Review of the accounting Process-Intermediate Accounting 1-Summer 2013(L1)-Professor Rebecca Bloch скачать в хорошем качестве

Review of the accounting Process-Intermediate Accounting 1-Summer 2013(L1)-Professor Rebecca Bloch

12 лет назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Review of the accounting Process-Intermediate Accounting 1-Summer 2013(L1)-Professor Rebecca Bloch в качестве 4k

У нас вы можете посмотреть бесплатно Review of the accounting Process-Intermediate Accounting 1-Summer 2013(L1)-Professor Rebecca Bloch или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Review of the accounting Process-Intermediate Accounting 1-Summer 2013(L1)-Professor Rebecca Bloch в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Review of the accounting Process-Intermediate Accounting 1-Summer 2013(L1)-Professor Rebecca Bloch

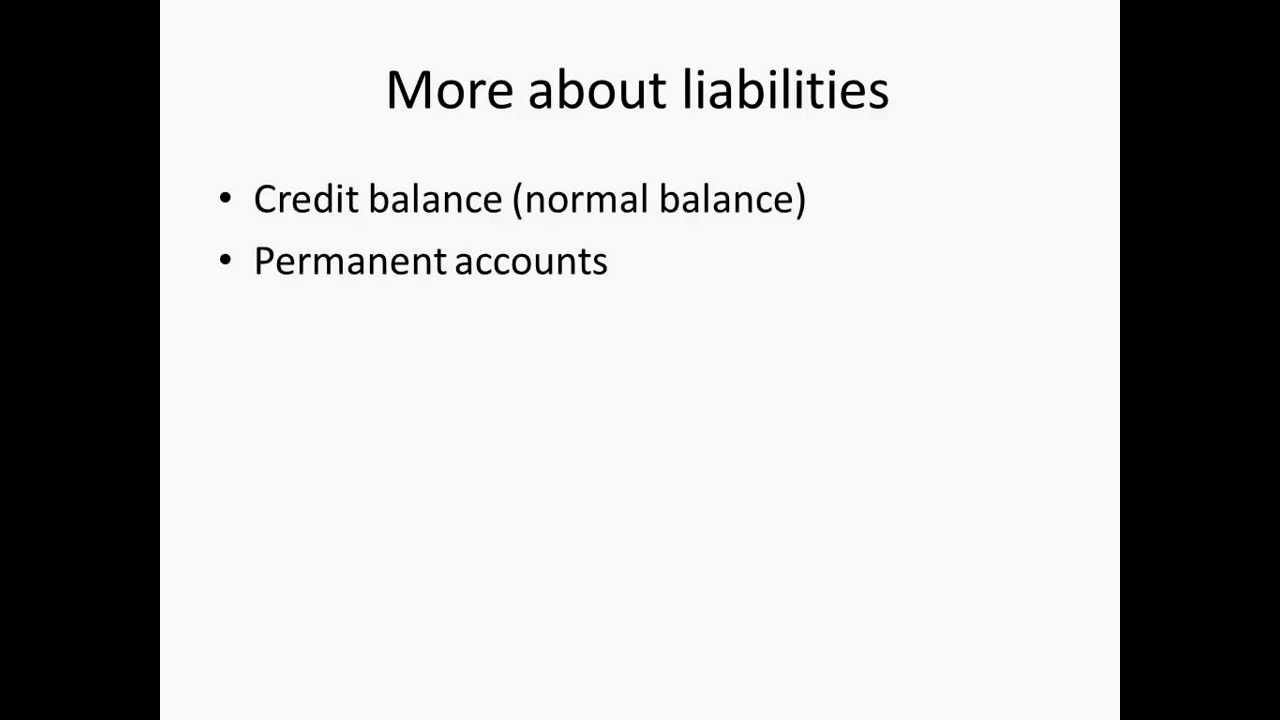

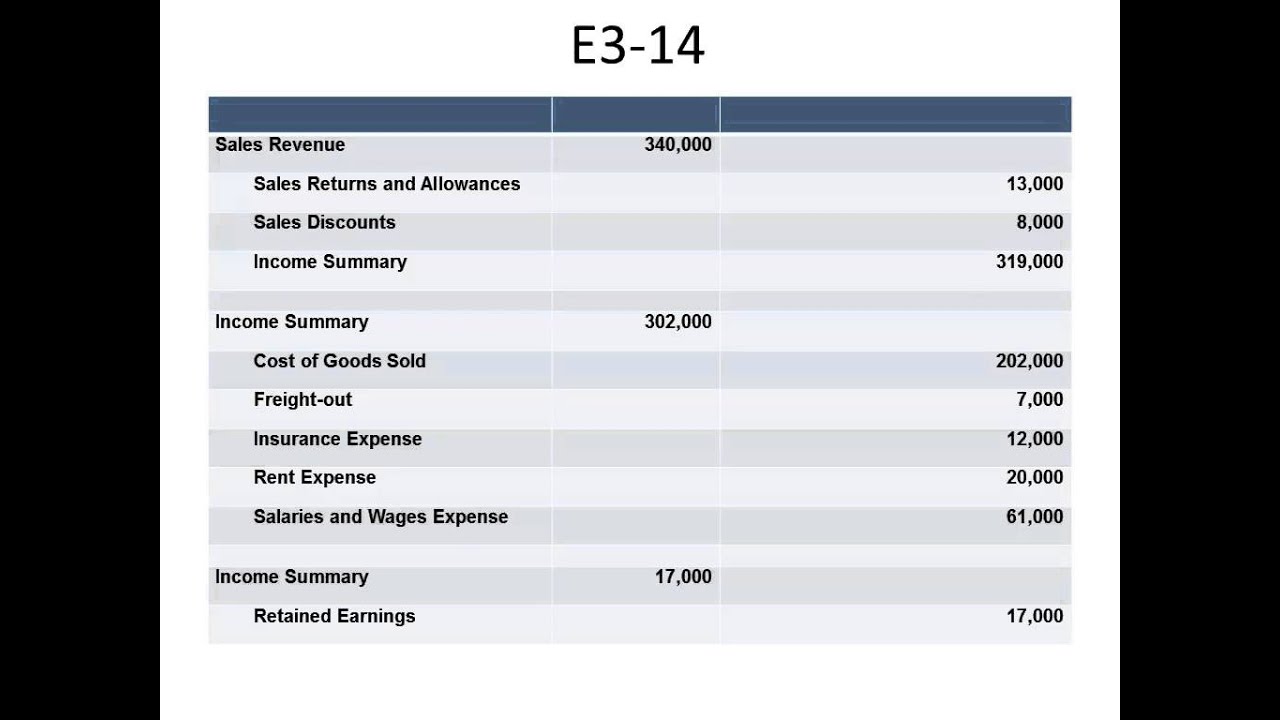

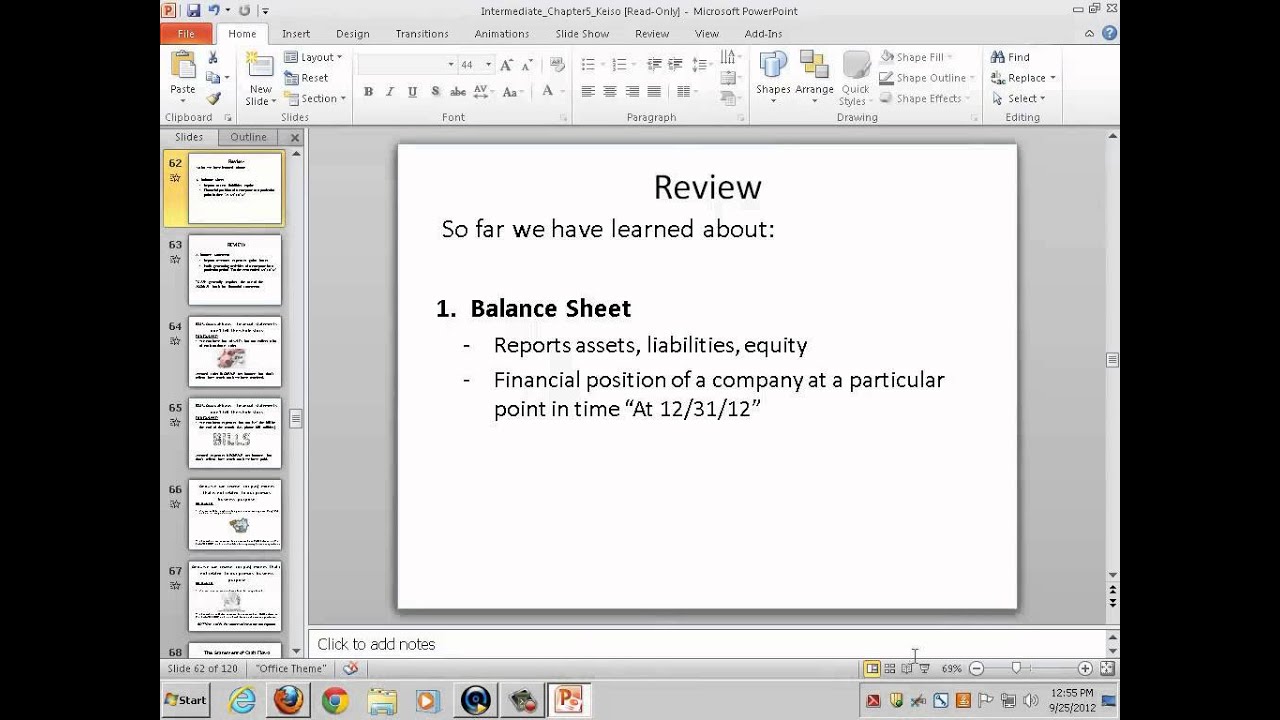

Intermediate Accounting I Lecture 1: Review of the Accounting Process (Part 1) by Rebecca Bloch All companies must record (accounting for) transactions that occur in a business (sales made, bills paid, etc). Accounting is the profession that tells us how to account for these transactions. Auditors review the accounting records that employees of a company enter into the accounting system. Thus, whether we are internal (employees) or external (auditors) it is crucial to understand how to properly account for transactions whether we work as external auditors or internal accounting employees of a company. Accounting data is important because it is ultimately consolidated into financial statements (income statements, balance sheets, statement of cash flows, etc). Financial statements are used by creditors and investors to make important investment decisions. Accounting rules can influence the decisions that we make as either internal or external users (internal users may favor rules that help them to show increases expenses to reduce taxes, while external users may see additional expenses as a sign that they should not invest). Accounting is the language of business. The accounting equation is assets are equal to liabilities plus owner's equity (ALOE), and they are used to capture economic events of an entity (i.e. what assets are owned and how they were obtained). An asset is a resource of a firm that will benefit the firm in the future. Examples of common assets include cash, accounts receivable, investments, inventory, prepaid expenses, and fixed assets. Most assets have a debit balance (normal balance) and are permanent accounts. A liability is a probable future sacrifice of economic benefits arising from present obligations of an entity to transfer assets or provide services to other entities in the future as a result of past transactions or events. Examples of liabilities include accounts payable, notes payable, accrued expenses, salaries payable, interest payable, and unearned revenue. Most liabilities have credit balances and are permanent accounts. Owners equity is the same thing as shareholder's / stockholder's equity. The residual interest in the assets of an entity that remain after deducting liabilities (A - L = OE). Equity is composed of common stock, paid-in capital, retained earnings, accumulated other comprehensive income, and distributions made to owners (dividends). Most have credit balances (unless a cumulative loss exists), and are permanent accounts (note that ALL balance sheet items are permanent accounts). Revenues and expenses, however, are temporary accounts that go into the equity section at the end of the year. Debits are the left side of a T-account and increase expenses, assets, and dividends. Debits should increase inventory, depreciation expense, prepaid rent, cost of goods sold, utility expense, equipment, and accounts receivable, bad debt expense, and interest expense. They should decrease accounts payable, sales revenue, common stock, wages payable, and allowance for uncollectible accounts, interest revenue, and gains on sale of equipment. Credits are the left side of a T-account and increase liabilities, income, common stock, capital, owner's equity, retained earnings, and revenues. Other key terms in accounting that should be familiarized with is the general ledger, t-accounts, journal entries, accrual basis, US GAAP, IFRS, permanent accounts (all asset, liability, and equity accounts), temporary accounts (all revenue & expense accounts), trial balance, and financial statements. Class Starts: 0:06 What is Accounting?: 1:02 Why is Accounting Important?: 4:05 The Fundamentals of Accounting: 9:58 What is an Asset?: 12:12 --- Examples of Assets: 13:53 --- More About Assets: 15:13 What is a Liability?: 16:27 --- Examples of Liabilities: 18:10 --- More About Liabilities: 20:04 Owners' Equity: 20:48 --- More About Equity: 27:46 Important Terms: 28:56 Debits: 46:21 Credits: 47:11 Game: Does a Debit Increase or Decrease...?: 48:11 Exercise 3-1: 55:31 Trial Balance Example: 1:06:01 Trial Balance from E3-1: 1:08:47 Adjusting Entries --- Accruals: 1:08:55 --- Prepayments: 1:15:47 --- Estimates: 1:17:57 --- Depreciation: 1:18:36 To receive additional updates regarding our library please subscribe to our mailing list using the following link: http://rbx.business.rutgers.edu/subsc...

Comments

![James Webb: How to Read a Financial Statement [Crowell School of Business]](https://imager.clipsaver.ru/Jkse-Wafe9U/max.jpg)