CBIC Clarifies Post-Sale Discounts under GST | ITC, Consideration & Promotional Services Explained скачать в хорошем качестве

CBIC Clarifies Post-Sale Discounts under GST | ITC, Consideration & Promotional Services Explained

4 месяца назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: CBIC Clarifies Post-Sale Discounts under GST | ITC, Consideration & Promotional Services Explained в качестве 4k

У нас вы можете посмотреть бесплатно CBIC Clarifies Post-Sale Discounts under GST | ITC, Consideration & Promotional Services Explained или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон CBIC Clarifies Post-Sale Discounts under GST | ITC, Consideration & Promotional Services Explained в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

CBIC Clarifies Post-Sale Discounts under GST | ITC, Consideration & Promotional Services Explained

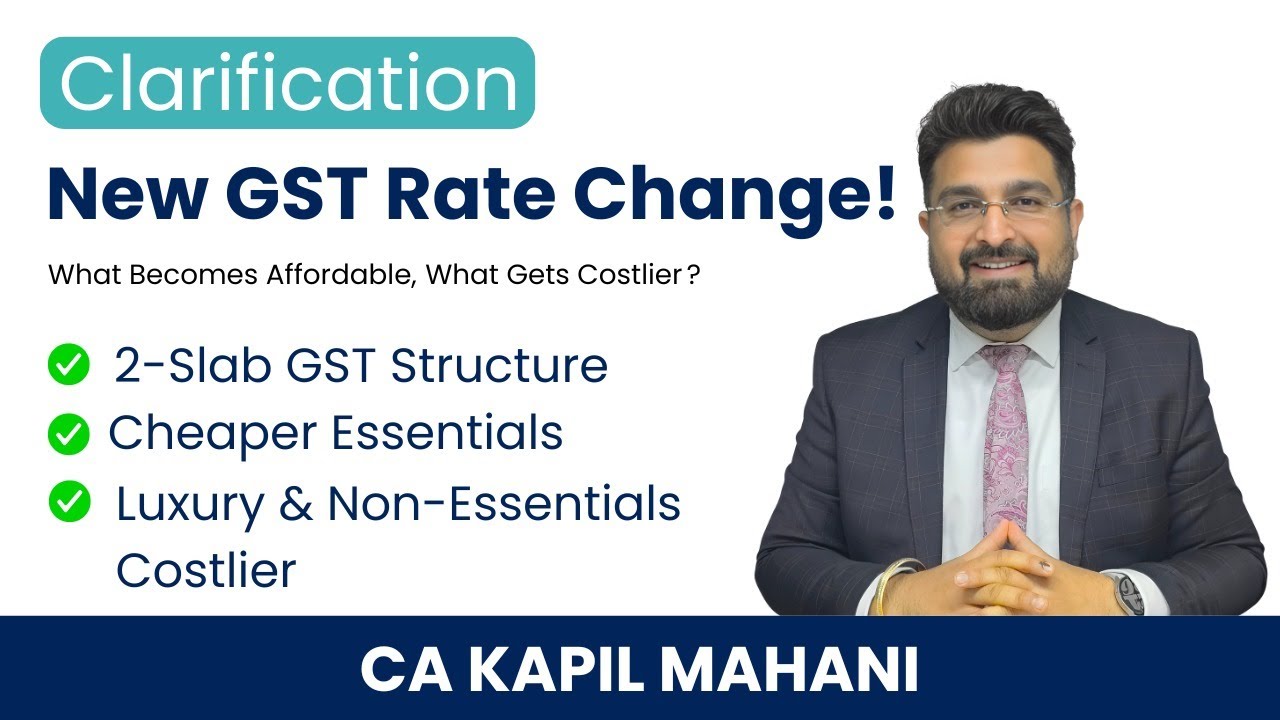

CBIC Clarifies Post-Sale Discounts under GST | ITC, Consideration & Promotional Services Explained Main Content (5–45 sec): “👉 First, if a supplier issues a financial or commercial credit note, the buyer can still take full ITC. No reversal is needed. 👉 Second, post-sale discounts between manufacturers and dealers are generally not taxable consideration. They are just price reductions. 👉 Third, only when dealers provide specific promotional services like advertising, branding, or campaigns under an agreement, GST will apply.” Close (45–60 sec): “In summary: ITC remains safe, discounts are not taxable, but promotional services are. This is Kapil Mahani, simplifying GST for you.” 🎥 Detailed Video Script (4–6 min) Intro (0:00 – 0:30) “Hello everyone, I’m Kapil Mahani. The CBIC has just issued Circular No. 251/08/2025 dated 12th September 2025. It clarifies important issues around post-sale or secondary discounts under GST. Let’s break this down step by step.” Part 1 – ITC on Discounts (0:30 – 1:30) “One of the biggest doubts was whether ITC has to be reversed if the buyer pays less due to a financial or commercial credit note. The clarification is clear: No ITC reversal is required. The supplier’s tax liability doesn’t reduce, so your ITC stays intact.” Part 2 – Discounts vs. Consideration (1:30 – 2:30) “Next, whether a manufacturer’s discount to a dealer is treated as consideration for sales to the end customer. The circular says: Normally No, because the dealer operates on a principal-to-principal basis. But — if the manufacturer has an agreement with the end customer for a discount, then the dealer’s sale at that reduced price may be seen as inducement, and forms part of consideration.” Part 3 – Promotional Services (2:30 – 4:00) “Another confusion was: are post-sale discounts really payment for promotional activities? The answer: Not by default. Discounts just reduce the price of goods. However, if the dealer explicitly agrees to run ads, exhibitions, co-branding, or customer support for the manufacturer, that’s a separate supply of services. In that case, GST applies.” Part 4 – Key Takeaways (4:00 – 5:30) “So what does this mean for businesses? ✅ You can claim full ITC even with financial/ commercial credit notes. 🚫 Post-sale discounts are not taxable unless tied to an agreement. ⚠️ If agreements mention promotional activities, GST will apply on that service.” Closing (5:30 – 6:00) “This circular brings much-needed clarity on post-sale discounts. Businesses should review their dealer agreements and ensure compliance. I’m Kapil Mahani, and I’ll keep simplifying GST for you.” Visit now- https://cretumadvisory.com/ Linkdin Page : https://bit.ly/37vz7w9 PS: Don't forget to SUBSCRIBE for more trusted and updated videos.

Comments

-

4 месяца назад

4 месяца назад

-

3 месяца назад

3 месяца назад

-

Трансляция закончилась 3 месяца назад

Трансляция закончилась 3 месяца назад

-

Трансляция закончилась 1 день назад

Трансляция закончилась 1 день назад

-

3 дня назад

3 дня назад

-

9 месяцев назад

9 месяцев назад

-

2 недели назад

2 недели назад

-

11 месяцев назад

11 месяцев назад

-

2 года назад

2 года назад

-

8 месяцев назад

8 месяцев назад

-

Трансляция закончилась 8 месяцев назад

Трансляция закончилась 8 месяцев назад

-

3 месяца назад

3 месяца назад

-

1 день назад

1 день назад

-

Трансляция закончилась 4 часа назад

Трансляция закончилась 4 часа назад

-

7 месяцев назад

7 месяцев назад

-

9 месяцев назад

9 месяцев назад

-

1 месяц назад

1 месяц назад

-

9 месяцев назад

9 месяцев назад

-

2 месяца назад

2 месяца назад

-

2 месяца назад

2 месяца назад