Quantum Finance - Quantum Monte Carlo for Option Pricing - qubit-lab.ch скачать в хорошем качестве

Quantum Finance - Quantum Monte Carlo for Option Pricing - qubit-lab.ch

6 месяцев назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Quantum Finance - Quantum Monte Carlo for Option Pricing - qubit-lab.ch в качестве 4k

У нас вы можете посмотреть бесплатно Quantum Finance - Quantum Monte Carlo for Option Pricing - qubit-lab.ch или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Quantum Finance - Quantum Monte Carlo for Option Pricing - qubit-lab.ch в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Quantum Finance - Quantum Monte Carlo for Option Pricing - qubit-lab.ch

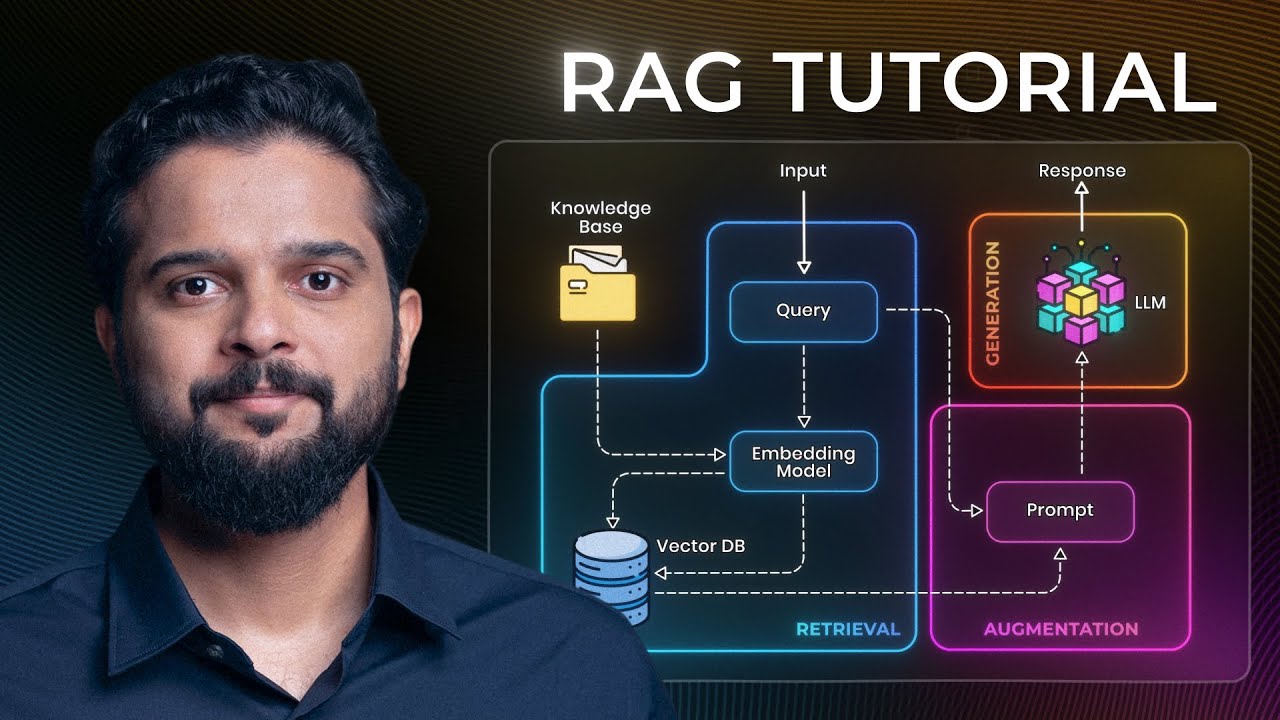

⚡️ Can quantum algorithms really speed up option pricing? In this video, we explore how Quantum Monte Carlo—and especially Quantum Amplitude Estimation (QAE)—could transform the way we price financial derivatives. 📈 You’ll learn: • Why Monte Carlo methods are essential for complex option pricing • How quantum circuits can simulate log-normal price distributions • The quadratic speedup of QAE: from 1/√N to 1/N error scaling • A hands-on comparison of three methods: Classical Monte Carlo, Quantum Monte Carlo, and the Black-Scholes formula • Live Python code, real-world examples, and visual walkthroughs 🚀 We’re still early—but this tech has the potential to reshape risk, pricing, and simulation workloads in finance. All code, resources, and videos at qubit-lab.ch Smash that like button if you want to stay ahead of the quantum finance curve! #QuantumFinance #QuantumMonteCarlo #QAE #OptionPricing #BlackScholes #Qiskit #QuantumComputing #Python #Investing #Derivatives

Comments

-

6 месяцев назад

6 месяцев назад

-

1 год назад

1 год назад

-

1 месяц назад

1 месяц назад

-

8 месяцев назад

8 месяцев назад

-

6 лет назад

6 лет назад

-

4 месяца назад

4 месяца назад

-

8 дней назад

8 дней назад

-

Трансляция закончилась 7 часов назад

Трансляция закончилась 7 часов назад

-

3 недели назад

3 недели назад

-

5 лет назад

5 лет назад

-

5 месяцев назад

5 месяцев назад

-

4 месяца назад

4 месяца назад

-

6 месяцев назад

6 месяцев назад

-

1 год назад

1 год назад

-

![Цепи Маркова — математика предсказаний [Veritasium]](https://imager.clipsaver.ru/QI7oUwNrQ34/max.jpg) 4 месяца назад

4 месяца назад

-

3 года назад

3 года назад

-

4 недели назад

4 недели назад

-

3 недели назад

3 недели назад

-

6 месяцев назад

6 месяцев назад

-

2 месяца назад

2 месяца назад