Chapter 1.4: Excluded Entities Assessment скачать в хорошем качестве

Chapter 1.4: Excluded Entities Assessment

2 недели назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Chapter 1.4: Excluded Entities Assessment в качестве 4k

У нас вы можете посмотреть бесплатно Chapter 1.4: Excluded Entities Assessment или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Chapter 1.4: Excluded Entities Assessment в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Chapter 1.4: Excluded Entities Assessment

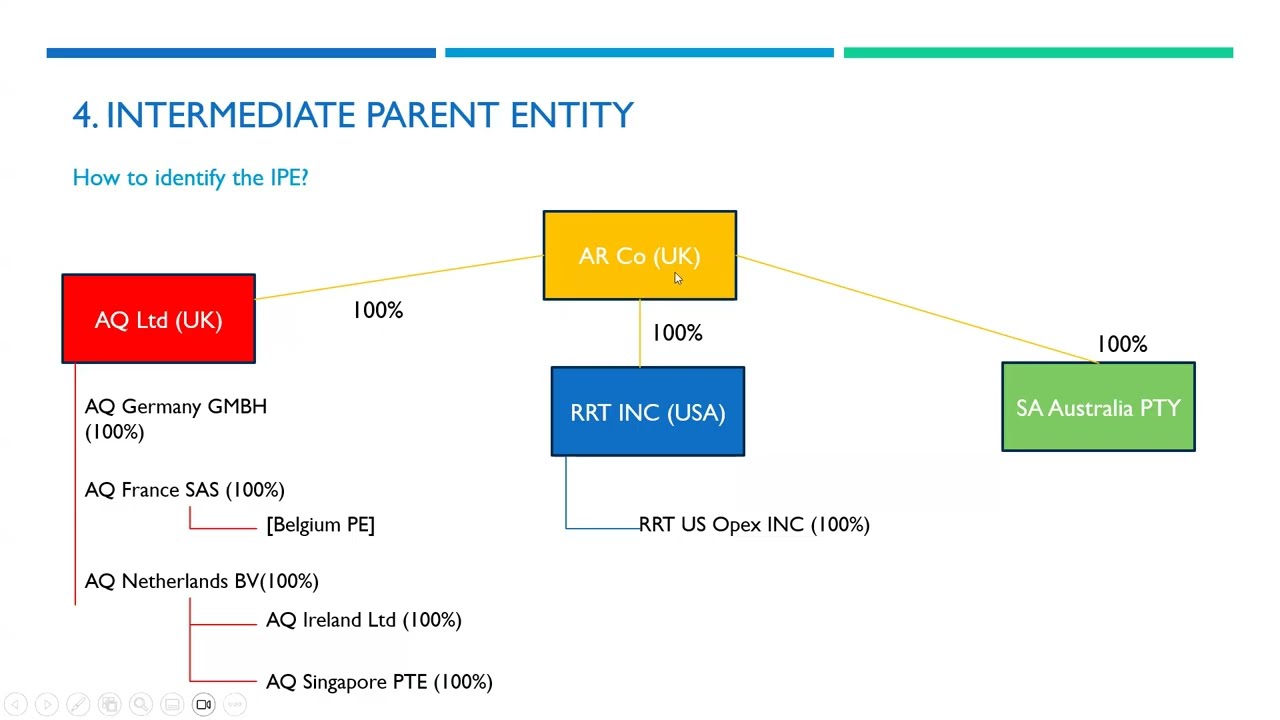

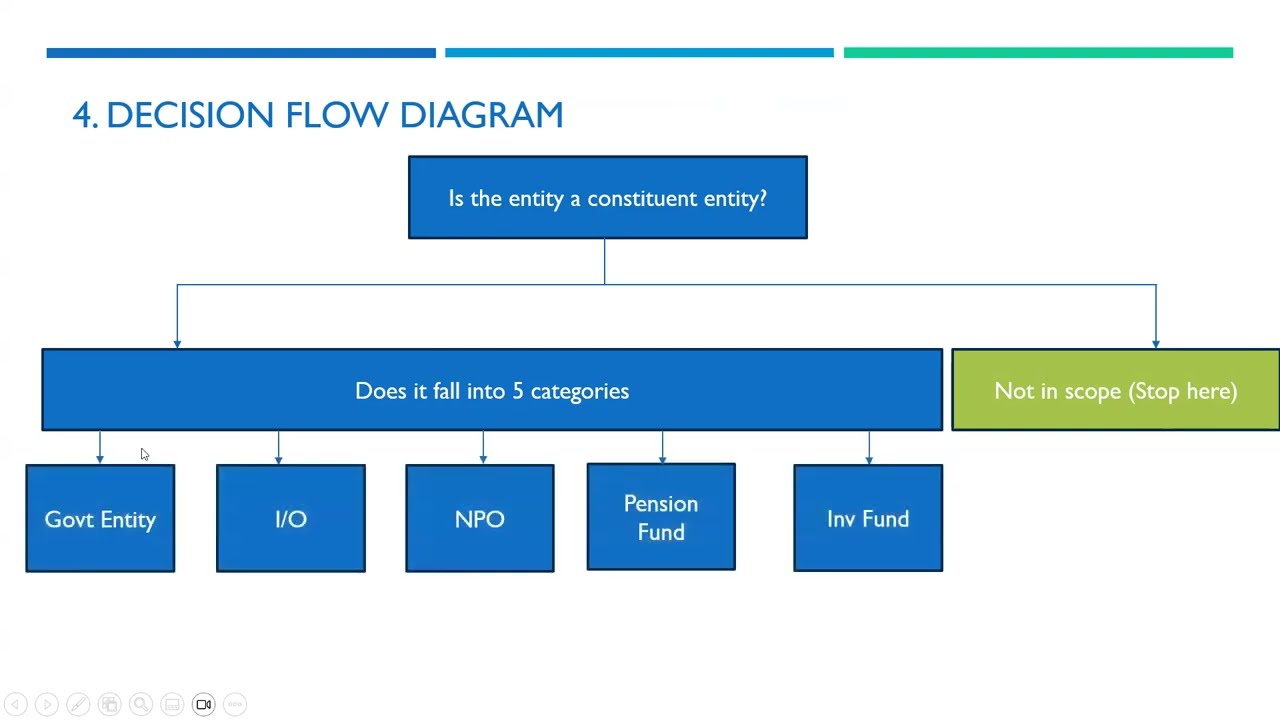

In Video 04 of our ADIT Pillar Two Award prep series, we dive into the "Excluded Entity" framework. While the €750M revenue threshold brings a group into scope, not every entity within that group is treated as a "Constituent Entity" subject to the GloBE charging mechanics. What we cover in this video: The Big Five Categories: We define the core organizations that are naturally excluded from the rules: Governmental Entities (e.g., Sovereign Wealth Funds not engaged in trade). International Organisations. Non-profit Organisations (including charities and certain religious bodies). Pension Funds. Investment Funds / Real Estate Investment Vehicles (specifically when they act as the UPE). Key Learning Outcomes: Correctly classify an entity as "Excluded" or "Constituent" under the Article 1.5 criteria. Understand the "Ancillary Activities" test for subsidiaries of non-profits and pension funds. Calculate the impact of excluded entities on the consolidated group's €750M threshold.

Comments