Finance Theory — 15.6: The CAPM: Beta and Systematic Risk скачать в хорошем качестве

Finance Theory — 15.6: The CAPM: Beta and Systematic Risk

12 часов назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Finance Theory — 15.6: The CAPM: Beta and Systematic Risk в качестве 4k

У нас вы можете посмотреть бесплатно Finance Theory — 15.6: The CAPM: Beta and Systematic Risk или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Finance Theory — 15.6: The CAPM: Beta and Systematic Risk в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Finance Theory — 15.6: The CAPM: Beta and Systematic Risk

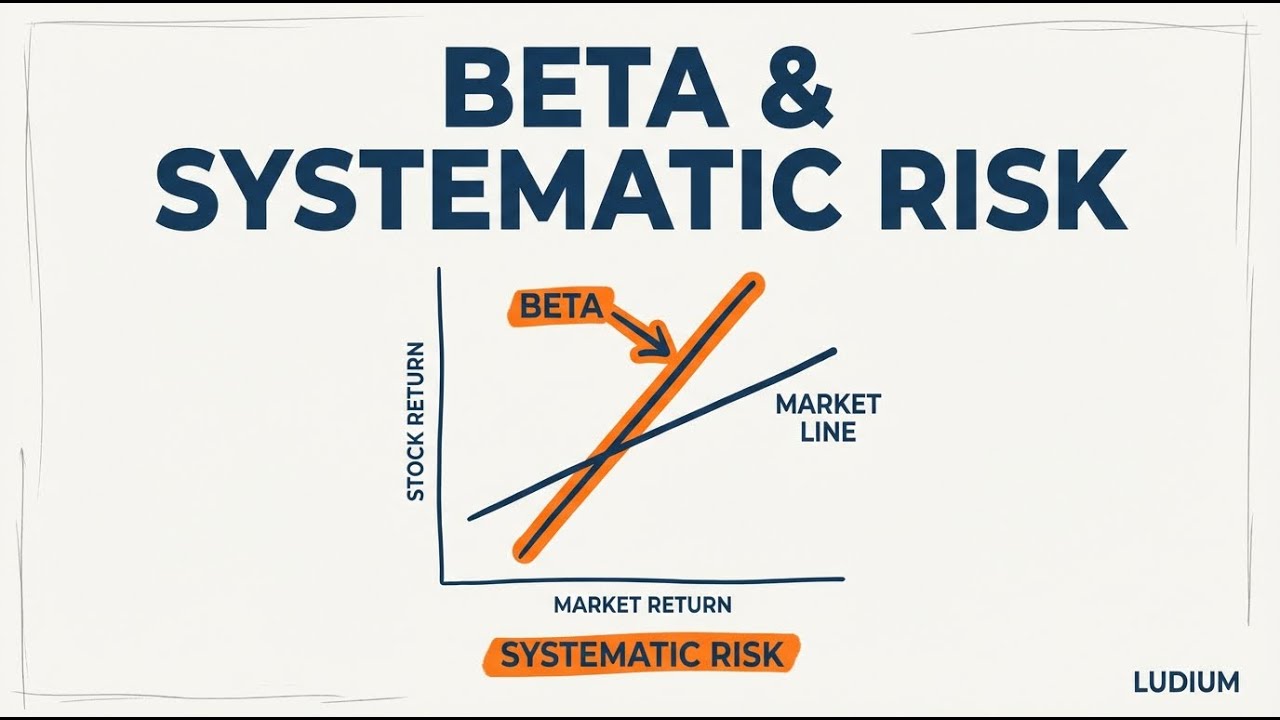

Why do two stocks with identical volatility earn vastly different expected returns? The Capital Asset Pricing Model reveals that the market only compensates investors for systematic risk — the portion that cannot be diversified away. This video walks through the full logic from the Capital Market Line to the Security Market Line, shows how beta is calculated, and demonstrates how the CAPM sets the cost of capital for real corporate investment decisions. Key concepts covered: • The Capital Market Line (CML) and how combining a risk-free asset with the market portfolio creates efficient portfolios • Historical U.S. equity risk premium (~7%) and market volatility (~15%) as empirical benchmarks • Why individual stocks sit below the CML due to idiosyncratic risk • The CAPM equation: E(Ri) = Rf + βi × (E(Rm) − Rf) • Beta as covariance of asset returns with the market divided by market variance • The Security Market Line (SML): expected return plotted against beta, identifying underpriced and overpriced assets • Total risk decomposition into systematic and idiosyncratic components for two stocks with equal 40% volatility but different betas • Why the CML is simply the CAPM restricted to efficient portfolios (β = σp / σm) • Common misconceptions: high volatility does not guarantee high expected returns, and beta is not a gut feeling about riskiness • Applying the CAPM to corporate finance: computing cost of capital (hurdle rate) and using it to discount cash flows for NPV analysis • Worked NPV example: a project with β = 1.2 yielding a 12.4% hurdle rate and a positive NPV of $204,776 ━━━━━━━━━━━━━━━━━━━━━━━━ SOURCE MATERIALS The source materials for this video are from • Ses 15: Portfolio Theory III & The CAPM an...

Comments

![KRYM PO 12 LATACH OKUPACJI PUTINA - SZPITALE WOJSKOWE ZAMIAST SANATORIÓW [BOJKE]](https://imager.clipsaver.ru/9wOp5s-3yRU/max.jpg)