Leaving Canada - Cutting Ties, Departure Taxes? скачать в хорошем качестве

Leaving Canada - Cutting Ties, Departure Taxes?

Трансляция закончилась 14 часов назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Leaving Canada - Cutting Ties, Departure Taxes? в качестве 4k

У нас вы можете посмотреть бесплатно Leaving Canada - Cutting Ties, Departure Taxes? или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Leaving Canada - Cutting Ties, Departure Taxes? в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Leaving Canada - Cutting Ties, Departure Taxes?

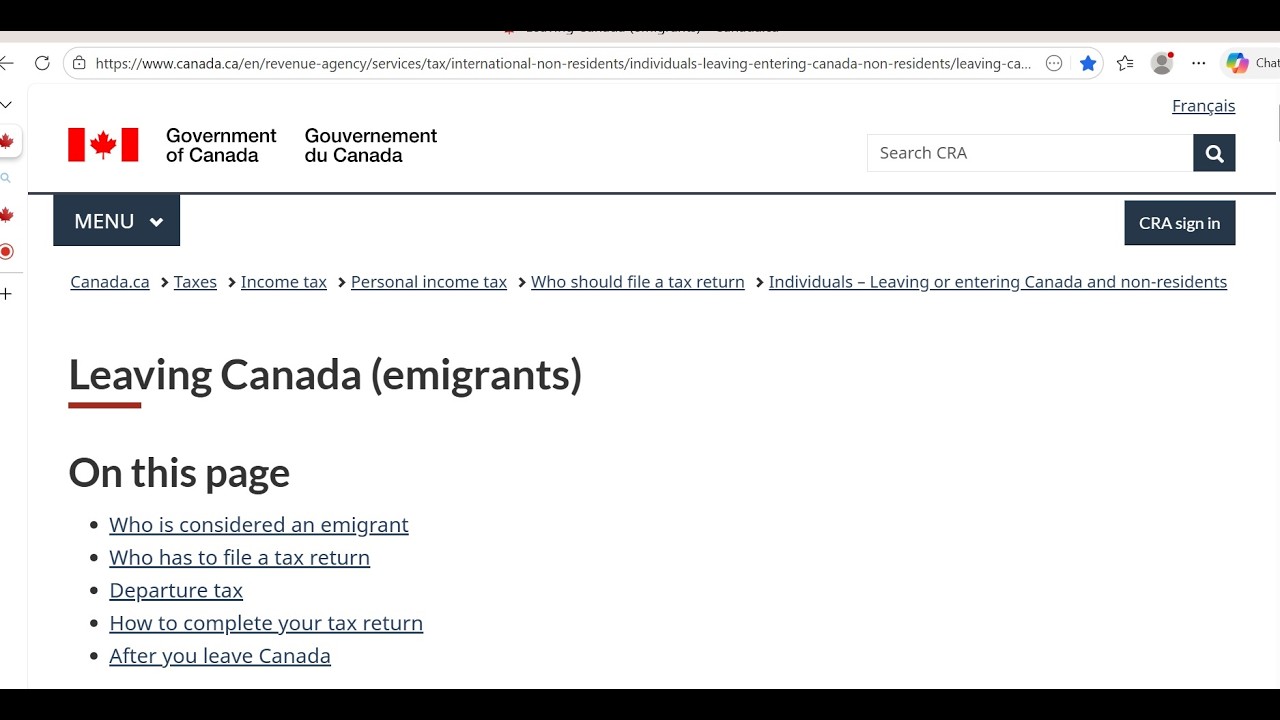

Canada has what’s commonly called a departure tax (or exit tax) when you leave the country and become a non-resident for tax purposes. How it works • When you emigrate, the Canada Revenue Agency (CRA) treats it as if you sold most of your property at fair market value the day before you leave — even if you didn’t actually sell anything. • This triggers capital gains tax on any unrealized appreciation of those assets. • You must file a final Canadian tax return for the year you leave, reporting this deemed disposition. Assets affected • Included: Investments (stocks, bonds, mutual funds), shares in private corporations, certain trusts, and other property. • Excluded: Canadian real estate, RRSPs, pensions, and certain other registered accounts — these are not subject to departure tax but may be taxed later when withdrawn. Key considerations • Planning opportunities: Some people restructure their holdings before leaving to minimize departure tax (e.g., selling assets while still a resident, or using exemptions). • Foreign tax credits: If you later pay tax in your new country of residence, Canada’s system allows credits to reduce double taxation. In short, yes — leaving Canada can trigger an exit tax, but it applies mainly to investments and certain property, not to everything you own. Would you like me to break down specific strategies people use to reduce or defer departure tax (like exemptions or elections), or keep it at a high-level overview? When you leave Canada to live in another country, you’re considered an emigrant for tax purposes once you sever your residential ties (such as selling your home, moving your spouse/dependents, and ending social ties in Canada). Here’s what you need to file: Key Forms and Filings • Final Canadian Tax Return (“Departure Return”) o Filed for the year you leave Canada. o Covers income earned from January 1 up to the date you became a non-resident. o After this, the CRA taxes you only on Canadian-sourced income (like rental property or investments). • Schedule A – Statement of World Income o Required if you were a resident of Canada for part of the year. o Declares worldwide income up to your departure date. • Form T1243 – Deemed Disposition of Property o Used to calculate “departure tax.” o When you leave, Canada treats most property as if you sold it, and you may owe capital gains tax. • Form T1161 – List of Properties by an Emigrant of Canada o Must be filed if the total fair market value of certain properties exceeds $25,000 CAD when you leave. o Includes items like shares, bonds, and real estate (but excludes personal-use property under $10,000). Important Notes • You must file a tax return for the year you leave if you owe taxes or want a refund. • Severing ties is key: if you keep significant ties (like a home or dependents in Canada), the CRA may still consider you a resident. • After departure, you’ll be taxed only on Canadian-source income, and you may need to file non-resident returns in future years.

Comments

-

7 месяцев назад

7 месяцев назад

-

Трансляция закончилась 3 года назад

Трансляция закончилась 3 года назад

-

12 дней назад

12 дней назад

-

Трансляция закончилась 1 месяц назад

Трансляция закончилась 1 месяц назад

-

2 недели назад

2 недели назад

-

5 дней назад

5 дней назад

-

5 дней назад

5 дней назад

-

13 дней назад

13 дней назад

-

6 лет назад

6 лет назад

-

5 часов назад

5 часов назад

-

Трансляция закончилась 2 дня назад

Трансляция закончилась 2 дня назад

-

4 года назад

4 года назад

-

4 дня назад

4 дня назад

-

2 года назад

2 года назад

-

2 месяца назад

2 месяца назад

-

2 месяца назад

2 месяца назад

-

5 лет назад

5 лет назад

-

2 месяца назад

2 месяца назад

-

Трансляция закончилась 1 день назад

Трансляция закончилась 1 день назад

-

![CCH Access Tax Software Demo: Tax Preparation Bootcamp Individual Return in 1 hour [2024]](https://imager.clipsaver.ru/LkaNyXMTbhA/max.jpg) 1 год назад

1 год назад