Endogeneity econometrics скачать в хорошем качестве

Endogeneity econometrics

8 лет назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Endogeneity econometrics в качестве 4k

У нас вы можете посмотреть бесплатно Endogeneity econometrics или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Endogeneity econometrics в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Endogeneity econometrics

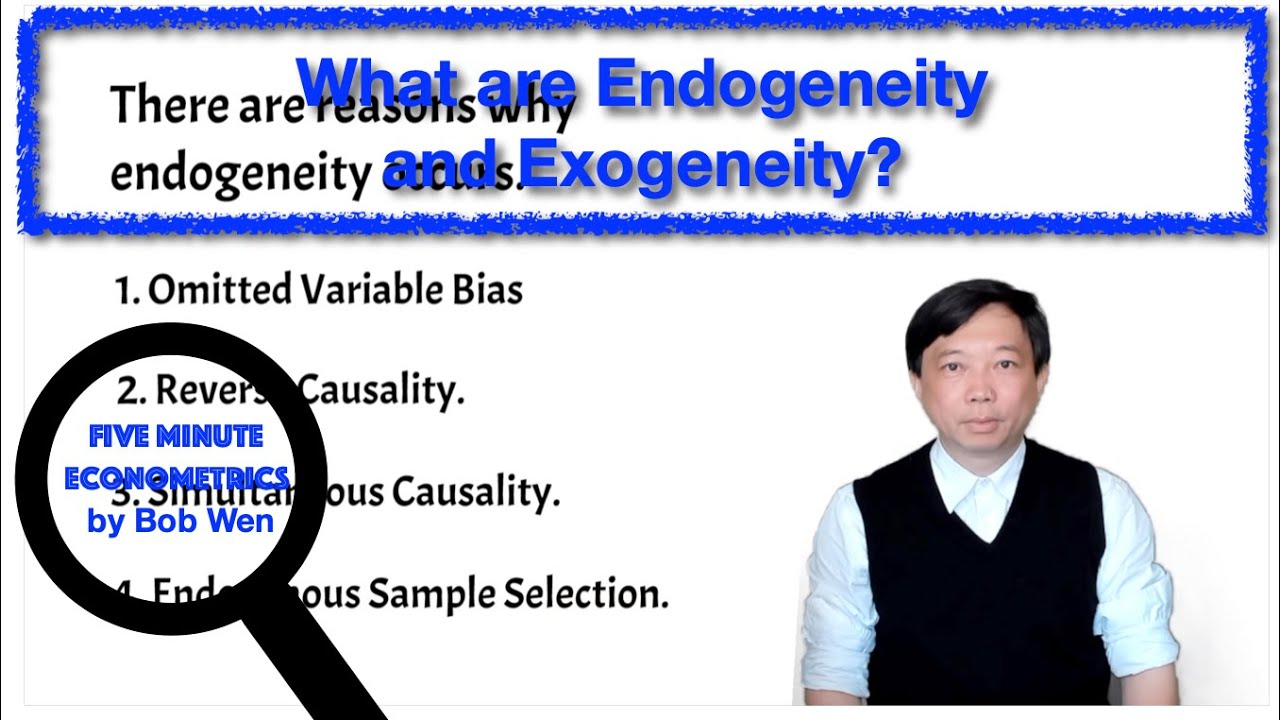

In econometrics, an endogeneity problem occurs when an explanatory variable is correlated with the error term.[1] Endogeneity can arise as a result of measurement error, autoregression with autocorrelated errors, simultaneous causality (see Instrumental variable), omitted selection, and omitted variables [2]. Two common causes of endogeneity are: 1) an uncontrolled confounder causing both independent and dependent variables of a model; and 2) a loop of causality between the independent and dependent variables of a model. The problem of endogeneity is very serious and oftentimes ignored by researchers conducting non-experimental research[3][4]. For example, in a simple supply and demand model, when predicting the quantity demanded in equilibrium, the price is endogenous because producers change their price in response to demand and consumers change their demand in response to price. In this case, the price variable is said to have total endogeneity once the demand and supply curves are known. In contrast, a change in consumer tastes or preferences would be an exogenous change on the demand curve.

Comments

![Endogénéité: une vérité qui dérange (pour les chercheurs) [VF]](https://imager.clipsaver.ru/HfC3IHCm9lg/max.jpg)