Cost Accounting for Joint Products and By-Products | CA Inter | English | Costing Capsules скачать в хорошем качестве

Cost Accounting for Joint Products and By-Products | CA Inter | English | Costing Capsules

2 года назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Cost Accounting for Joint Products and By-Products | CA Inter | English | Costing Capsules в качестве 4k

У нас вы можете посмотреть бесплатно Cost Accounting for Joint Products and By-Products | CA Inter | English | Costing Capsules или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Cost Accounting for Joint Products and By-Products | CA Inter | English | Costing Capsules в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Cost Accounting for Joint Products and By-Products | CA Inter | English | Costing Capsules

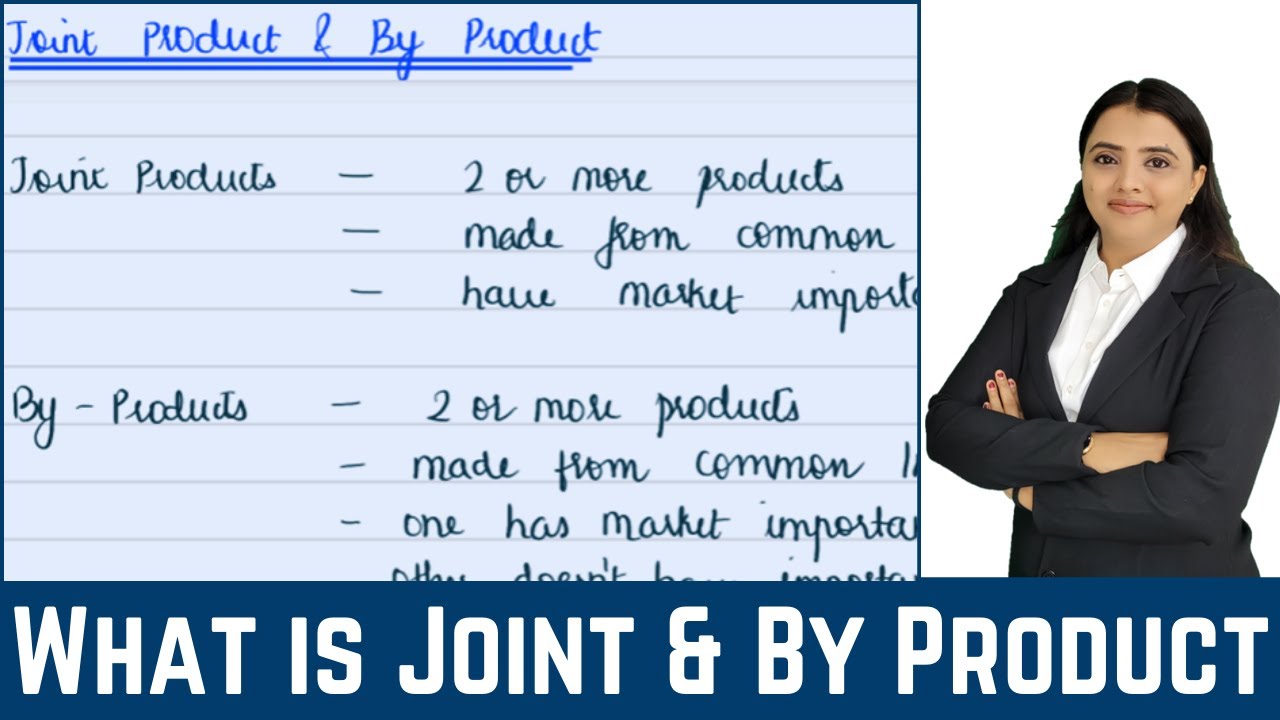

Detailed Explanation of Joint Products and By-Products: Joint Products: Joint products are two or more products that are produced simultaneously from a single production process. They share common inputs, such as raw materials, labor, and overhead costs. Examples of joint products include: Gasoline and diesel from crude oil -Lumber and wood chips from a tree The main challenge in joint product costing is to allocate the joint costs (i.e., the costs incurred up to the split-off point) to the individual joint products. This is necessary to determine the cost of each product and to set appropriate selling prices. By-Products: By-products are secondary products that are produced in addition to the main product(s) of a production process. They are usually of lesser value than the main products and may be generated unintentionally. Examples of by-products include: -Molasses from sugar production -Sawdust from lumber production By-products can be sold to generate additional revenue, or they can be used internally within the company. The decision of whether to sell or use a by-product depends on factors such as its market value, the cost of processing it further, and the availability of alternative sources of supply. Cost Allocation Methods: There are various methods for allocating joint costs to joint products. Some of the most commonly used methods include: Proportional Method: This method allocates joint costs based on the relative sales value of the joint products. Constant Gross Margin Method: This method allocates joint costs based on the assumption that each joint product should earn the same gross margin percentage. Physical Units Method: This method allocates joint costs based on the physical quantity of each joint product produced. The choice of cost allocation method depends on the specific circumstances of the business and the nature of the joint products. Profitability: The profitability of joint products and by-products is influenced by a number of factors, including: The market demand for the products The selling prices of the products The costs of production The efficiency of the production process By carefully managing these factors, businesses can maximize the profitability of their joint products and by-products. In summary, joint products and by-products are important concepts in cost accounting and profitability analysis. By understanding the different costing methods and management strategies, businesses can make informed decisions that lead to improved financial performance. Download our App: http://on-app.in/app/home?orgCode=ufzcg Benefits of App: 1. Personal Coach 2. Dedicated Doubt Clearing Space 3. Personalized Test Analysis 4. Study Booster Sessions 5. Free Preparatory Study Material 6. ICAI Update, Tips & strategy, Result update, Revision Marathon, Plan, etc 7. Live Online Classes 8. Learn from Past Year Question paper. Website: www.costingbydevangi.com Telegram: https://t.me/costingbydevangi Whatsapp: https://wa.me/message/HZ4LCPJ4SFZSI1 or 8097942402 Instagram: / devangim Facebook: / prof.ca.devangishah #JointProducts #ByProducts #CostAllocation #CostAccounting #ProfitabilityAnalysis #CostingMethods #ProportionalMethod #ConstantGrossMarginMethod #PhysicalUnitsMethod #ByProductManagement

Comments