What Are Transaction Costs скачать в хорошем качестве

What Are Transaction Costs

9 месяцев назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: What Are Transaction Costs в качестве 4k

У нас вы можете посмотреть бесплатно What Are Transaction Costs или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон What Are Transaction Costs в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

What Are Transaction Costs

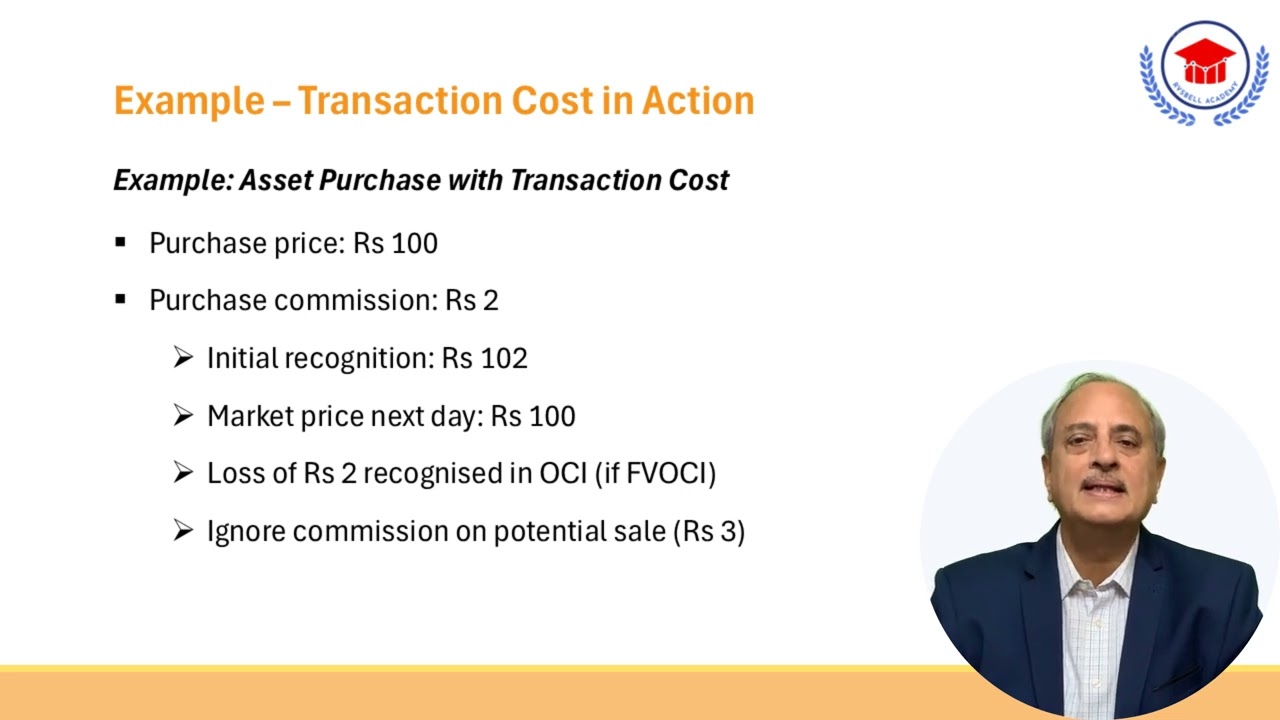

Transaction costs include fees and commission paid to agents (including employees acting as selling agents), advisers, brokers and dealers, levies by regulatory agencies and security exchanges, and transfer taxes and duties. Transaction costs do not include debt premiums or discounts, financing costs or internal administrative or holding costs. Financial assets measured not at FVPL For financial assets not measured at fair value through profit or loss, transaction costs are added to the fair value at initial recognition. For financial liabilities, transaction costs are deducted from the fair value at initial recognition. Financial assets at amortised cost For financial instruments that are measured at amortised cost, transaction costs are subsequently included in the calculation of amortised cost using the effective interest method and, in effect, amortised through profit or loss over the life of the instrument. Financial assets at FVOCI For financial instruments that are measured at fair value through other comprehensive income transaction costs are recognised in other comprehensive income as part of a change in fair value at the next re-measurement. If the financial asset is measured those transaction costs are amortised to profit or loss using the effective interest method and, in effect, amortised through profit or loss over the life of the instrument. Example An entity acquires a financial asset for Rs 100 plus a purchase commission of Rs 2. Initially, the entity recognises the asset at Rs 102. The reporting period ends one day later, when the quoted market price of the asset is Rs 100. If the asset were sold, a commission of Rs 3 would be paid. On that date, the entity measures the asset at Rs 100 (without regard to the possible commission on sale) and recognises a loss of Rs 2 in other comprehensive income. If the financial asset is measured at fair value through other comprehensive income, the transaction costs are amortised to profit or loss using the effective interest method. Transaction costs expected to be incurred on transfer or disposal of a financial instrument are not included in the measurement of the financial instrument.

Comments

![Леонид АГУТИН - ЛУЧШИЕ ПЕСНИ 2025 [СБОРНИК] @ХитЗаХитом](https://imager.clipsaver.ru/lAWkb8GArIw/max.jpg)