#8 PORTFOLIO EVALUATION METHODS | Sharpe Ratio, Treynor Ratio & Jensen's Alpha | CA/CMA Final AFM скачать в хорошем качестве

#8 PORTFOLIO EVALUATION METHODS | Sharpe Ratio, Treynor Ratio & Jensen's Alpha | CA/CMA Final AFM

1 месяц назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: #8 PORTFOLIO EVALUATION METHODS | Sharpe Ratio, Treynor Ratio & Jensen's Alpha | CA/CMA Final AFM в качестве 4k

У нас вы можете посмотреть бесплатно #8 PORTFOLIO EVALUATION METHODS | Sharpe Ratio, Treynor Ratio & Jensen's Alpha | CA/CMA Final AFM или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон #8 PORTFOLIO EVALUATION METHODS | Sharpe Ratio, Treynor Ratio & Jensen's Alpha | CA/CMA Final AFM в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

#8 PORTFOLIO EVALUATION METHODS | Sharpe Ratio, Treynor Ratio & Jensen's Alpha | CA/CMA Final AFM

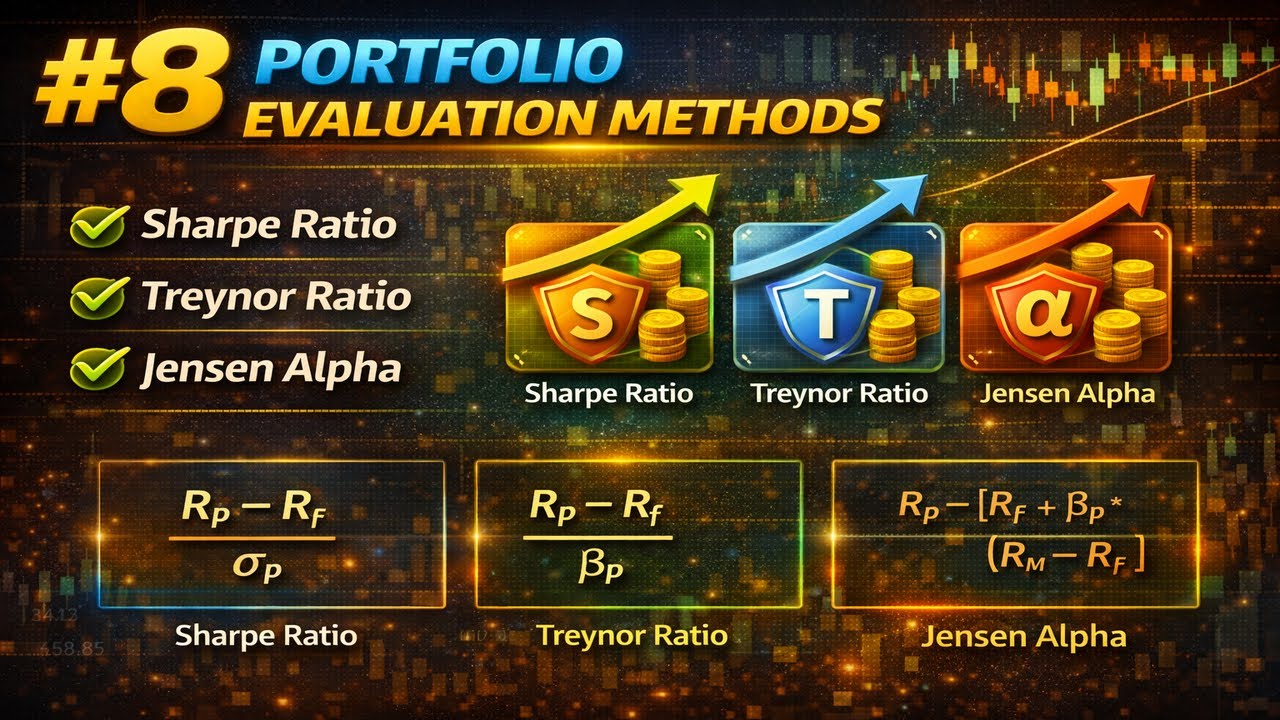

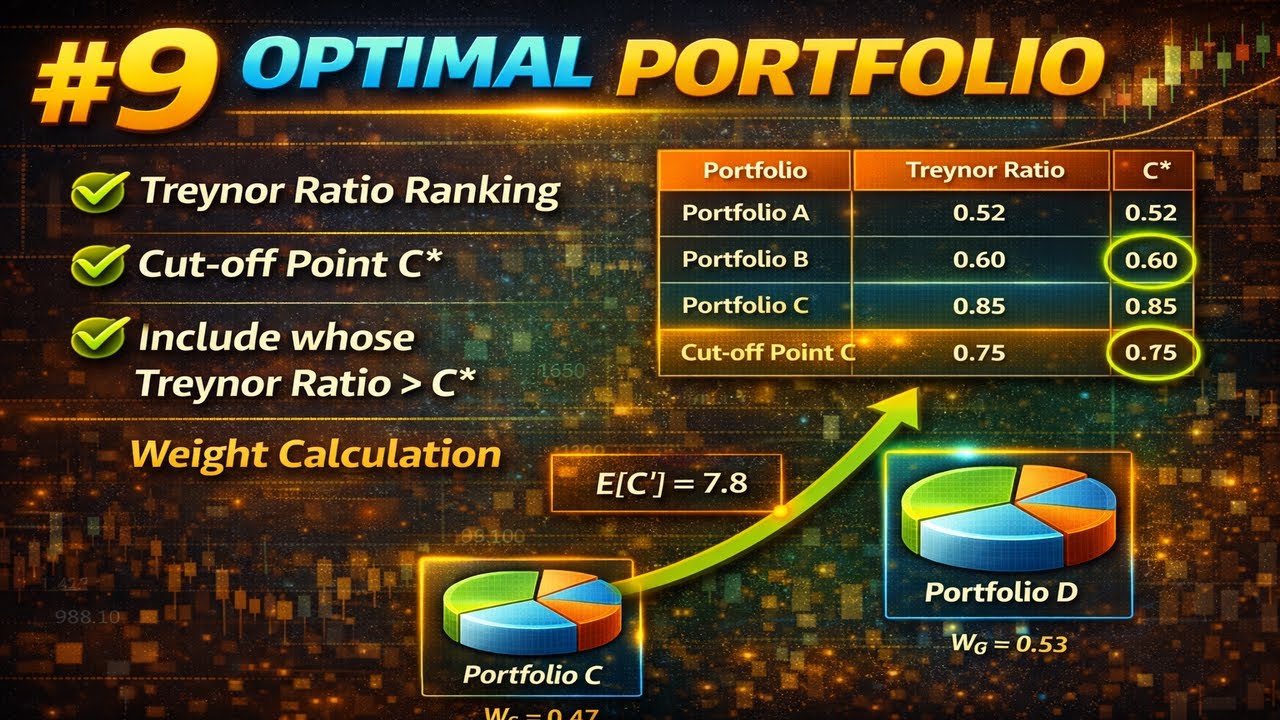

You’ve built the portfolio—now, how do you know if it’s actually performing well? 📊 In this 8th video of our AFM Portfolio Management series, we master the three legendary ratios used to evaluate investment performance: Sharpe Ratio, Treynor Ratio, and Jensen's Alpha. Understanding these is the difference between simply seeing returns and understanding "Risk-Adjusted" returns. This session is essential for CA Final and CMA students, as it often appears in practical exam questions alongside CAPM and Portfolio Theory. 📌What you will learn in this video: Sharpe Ratio: Measuring return per unit of Total Risk (Standard Deviation). Treynor Ratio: Measuring return per unit of Market Risk (Beta). Jensen’s Alpha: Calculating the "Excess Return"—did the manager beat the market? Comparative Analysis: When to use Sharpe vs. Treynor (Diversified vs. Undiversified portfolios). Step-by-Step Practical: Solving an evaluation problem with real numbers. __________________ Subscribe and hit the bell icon! In Video #9, we will dive into OPTIMAL PORTFOLIO! #PortfolioEvaluation #AFM #SharpeRatio #TreynorRatio #JensensAlpha #CAFinal #CMAFinal #PortfolioPerformance #FinanceSimplified #NandJhaAFM #InvestmentAnalysis Resources: ✅ Watch Previous Video (ARBITRAGE PRICING THEORY) : • #7 ARBITRAGE PRICING THEORY (APT) | CAPM -... AFM Full Playlist: • Portfolio Management (AFM) 📈 Join our Telegram for Notes: https://t.me/CANandJha

Comments

-

1 месяц назад

1 месяц назад

-

![[95% Qs from Here] CUSTOMS VALUATION | PART 1 | Rule 10 Explained | CA/CMA Final IDT May 2026](https://imager.clipsaver.ru/u2Qjeuvdhxo/max.jpg) 2 недели назад

2 недели назад

-

-

-

12 дней назад

12 дней назад

-

Трансляция закончилась 10 часов назад

Трансляция закончилась 10 часов назад

-

1 день назад

1 день назад

-

23 часа назад

23 часа назад

-

2 часа назад

2 часа назад

-

20 часов назад

20 часов назад

-

Трансляция закончилась 1 день назад

Трансляция закончилась 1 день назад

-

3 недели назад

3 недели назад

-

4 дня назад

4 дня назад

-

Трансляция закончилась 10 часов назад

Трансляция закончилась 10 часов назад

-

22 часа назад

22 часа назад

-

Трансляция закончилась 8 лет назад

Трансляция закончилась 8 лет назад

-

Трансляция закончилась 23 часа назад

Трансляция закончилась 23 часа назад

-

1 месяц назад

1 месяц назад

-

2 месяца назад

2 месяца назад

-

1 день назад

1 день назад