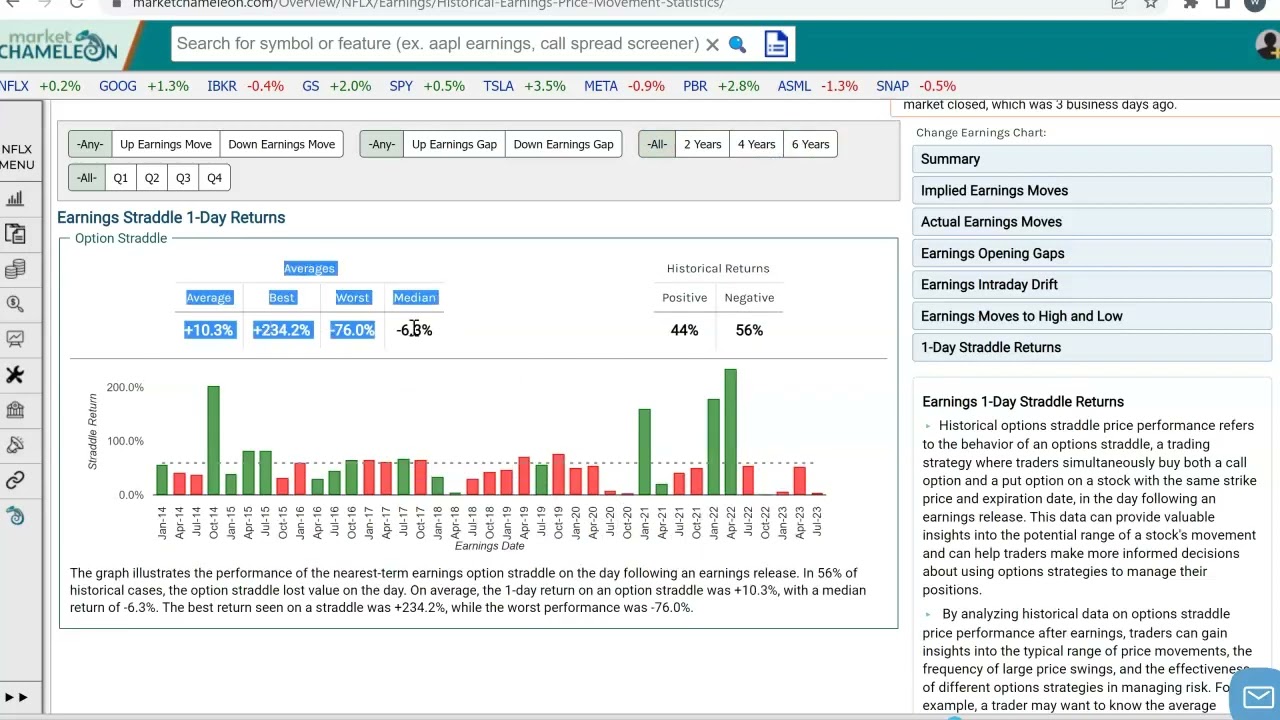

In this video we demonstrate hwo to use a tool that tracks and reveals valuable statistics on the historical performance of options straddles for a specific stock around earnings. This tool offers invaluable insights into the behavior of options straddles, a popular trading strategy involving simultaneous purchases of both a call option and a put option on a stock with the same strike price and expiration date, in the day following an earnings release. By leveraging historical data on options straddle price performance after earnings, traders gain valuable knowledge about the typical range of price movements, the frequency of significant price swings, and the effectiveness of various options strategies in risk management. As traders, understanding the average percentage move of an underlying stock after an earnings release and the probability of the options straddle resulting in a profit or loss can significantly impact decision-making and risk management strategies. Throughout this tutorial, we'll walk you through the process of analyzing the historical options straddle price performance data, equipping you with the skills to make more informed decisions when employing options strategies to manage the risk associated with holding a position. We used NFLX historical data in this example https://marketchameleon.com/Overview/...

Comments

-

Трансляция закончилась 2 года назад

Трансляция закончилась 2 года назад

-

6 лет назад

6 лет назад

-

11 месяцев назад

11 месяцев назад

-

1 месяц назад

1 месяц назад

-

23 часа назад

23 часа назад

-

2 дня назад

2 дня назад

-

3 года назад

3 года назад

-

2 года назад

2 года назад

-

1 месяц назад

1 месяц назад

-

3 дня назад

3 дня назад

-

1 день назад

1 день назад

-

2 года назад

2 года назад

-

11 лет назад

11 лет назад

-

3 года назад

3 года назад

-

2 дня назад

2 дня назад

-

Трансляция закончилась 7 дней назад

Трансляция закончилась 7 дней назад

-

1 месяц назад

1 месяц назад

-

3 года назад

3 года назад

-

1 год назад

1 год назад

-

Трансляция закончилась 3 недели назад

Трансляция закончилась 3 недели назад