Chapter 1.3: Identification of UPE & IPEs скачать в хорошем качестве

Chapter 1.3: Identification of UPE & IPEs

2 недели назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Chapter 1.3: Identification of UPE & IPEs в качестве 4k

У нас вы можете посмотреть бесплатно Chapter 1.3: Identification of UPE & IPEs или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Chapter 1.3: Identification of UPE & IPEs в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Chapter 1.3: Identification of UPE & IPEs

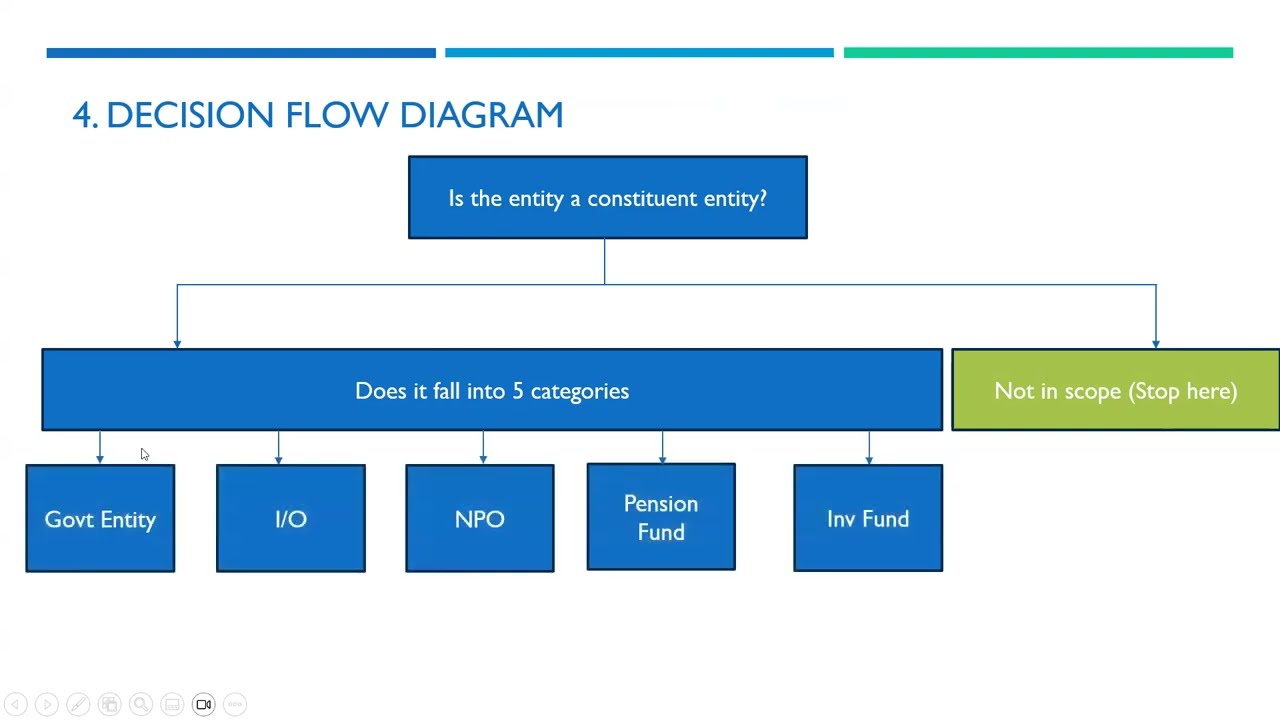

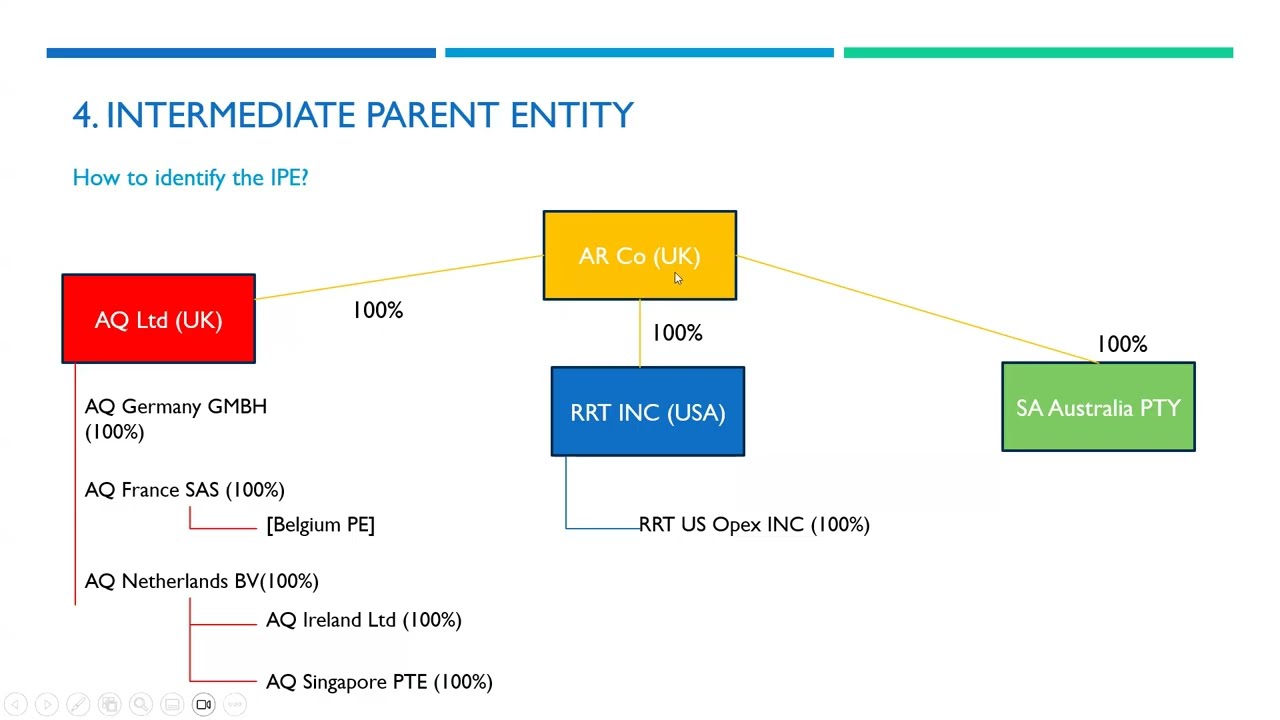

In Video 03 of our ADIT Pillar Two Award prep series, we tackle the hierarchy of the GloBE rules. Once you've identified your Constituent Entities, the next critical step is determining which entity in the group is actually liable to pay the Top-Up Tax under the Income Inclusion Rule (IIR). What we cover in this video: The Ultimate Parent Entity (UPE): We break down the definition of a UPE under Article 1.4—the entity that sits at the top of the consolidation chain and is not owned by any other entity with a controlling interest. Intermediate Parent Entities (IPEs): Understanding the role of an IPE (an entity that owns an interest in a low-taxed constituent entity but is itself owned by another parent). The Top-Down Approach: We explain the primary priority rule. In the first instance, the UPE is responsible for the group’s Top-Up Tax. If the UPE is in a jurisdiction without a Qualified IIR, the obligation "drops down" to the next IPE in the chain. Controlling Interest: A deep dive into what constitutes "control" for GloBE purposes, moving beyond simple share percentages to accounting consolidation principles. Key Learning Outcomes: Apply the Article 1.4 tests to identify the UPE of any MNE Group. Determine the priority of IIR application between a UPE and various IPEs.

Comments