44AD, 44ADA, 44AE Merged?| Income Tax Act 1961 vs 2025 – Section 58| Big Change in Presumptive Tax скачать в хорошем качестве

44AD, 44ADA, 44AE Merged?| Income Tax Act 1961 vs 2025 – Section 58| Big Change in Presumptive Tax

12 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: 44AD, 44ADA, 44AE Merged?| Income Tax Act 1961 vs 2025 – Section 58| Big Change in Presumptive Tax в качестве 4k

У нас вы можете посмотреть бесплатно 44AD, 44ADA, 44AE Merged?| Income Tax Act 1961 vs 2025 – Section 58| Big Change in Presumptive Tax или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон 44AD, 44ADA, 44AE Merged?| Income Tax Act 1961 vs 2025 – Section 58| Big Change in Presumptive Tax в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

44AD, 44ADA, 44AE Merged?| Income Tax Act 1961 vs 2025 – Section 58| Big Change in Presumptive Tax

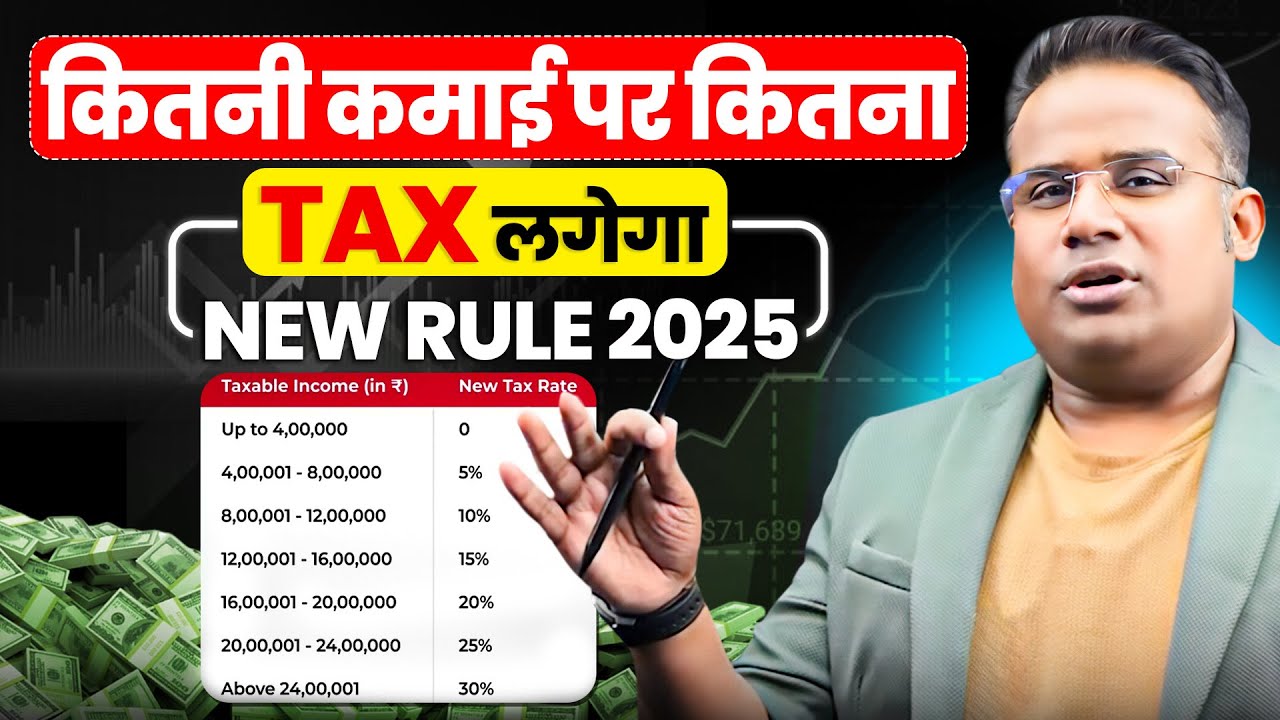

Latest Amendment Section 58 Income Tax Act 1961 vs 2025 | 44AD vs 44ADA vs 44AE (Presumptive Taxation 2026) Explained in Simple Language #incometax #cadeveshthakur #incometaxact2025 @cadeveshthakur Section 58 under the Income Tax Act 2025 introduces a major structural change in Presumptive Taxation in India. From 1 April 2026, Sections 44AD, 44ADA and 44AE are consolidated under Section 58 – Presumptive Taxation. In this detailed video, I explain the complete framework of Section 58 Income Tax Act 2025, including how it replaces earlier provisions and what it means for business owners, professionals, transport operators and tax practitioners. 🔍 What You Will Learn in This Video: ✔ Section 58 Presumptive Taxation Explained ✔ 44AD New Rule 2026 (6% / 8% Rule) ✔ 44ADA 50 Percent Rule for Professionals ✔ 44AE Fixed Income Rule for Goods Carriage Business ✔ Section 58 Replaces 44AD, 44ADA & 44AE ✔ 5 Year Lock in Rule under Business Category ✔ Digital Receipt 5 Percent Condition ✔ Turnover Limits – ₹2 Cr / ₹3 Cr / ₹50L / ₹75L ✔ Audit Trigger under Section 58 ✔ Income Computation under Section 58 ✔ Effective from 1 April 2026 – Tax Changes Video Timeline – Income Tax Act 2025 | Section 58 & Presumptive Taxation Explained 00:00 – Introduction to New Section 58 under Income Tax Act 2025 | Key Amendments Explained 01:09 – Structural Breakdown of Section 58 | Clauses & Applicability 03:09 – Section 44AD Explained | Presumptive Taxation for Small Businesses 05:46 – Section 44AE Explained | Tax Provisions for Goods Transport Business 07:18 – Section 44ADA Explained | Presumptive Tax for Professionals (CA, Doctor, Lawyer, etc.) 08:50 – General Impact of Section 58 | Definitions, Scope & Tax Implications 11:22 – Judicial Principles & Comparison | Section 44AD vs 44AE vs 44ADA Analysis Why This Update is Important The Presumptive Taxation 2026 framework under Section 58 is not just a renumbering of 44AD, 44ADA and 44AE. It restructures compliance, clarifies eligibility conditions and introduces strict application of audit triggers. This update is crucial for: • Small Business Owners • Professionals (Doctors, Lawyers, CAs, Consultants) • Transport Business Owners • Accountants & Tax Practitioners • CA, CS, CMA Students • Anyone preparing for Income Tax Amendment 2025 Understanding the difference between 44AD vs Section 58, 44ADA vs Section 58, and 44AE vs Section 58 is essential before opting for presumptive taxation. Important Clarifications Covered: • Is 44AD removed? • What changes under Income Tax Act 2025? • How does Section 58 impact business income computation? • When does audit become mandatory? • What is the 5% cash condition? • Is presumptive taxation always tax saving? Presumptive taxation under Section 58 is a compliance relief mechanism — not automatically a tax saving strategy. Applicable from: 1 April 2026 Law Reference: Section 58 – Income Tax Act 2025 🔗 Connect with CA Devesh Thakur Stay updated with structured Income Tax learning, section-wise breakdowns, practical insights, and regular tax updates across platforms: 📌 Instagram: / cadeveshthakur 📌 YouTube: / @cadeveshthakur 📌 LinkedIn: / cadeveshthakur 📌 Facebook: / cadevesh 📌 X (Twitter): https://x.com/cadeveshthakur 📌 Pinterest: / cadevesht 📌 Threads: https://www.threads.com/@cadeveshthakur 📌 WhatsApp Channel: https://whatsapp.com/channel/0029Va6G... Subscribe for structured updates on Income Tax Law 2026, tax planning strategies and professional tax analysis. Section 58 Income Tax, Presumptive Taxation 2025, 44AD limit, 44ADA professional income, 44AE transport business tax, Income Tax Amendment 2025 India

Comments

-

10 дней назад

10 дней назад

-

7 дней назад

7 дней назад

-

Трансляция закончилась 1 день назад

Трансляция закончилась 1 день назад

-

2 недели назад

2 недели назад

-

Трансляция закончилась 1 час назад

Трансляция закончилась 1 час назад

-

8 дней назад

8 дней назад

-

5 часов назад

5 часов назад

-

2 года назад

2 года назад

-

2 недели назад

2 недели назад

-

8 часов назад

8 часов назад

-

8 дней назад

8 дней назад

-

7 лет назад

7 лет назад

-

2 недели назад

2 недели назад

-

1 год назад

1 год назад

-

5 месяцев назад

5 месяцев назад

-

3 недели назад

3 недели назад

-

1 год назад

1 год назад

-

1 день назад

1 день назад

-

3 недели назад

3 недели назад

-

3 месяца назад

3 месяца назад