Florida Foreclosure Complaint Overview of Newrez LLC vs Deloach with Lawman Scott live w/ ChatGPT. скачать в хорошем качестве

Florida Foreclosure Complaint Overview of Newrez LLC vs Deloach with Lawman Scott live w/ ChatGPT.

2 недели назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Florida Foreclosure Complaint Overview of Newrez LLC vs Deloach with Lawman Scott live w/ ChatGPT. в качестве 4k

У нас вы можете посмотреть бесплатно Florida Foreclosure Complaint Overview of Newrez LLC vs Deloach with Lawman Scott live w/ ChatGPT. или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Florida Foreclosure Complaint Overview of Newrez LLC vs Deloach with Lawman Scott live w/ ChatGPT. в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Florida Foreclosure Complaint Overview of Newrez LLC vs Deloach with Lawman Scott live w/ ChatGPT.

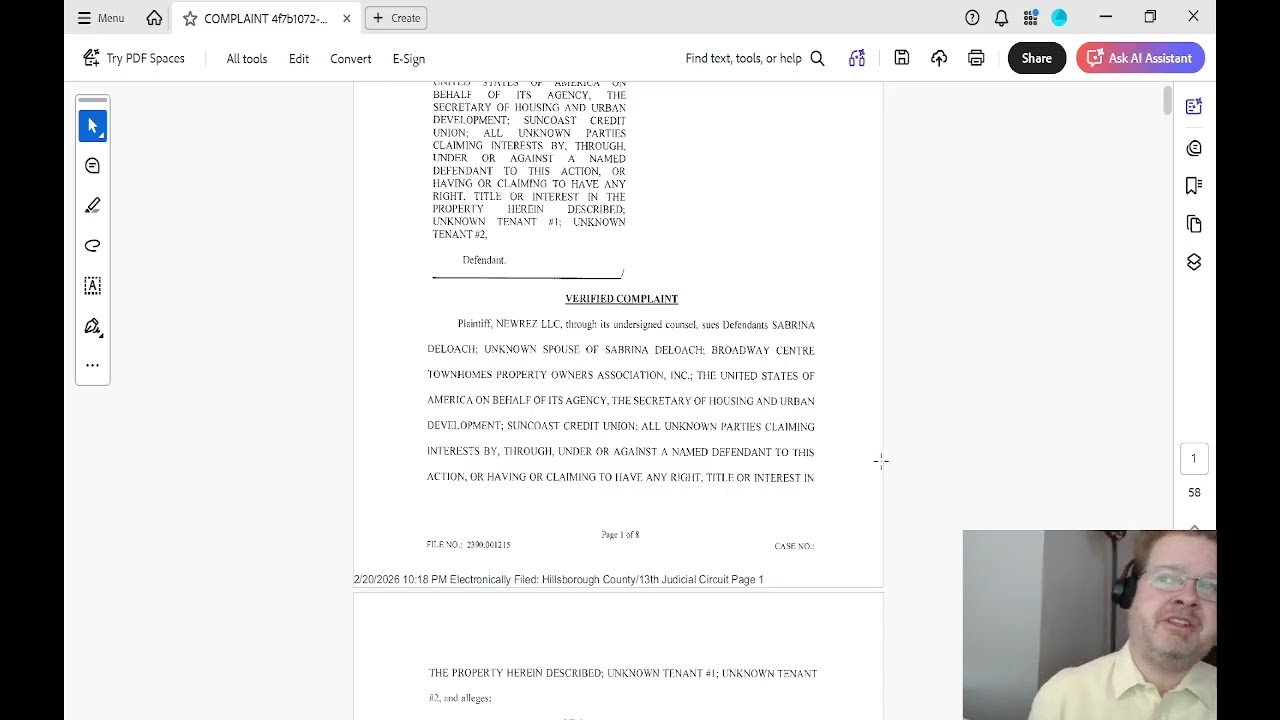

If you’ve been served with a foreclosure lawsuit in Florida, this video may change how you look at the entire process. In this detailed walkthrough, I break down a real verified mortgage foreclosure complaint filed in Hillsborough County, Florida and explain how a foreclosure defense attorney actually analyzes it. This is not surface level commentary. This is how these cases are evaluated in real practice. The complaint itself is only a few pages long, but the full PDF is nearly 60 pages with exhibits attached. For someone unfamiliar with litigation, that can feel overwhelming. I show you how to cut through the noise and focus on what matters. We cover: The 20 Day Deadline and Clerk’s Default If you are properly served in Florida, you generally have 20 days to respond. I explain what a Clerk’s Default is, how quickly it can change the posture of a case, and why it is not enough to simply “file something.” What you file at the outset shapes leverage, settlement posture, and long term strategy. Why So Many Parties Are Named The borrower. An unknown spouse. The homeowners association. The United States Secretary of Housing and Urban Development. A junior lienholder. Unknown tenants. All parties claiming interest. Foreclosure is not just about debt. It is about extinguishing competing property interests and clearing title. Every named party serves a strategic purpose. Pleading Capacity and Standing When an LLC files suit, it must have capacity to sue. More importantly, the plaintiff must establish standing at the inception of the lawsuit. Standing cannot be created later. If the foreclosing party did not hold the right to enforce the note when the case was filed, that issue can be outcome determinative. Note, Mortgage, and Loan Modifications Florida requires that when you sue on a written contract, you attach it. I explain why the note and mortgage must be included, what happens if they are not, and how loan modifications can complicate the principal balance and default analysis. Acceleration and “All Subsequent Payments” The complaint alleges default beginning with a specific missed payment and all payments after that. I explain acceleration in plain language and why, once triggered, the entire balance can be declared due. Why the Balance Increased The original note amount was approximately 198,000 dollars. The alleged balance now exceeds 239,000 dollars. We discuss capitalization of arrears, deferred principal, accrued interest, and how modifications can cause balances to grow instead of shrink. Attorney’s Fees and Reciprocal Rights The plaintiff alleges entitlement to attorney’s fees under the note and mortgage. In Florida, those provisions can become reciprocal. If the borrower prevails, the borrower may also be entitled to fees. That changes the risk analysis for both sides. HUD and FHA Implications The presence of the Secretary of Housing and Urban Development signals an FHA insured loan. That can trigger additional servicing requirements and strict compliance issues, including the importance of Paragraph 22 notice provisions. Paragraph 22 and Conditions Precedent Many Florida mortgages require specific pre acceleration notice language before foreclosure can proceed. Courts have dismissed cases for failure to strictly comply. Technical does not mean trivial. Technical can mean dispositive. Endorsements, Bearer Paper, and Allonges We discuss endorsements in blank, what bearer paper means, and what an allonge is. These concepts trace back to traditional negotiable instrument law but remain highly relevant in modern foreclosure litigation. Due Process and the Role of Defense Counsel Foreclosure defense is not about pretending default did not occur. It is about requiring strict compliance with procedural and contractual safeguards. The rule of law only works when it is enforced. Strategic Framing at the Outset The first 20 days matter. Early pleadings set the tone. They affect settlement leverage. They create time for potential workouts, loan modifications, short sales, or structured exits. If you are a Florida homeowner facing foreclosure, do not ignore the lawsuit. Early strategic decisions can expand or eliminate your options. If you are a lawyer considering adding foreclosure defense to your practice, this video gives you a structured framework for analyzing a verified complaint and spotting issues that may affect the outcome. Future videos will cover short sales in a declining market, FHA servicing defenses, loan modification strategy, and settlement leverage in foreclosure litigation. The goal is simple: protect due process, enforce the contract, and require compliance with the law. Subscribe for practical legal analysis designed to bring clarity to complex real estate litigation.

Comments

-

5 дней назад

5 дней назад

-

11 дней назад

11 дней назад

-

3 дня назад

3 дня назад

-

12 часов назад

12 часов назад

-

18 часов назад

18 часов назад

-

3 месяца назад

3 месяца назад

-

Трансляция закончилась 4 дня назад

Трансляция закончилась 4 дня назад

-

Трансляция закончилась 3 часа назад

Трансляция закончилась 3 часа назад

-

17 часов назад

17 часов назад

-

Трансляция закончилась 4 дня назад

Трансляция закончилась 4 дня назад

-

6 лет назад

6 лет назад

-

1 месяц назад

1 месяц назад

-

18 часов назад

18 часов назад

-

Трансляция закончилась 3 часа назад

Трансляция закончилась 3 часа назад

-

Трансляция закончилась 4 часа назад

Трансляция закончилась 4 часа назад

-

Трансляция закончилась 3 дня назад

Трансляция закончилась 3 дня назад

-

4 месяца назад

4 месяца назад

-

20 часов назад

20 часов назад